Farmland Investing: Returns, Risks, and Accessibility

19.05.2026

6

Farmland has moved from a niche allocation to a recognised real-asset class in institutional portfolios. This guide explains how it generates returns, how it behaves across economic cycles, the principal risks, and the routes through which retail investors can now gain exposure — including how income-oriented crowdlending fits alongside it.

Real-asset exposure increasingly combines physical land with digital portfolio management.

Farmland generates returns through two channels: ongoing income from leasing agricultural land to farmers, and long-term appreciation of the land itself. Cash rent leases provide predictable annual payments regardless of harvest, while crop-share agreements link income to commodity yields. Limited arable land combined with structural food demand has historically supported steady appreciation across cycles.

How does farmland generate returns?

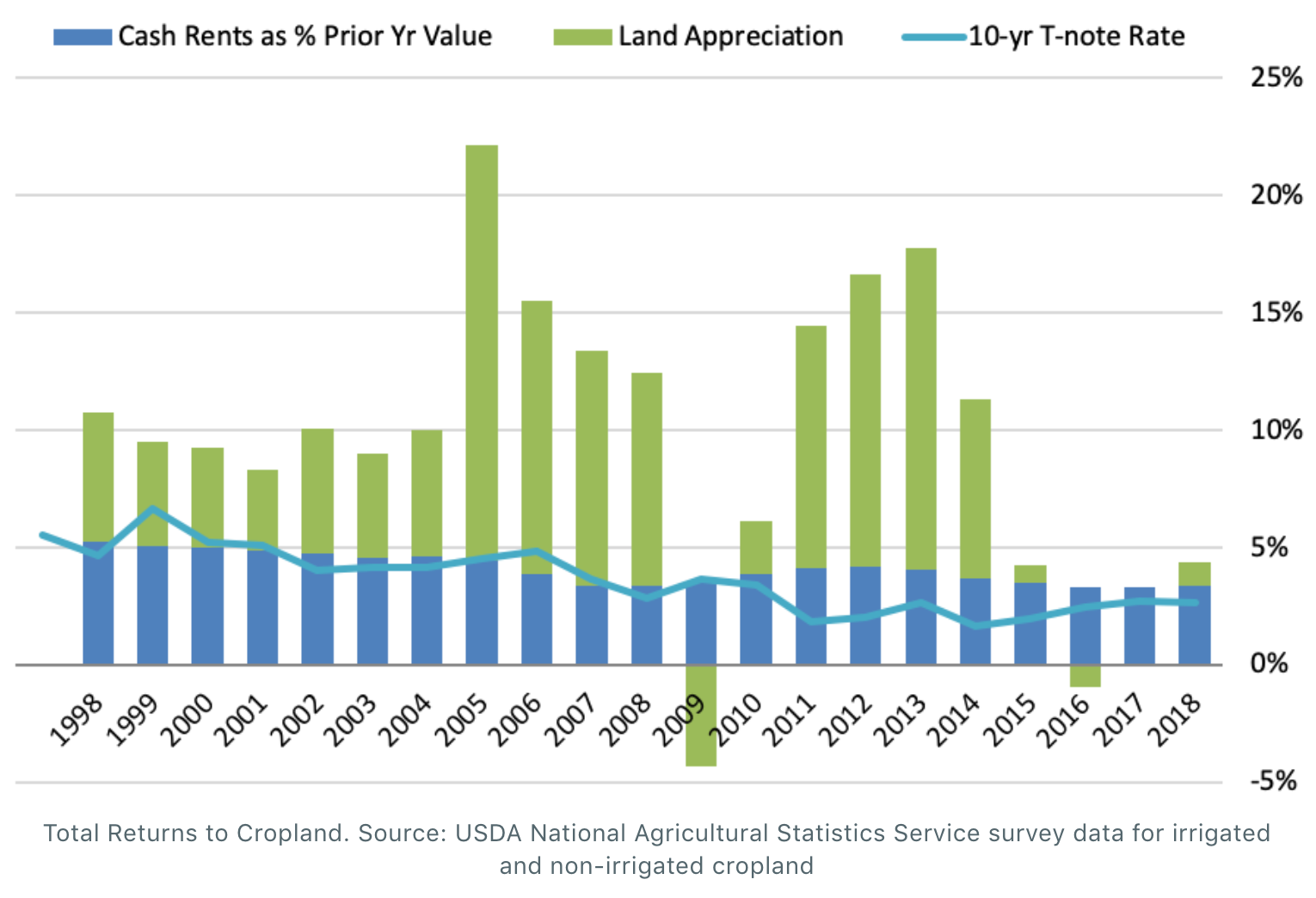

Farmland produces returns from two distinct sources: lease income paid by farmers operating the land, and capital appreciation of the land itself. Income tends to be the more stable of the two, while appreciation is influenced by commodity cycles, productivity gains, and the long-run scarcity of arable land. USDA National Agricultural Statistics Service data on irrigated and non-irrigated cropland shows that, between 1998 and 2018, cash rent income remained positive every year while land appreciation contributed an additional component in most years (source: USDA NASS, 2019).

Total returns to U.S. cropland, 1998–2018: cash rents (blue) remained positive each year; land appreciation (green) added a variable second component. Source: USDA National Agricultural Statistics Service survey data for irrigated and non-irrigated cropland.

How do farmland leases work?

The majority of farmland income comes from leasing land to farm operators. The two dominant lease structures differ in how risk and return are shared.

Cash rent lease

