Peer-to-peer (P2P) lending has gained unimaginable popularity in recent years, offering traders the tempting possibility of getting a significant return on their own investments. But the common belief that high returns are necessarily associated with high risk is a misconception. This publication is dedicated to the aspects of P2P lending and also denies the position that great profitability is accompanied by significant risk. Having studied the mechanics of P2P lending as well as the various risk conditions, I will learn the reason why it is possible to strive for significant profitability without being afraid of exciting games together with high stakes.

The appeal of high yields in P2P lending

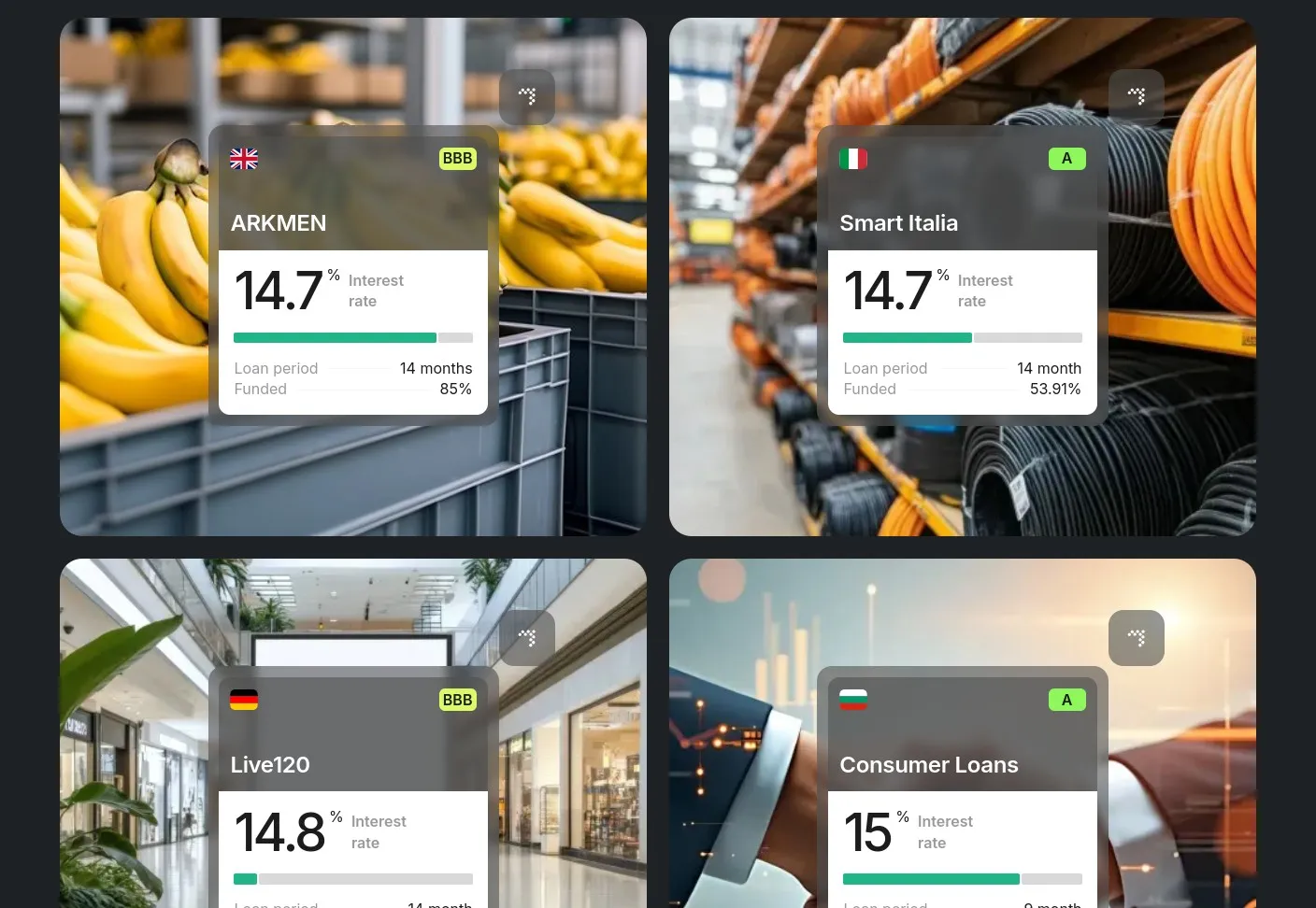

P2P lending is based on a simple premise: Individuals can directly provide loans to borrowers via an online platform, with the exception of classical banks as well as intermediaries. Such a straightforward relationship enables investors to choose loans that meet their risk appetite, which gives them the opportunity to acquire a significantly higher return compared to simple savings accounts or bonds. For example, if a classical bank is able to recommend an annual profit rate on savings provisions in the amount of 1-3%, in this case P2P-credits have all chances to give profit from 5% to 15%, and in certain variants even higher.

