Why Institutional Investors Are Turning to Alternatives

07.05.2026

7

Pension funds, endowments, and insurers are reallocating from the 60/40 portfolio to private credit, infrastructure, and crowdlending — not because of a yield chase, but because long-dated liabilities require contractual cash flows that public markets no longer reliably provide.

Why the 60/40 model no longer fits an institutional mandate

The 60/40 portfolio — 60% equities, 40% bonds — became the default for one structural reason: when equities sold off, government bonds rallied and absorbed the loss. Through three decades of falling interest rates and disinflation, that relationship held. In 2022 it broke. Aggregate global bond indices declined 10–15% — the worst year for global bonds on record — while the S&P 500 fell more than 18% in the same year. The hedge that defined the model failed.

For an individual investor that is uncomfortable. For an institution it is a mandate problem. Pension funds, insurers, and endowments are not optimising for next year's return. They have liabilities that extend out twenty to forty years, and the volatility of the asset side has to be tolerable against the cash flows that have to leave the door each quarter.

How does inflation actually break the 60/40 hedge?

Stocks and bonds reprice against the same macro inputs — interest rates, inflation expectations, central-bank policy. In an inflationary tightening cycle, those forces push both asset classes in the same direction. The protective negative correlation flips positive precisely when capital preservation matters most.

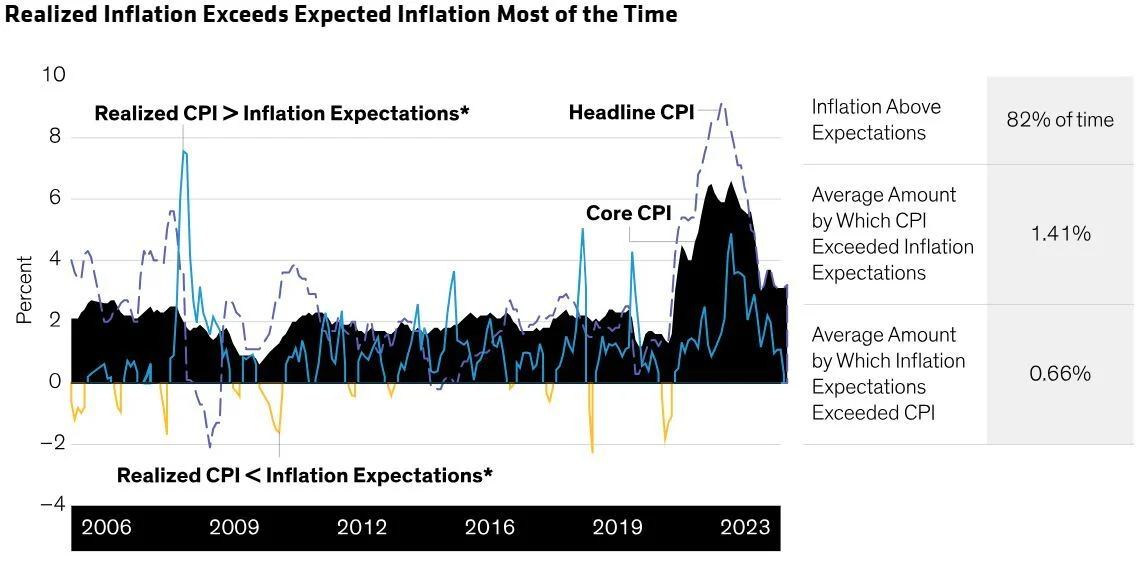

Realised inflation has run hotter than expectations 82% of the time since 2006, with an average overshoot of 1.41 percentage points. This is the macro environment in which traditional 60/40 hedging breaks down. Source: Bloomberg, BLS data 2006–2023.

BlackRock's investment strategy team has already flagged the structural problem and proposed a replacement framework. Their 50/30/20 model — 50% equities, 30% fixed income, 20% alternatives — explicitly carves out a fifth of the portfolio for non-correlated assets, and represents the direction institutional allocators are moving.

The 60/40 portfolio worked when bonds were a reliable hedge. The 50/30/20 framework assumes they no longer are — and reallocates accordingly.

The companion piece to this article — how alternative assets reduce portfolio volatility — covers the same problem from a private-investor lens. The institutional case adds two further dimensions: liability matching and the duration of capital.

How institutional risk management actually works

Institutions are evaluated on whether they can meet defined obligations within defined risk parameters — not on whether they beat a benchmark in any given year. That mandate has four practical implications, each of which favours assets that public markets do not produce.