Tenant pays a fixed annual amount regardless of crop performance. Income is predictable; operational risk sits entirely with the farmer.

Crop-share lease

Landowner receives a percentage of the harvest revenue. Income varies with yield and commodity prices; investor participates in upside and downside.

Flexible / variable

Hybrid structure: a base cash rent plus a bonus tied to revenue or yield thresholds. Common in U.S. Midwest grain belt operations.

Custom farming

Landowner retains all crop revenue and pays the operator a fixed fee for labour and equipment. Maximum exposure to commodity prices.

Why does farmland appreciate over time?

Arable land is finite: it cannot be manufactured, and changes in zoning, urbanisation, and erosion reduce the available stock over time. Productivity improvements — irrigation, drainage, precision agriculture — increase the income a given parcel can support, which in turn supports higher valuations. The Cambridge Centre for Alternative Finance and the Bank of England have both identified land scarcity as a structural support for agricultural asset values in non-bank lending studies (source: Bank of England research on real assets, 2023).

How do commodity prices affect farmland returns?

Crop prices influence farm profitability, rent renewal rates, and, indirectly, land values. Lease structures smooth this volatility: a cash rent contract isolates the landowner from a poor harvest, while a crop-share contract transmits price movements directly to investor income. Across cycles, lease income tends to be less volatile than commodity prices themselves.

How has farmland performed across market cycles?

Farmland returns are driven by food consumption and lease economics rather than by corporate earnings or equity market sentiment. Historically, this has produced a return profile that diverges from listed equities and fixed income, which is the basis for its role as a diversifying real asset.

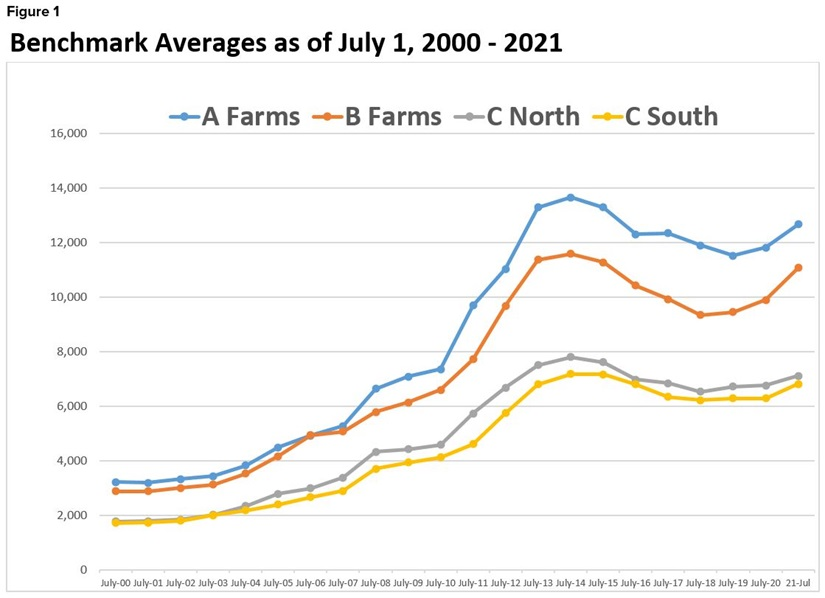

Benchmark farmland values per acre by quality grade, July 2000 to July 2021. Source: Iowa State University, Farmland Value Survey, 2021.