In order to understand why high profitability does not necessarily mean high risk, it is worth examining the risk assessment methods used by P2P platforms. Most of the influential P2P lending platforms thoroughly vet borrowers by assigning them plastic ratings that take into account conditions such as plastic history, income level, and existing obligations. Such control considerably reduces the danger of default, allowing traders to make weighty rulings about it, concentrating their own resources.

In addition, investors have all the chances to diversify their portfolios within P2P lending in addition, in order to increase security without harming profitability. By spreading investments across multiple loans, they have a chance to reduce the results of each individual default, similar to spreading a notch across different assets in a promotional portfolio. For example, instead of investing 1000$ in one profitable loan, the investor is able to choose ten loans according to 100$ each. Such a policy reduces possible losses associated with one borrower, and also proves the rule, according to which the greatest profitability is able to be won due to the result of rational distribution of money, and not frivolous speculation.

Another single approach that should be taken into account is the diverse qualification of P2P-lending. Many platforms work in the types of loans, which are usually characterized by the lowest degree of default, for example, loans to small businesses or plastic directions in the purchase of housing that can guarantee competitive profitability in the absence of significant risk. For the purpose of traders it is very important to perform a painstaking study of platforms and types of loans, primarily in comparison with investing their own capital.

To summarize, it is possible to note that great profitability, as well as the principle, attracts traders due to the ability to extract significant income, but it is important to realize that there are devices that can help to control the dangers in P2P-lending. The perception of this, as well as the evaluation of borrowers, strategic diversification as well as experimental information indicating the sustainability of the platform, have the potential to dispel fears as well as provide investors with the opportunity to take advantage of this innovative way of investing without entering the realm of gambling with high stakes.

Understanding P2P Lending

P2P lending platforms connect individual borrowers with lenders, bypassing traditional financial institutions. This innovative approach allows borrowers to access funds at competitive rates while offering lenders an attractive return on their investment. The yields in this environment can often exceed those of conventional savings accounts or CDs, leading many to view P2P lending as a compelling investment.

Deciphering the Relationship Between Yield and Risk

While it’s intuitive to associate high returns with high risk, this relationship doesn’t always hold true in P2P lending. Here’s why:

Risk Management Strategies

Many P2P lending platforms implement rigorous risk assessment procedures before approving loans. Platforms often assess borrowers’ creditworthiness through detailed analysis of credit scores, income verification, and debt-to-income ratios. By relying on data-driven decision-making, platforms can significantly reduce the risk of defaults. Consider a P2P platform that utilizes advanced machine learning algorithms to predict loan performance based on a vast array of data points; this can guide lenders in making informed choices that balance yield and risk.

Diversification Opportunities

One of the most effective strategies in P2P lending is diversification. Investors can spread their funds across multiple loans with varying risk profiles, mitigating potential losses from any single default. For instance, imagine investing $1,000 across twenty different loans of $50 each. Even if one borrower defaults, the potential impact on your overall investment is minimized. This calculated approach offers the potential for high aggregate yields without experiencing commensurate high risks.

The Role of Secured Loans

Not all P2P loans are unsecured. Some P2P platforms offer secured loans where the borrower puts up collateral, such as property or vehicles. This security provides an added layer of protection for investors. In the unfortunate event of a default, the lender can reclaim the collateral, thus reducing loss. Imagine funding a secured loan for home improvements; if the borrower cannot repay, you could potentially recover your investment by claiming the asset.

Market Demand and Trends

The demand for personal loans and small business financing continues to rise. P2P lending caters to this market, especially during economic fluctuations when traditional banks may tighten their lending criteria. As a result, even amid economic uncertainty, investors can tap into a pool of creditworthy borrowers seeking funds, sustaining high yields without significantly increased risk. For example, if a borrower demonstrates a strong business model and robust cash flow, investing in their venture via P2P lending remains a sound choice.

Investing Smartly in P2P Lending

To capitalize on high yields while mitigating risk in P2P lending, investors should do their due diligence. Analyzing the platform's track record, understanding the borrower’s financial background, and diversifying investments are key strategies for successful engagement in P2P lending. By focusing on these areas, investors can confidently pursue high returns without overexposing themselves to potential pitfalls.

Conclusion

The opportunity for high yields in P2P lending does not inherently mean high risk. By leveraging strong risk management strategies, diversification, and careful selection of loan types, investors can navigate the P2P lending landscape with confidence. This space not only democratizes access to capital but also creates a viable investment option for those seeking attractive returns. Don't let misconceptions deter you; dive into the world of P2P lending and explore the potential rewards awaiting you!