At the thought of pursuing enduring monetary growth, one cannot help but want to get investing – the dollar gets eroded every day by inflation, the indexes continue to abound, and one must devise a shrewd plan for one’s retirement somehow. But going gung-go right into the Wild West of stocks feels pretty scary at times for the casual observer.

Sharks truly do lurk these waters, and things get pretty volatile. You don’t want to just spend every waking hour watching securities or commodities like a soulless hawk either. Fortunately, the means exist to ride the flourishing waves of prosperous asset vehicles, negating the obligation to figure out the tides. Such is the promise dollar-cost averaging brings – a steady, stable, consistent method of growing your income while keeping negative scenarios at an absolute minimum. When your calendar reminder pings, you once again hit the purchase button, no matter the pricing, automatically scooping up additional stock.

Over months and years, those steady contributions soften the blows and sharp turns, cultivate a savings habit, and take emotion out of investing. Today, we’re going to break down how it operates, where it shines & fails, and why it remains a bedrock for everyone from fledgling 401(k) contributors to veterans navigating turbulent trends.

DCA 101

This idea is fairly straightforward, rendering it perfect for laymen. This concept goes like this – take a particular dollar quantity of shares, securities, commodities, or another financial vehicle, or a whole group of them, such as within the bounds of an index fund, and throw it in at a predetermined time interval.

The fact that you never waver from this schedule helps keep you cool. That said, you can still make adjustments and switch to other valuables over time once you see that you’re overinvested in one particular asset or another asset hasn't met your expectations after a long period of time.

The Magic

Far from all people possess the desire to slave down on charts or graph trends. You’re dealing with a job, bills, probably along with kids on top of that. Most people aren’t eyes-glued to Bloomberg all day. Which is precisely why such people are cut out for DCA.

Its biggest benefits:

Removes the timing off your plate: Most of us don’t know when the next crash or rally is going to happen. DCA says don’t worry about it. If markets are red or green, the plan stays the same regardless. This sturdy rhythm keeps people moving forward and prevents panic along with FOMO from occupying the driver’s seat.

Softens shock blows: Instruments bounce around – sometimes wildly. With DCA, you’re not betting the farm on a single price point. You’re spreading your risk over time. This can really pay off in bumpy markets. Instead of riding the highs and lows, you ride out the average.

Builds a long-term habit: Good investing isn’t about hitting home runs. It’s about showing up consistently. DCA aids you in doing that. That develops investing into a monthly habit, like paying rent or hitting a gym.

In Practice

Meet Bob. He endeavors to invest $300 month in, month out, into Russell 2000.

Observe a 4-month hypothetical scenario:

Month

ETF Price

Investment

Shares Bought

Jan

$187

$300

1.60

Feb

$180

$300

1.67

Mar

$158

$300

1.90

Apr

$186

$300

1.61

Total invested: $1,200 Total shares: 6.78 Average cost per share: $177

Even though the ETF went back up to $186 by April, your average cost is $177 – not bad.

Crowdlending

Another great avenue to profit-making is decentralized crowdlending, when you’re able to lend out money along with a group of other investors, thus smoothing out your risk. Besides that, some platforms organize collateral should a default occur. One such platform is Maclear.

Perfect DCA Matches

This isn’t ideal for everyone. But here’s when the technique of setting particular dollar amounts to acquire at predetermined intervals will pay off in spades:

You’re new in making investments. You get to dip the old toes in without overthinking every acquisition.

You’re building wealth slowly. This is perfect should you endeavor to use money out of a steady month’s salary.

Markets look unpredictable. And let’s face it – they usually are.

Stress aversion: DCA clears the path away from being drowned under the daily noise, allowing you to calmly stick to your pre-designed strategy.

Common Missteps to Watch for

Just because DCA is simple doesn’t mean DCA’s foolproof. Read below for some frequent mistakes to dodge:

Stopping after Assets Dip

This is when plenty of novices panic. In reality, this scenario is where DCA is actually doing its best work. Refusing to buy fresh stocks while they’re ripe for the picking at a low price? That’s the whole point.

DCA Into the Wrong Assets

It doesn’t magically fix a bad investment. Focus on quality – diversified index funds, bonds, or commodities with long-term growth potential.

Forgetting About Fees

Should you have to pay for each trade, frequent small purchases can chip away at your returns. Choose a broker offering rock-bottom or zero trading fees.

Big Bets vs. Steady Investments

Oh, that age-old financial dilemma – Should you dive in head-first betting big or take the tortoise strategy?

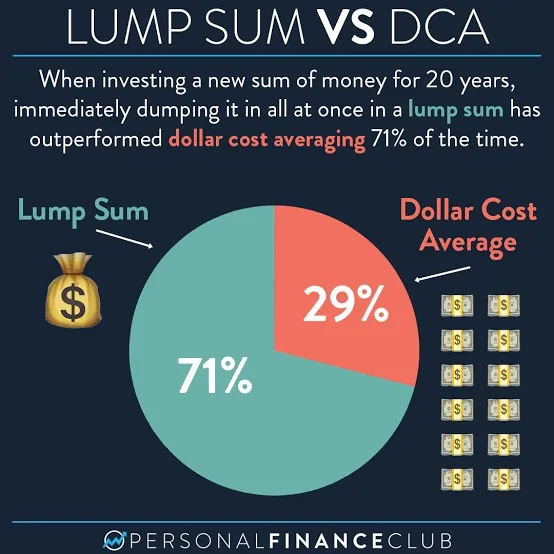

According to a Vanguard study, bold investing most often outperforms DCA in about two-thirds of cases, since year after year, assets mostly go up in value.

Still though, DCA remains a genius tactic for many types of people. Casual investors would simply like to make some money off of gold or steady big tech stock like Meta. The whole gist of the technique is that while it doesn’t have to turn you into a killer on the stock market, that’s not the goal. What it does is spur people from letting their money just depreciate with the value of the dollar over time, as it would in a savings account, and get them to increase the value of their net worth instead.

Automate It and Forget It

Most major platforms like Schwab provide you a medium to auto-invest on a set basis, so you don’t even have to worry about forgetting. If you’re a teacher that gets paid at the end of every month, and you like 300 dollars as your comfortable regular monthly purchase, and you like ICLN clean energy as you predict it to grow and it resonates with your values, tell them your plan, and they’ll automate it. Carbon Credits provided this year’s 5 best carbon ETFs.

This takes all the messiness and the busywork out of it.

Taxes

Each move you make to invest, you create a separate tax lot. If you sell later, you’ll need to track each lot’s cost basis. But don’t panic – most brokers handle this for you. And if you’re using a retirement account like an IRA or 401(k), those tax worries mostly disappear. Still, it’s worth checking with a tax advisor if you’re unsure.

Final Thoughts

The DCA investment strategy won’t make you rich overnight and there’s no one-size-fits-all strategy in investing. But if you:

Struggle with timing the market

Want to build a steady investing habit

Prefer a low-stress, long-term approach,

then the DCA investment strategy might be your best bet. It doesn’t promise overnight returns. But it works steadily, quietly, and consistently.

If you’re interested in keeping your risk measured and low in other ways yet gain the potential for major income via decentralized crowd lending online, Maclear offers you that opportunity with sophisticated credit scoring methods, collateral, and sharing investment burden evenly with other investors.