How does farmland behave during economic expansions?

In expansion phases, rising incomes and food consumption support agricultural demand, which translates into stable rents and gradual appreciation. Farmland does not match the upside of equities in strong bull markets but contributes lower-volatility returns to a multi-asset portfolio. The pattern is consistent with broader observations on aligning investment strategy with economic cycles.

How has farmland performed in recessions?

USDA cropland data show only one year of negative total return between 1998 and 2018 — 2009, during the global financial crisis — and the drawdown was modest compared with equity market losses that year. Cash rent income remained positive throughout, providing income continuity even as land appreciation paused. The asset class is not recession-proof, but its drawdowns have historically been shallower and shorter than those of listed equities.

Does farmland act as an inflation hedge?

Farmland income and land values both respond to general price levels: food prices feed into rent renewals, and input costs reset both yields and asset valuations. The asset class has historically preserved real purchasing power better than fixed-rate bonds during inflationary episodes, although the response can lag by one to two years. For a portfolio approach that combines real assets with income-generating credit, see our overview of alternative investments and what options exist.

How can investors access farmland today?

Until the 2010s, direct farmland ownership required substantial capital and operational expertise. Three modern routes have lowered the barriers significantly: publicly listed REITs, private fractional ownership platforms, and crowdlending platforms financing agribusiness loans.

Listed equities

Public REITs

Farmland Partners (FPI) and Gladstone Land (LAND) own and lease cropland across the U.S. Daily liquidity and full transparency, but share prices can diverge from underlying land values, particularly under equity market stress.

Private platforms

Fractional ownership

Investors purchase fractional interests in individual farms or diversified portfolios. Lower minimums than direct ownership, but longer lockups, higher management fees, and limited secondary liquidity.

Debt exposure

Crowdlending

Investors finance agribusiness loans secured by collateral, receiving scheduled interest payments. Shorter durations and contractual income terms, distinct from equity ownership of the land itself.

Direct

Outright ownership

Buying agricultural land directly. Highest capital requirement, full operational responsibility, and the most direct exposure to both appreciation and lease income — typical of family offices and institutional investors.

How do farmland REITs compare with fractional platforms?

REITs trade like equities — minute-by-minute pricing, daily liquidity — but inherit equity market volatility. Fractional platforms hold the actual asset and report values quarterly or annually, smoothing volatility but locking up capital for years. The choice depends on the investor's liquidity horizon and tolerance for mark-to-market price swings.

How does agribusiness crowdlending differ from owning farmland?

Crowdlending provides debt rather than equity exposure. Investors do not own the land; they fund a business loan to an agricultural operator, typically secured by collateral, and receive interest payments under contractually defined terms. Durations are shorter — usually 6 to 36 months versus multi-year ownership — and the return profile is income-led rather than appreciation-led.

Spotlight — Maclear AG

Swiss crowdlending with collateral and a Provision Fund

Maclear AG is a Swiss-based crowdlending platform connecting investors with EU-based business borrowers, including agribusiness operators in the Baltic region and neighbouring EU markets. Each project is graded on a proprietary AAA-to-D scale and assessed by Maclear's credit team before listing.

Two features distinguish Maclear's risk management. Loans are backed by physical collateral, with Maclear acting as collateral agent on behalf of investors. A Provision Fund provides an additional buffer, absorbing late-payment risk so that investor interest payments continue while Maclear works with the borrower on recovery.

Farmland has a defensive return profile, but it is not low-risk. Four risk categories materially affect outcomes and should be understood before committing capital.

WeatherDroughts, floods, frost, and heat waves directly reduce yields. Crop insurance and geographic diversification mitigate some exposure, but climate variability remains an unavoidable feature of agricultural investing. The European Central Bank has documented increasing weather-related credit risk in agricultural lending portfolios (source: ECB Financial Stability Review, 2024).

CommoditySharp declines in crop prices reduce tenant income and may limit rent renewal at higher rates. Cash rent leases insulate the landowner from a single bad season but not from prolonged commodity downturns.

OperatorPerformance depends on the financial strength and skill of the farmer operating the land. Undercapitalisation, poor agronomy, or operational errors increase default and lease-disruption risk. Operator selection is a primary underwriting concern.

RegulatoryZoning, environmental rules, water rights, foreign ownership restrictions, and changes in agricultural subsidies all affect land use and value. Trade policy shifts can also influence farm economics independently of agronomic outcomes.

These risks do not negate farmland's appeal, but they justify diversification, professional underwriting, and conservative position sizing. For a broader treatment of how different asset classes behave under stress, see how to protect your money with crisis-proof investments.

Why is farmland illiquid, and what does it mean for investors?

Farmland is intrinsically a long-horizon asset. Unlike publicly traded securities, fields and orchards cannot be sold quickly without price concessions. This illiquidity is often cited as a drawback, but for patient investors it also imposes return discipline and limits behavioural mistakes.

How long does it take to sell farmland?

Direct sales typically take months rather than days, depending on location, land quality, local demand, and commodity conditions. Farmland is best suited to investors with multi-year or multi-decade horizons who do not require near-term access to capital.

How is farmland valued?

Farmland values come from periodic appraisals based on comparable sales, income potential, and land characteristics. Appraisal-based pricing smooths short-term volatility relative to mark-to-market securities, but it can also lag real economic conditions. Values may appear stable during stress and adjust gradually over the following 12 to 24 months.

How does crowdlending compare on liquidity?

Crowdlending sits between direct farmland ownership and listed equities on the liquidity spectrum. Loans have defined durations of months rather than years, and Maclear's Secondary Market allows investors to list claims for resale to other investors via Good 'Til Cancelled (GTC) listings. Liquidity on a secondary market depends on buyer demand and is not guaranteed.

Where does crowdlending fit alongside farmland?

Farmland and agribusiness crowdlending occupy different positions in a real-asset allocation. Farmland is equity-like: long-duration, appreciation-driven, illiquid. Crowdlending is debt-like: shorter-duration, income-driven, with contractually defined cash flows and collateral protection. The two can complement rather than substitute for each other.

Farmland offers durability through scarcity and food demand; crowdlending offers durability through contractual income and collateral. A portfolio can use both — one for long-horizon real-asset exposure, the other for shorter-duration cash flow.

Key takeaways

Farmland generates returns from lease income and long-term land appreciation; income tends to be the more stable of the two.

USDA cropland data show positive cash-rent returns in every year between 1998 and 2018, with only one year of negative total return (2009).

Retail investors can access farmland through public REITs (Farmland Partners, Gladstone Land), private fractional ownership platforms, or agribusiness crowdlending.

The four principal risks are weather, commodity prices, operator quality, and regulation — all manageable with diversification and professional underwriting.

Direct farmland ownership is illiquid by design, with sale timelines measured in months; appraisal-based valuations smooth volatility but lag real conditions.

Crowdlending provides shorter-duration, income-led debt exposure that can complement rather than substitute for equity ownership of land.

Practical conclusion

Farmland earns its place in a portfolio through durability rather than upside. Its return profile is anchored in food production, land scarcity, and lease economics, which is why it has been a quiet mainstay of institutional portfolios for decades. The trade-offs are real: illiquidity, operational complexity, and exposure to weather, commodities, regulation, and operator quality.

For investors who want exposure to real economic activity without committing capital for a decade, agribusiness crowdlending offers a structurally different but complementary allocation. Maclear provides graded, collateral-backed business loans with a Provision Fund as an additional buffer, scheduled income, and access to a Secondary Market for liquidity (subject to demand). The two — farmland and crowdlending — can sit together in a diversified, real-asset-aware portfolio.

Looking to add real-economy exposure to a diversified portfolio? Browse Maclear's open projects — each with full grading, collateral details, and a defined repayment schedule.

Maclear AG is a Swiss-based P2P lending and crowdlending platform headquartered in Switzerland. The company operates as a financial intermediary in the non-banking sector and is a member of PolyReg SRO, in compliance with Swiss financial regulations including AML, KYC, and GDPR. Maclear offers retail and qualified investors access to vetted business loan opportunities, with built-in risk assessment, a Provision Fund, and a Secondary Market for liquidity.

Disclaimer

The content of this article is provided for informational and educational purposes only. It does not constitute investment, financial, tax, or legal advice. P2P lending and crowdlending investments carry a risk of partial or total capital loss. Past performance is not indicative of future results. Liquidity on a secondary market is not guaranteed. Readers should conduct independent research and consult qualified advisors before making any financial decisions. Availability of products and services may be restricted in certain jurisdictions.