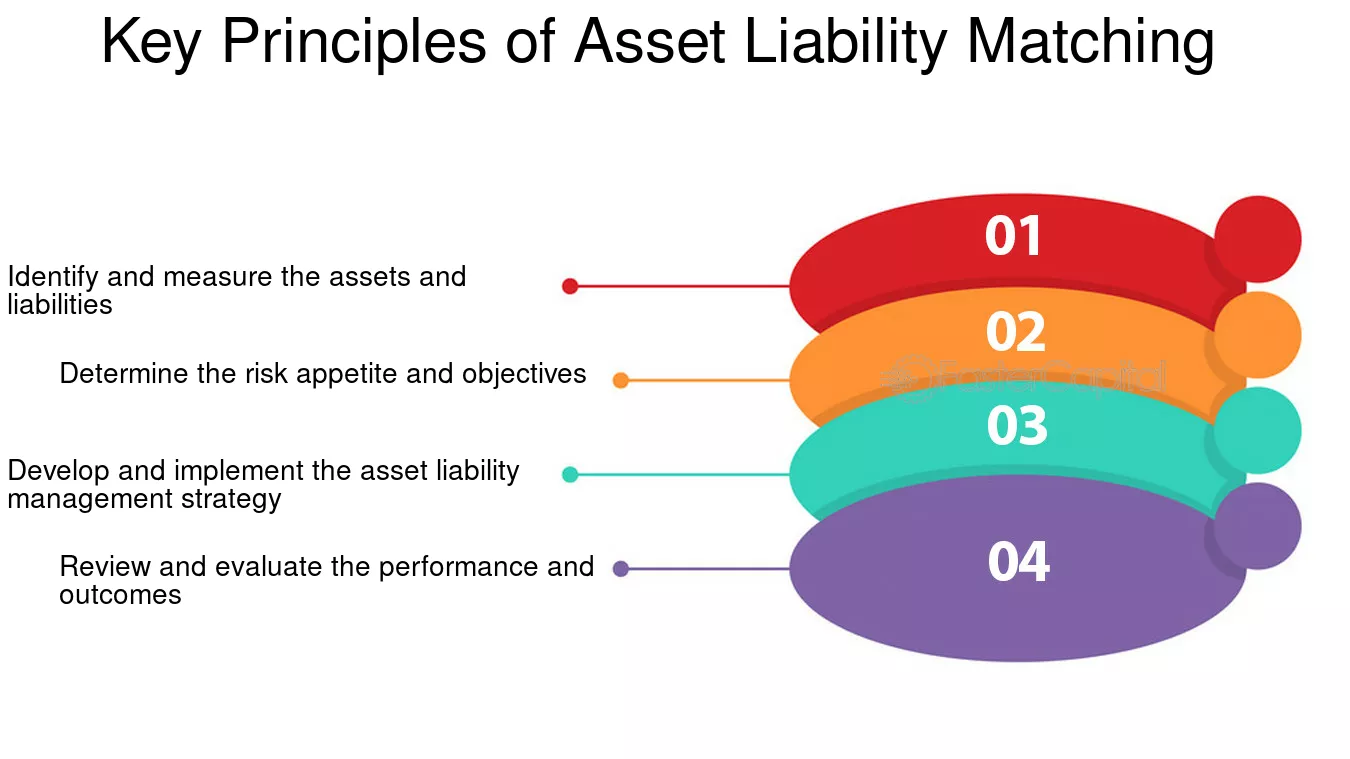

What is liability-driven investing?

Liability-driven investing (LDI) aligns the timing and nature of an institution's assets with the cash flows it must pay out — pensions, claims, endowment distributions. The four-step framework below is the one most defined-benefit pension funds and insurers operate inside.

The four-step asset–liability matching framework. Identify, define risk appetite, implement, and review. Source: Aurora Training Advantage.

Public equities introduce short-term volatility that complicates that match. Income-driven alternatives — private credit, infrastructure, and farmland — produce contractual or regulated cash flows, often inflation-linked, which fits the LDI mandate far better than mark-to-market public assets.

How is risk-adjusted return measured at the institutional level?

Institutional performance is measured with metrics like the funded ratio (assets ÷ projected liabilities), the Sharpe ratio (return per unit of volatility), and information ratio (active return per unit of tracking error). All three improve when the asset mix includes assets that are uncorrelated to public markets — which is the structural reason alternatives appear in every institutional model portfolio published by major asset managers in the last five years.

Why does illiquidity actually help institutional portfolios?

Long-dated liabilities allow institutions to commit capital for years without needing to liquidate. This converts illiquidity from a cost into a premium — what academics call the illiquidity premium. Assets that cannot be sold in a panic are also assets that do not get marked down in a panic. For a thirty-year liability, that volatility damping is more valuable than daily liquidity.

Why is capital preservation more important than upside?

Large drawdowns force institutions to crystallise losses, rebalance against rules, or report performance below covenant. The asymmetry is severe: a 50% loss requires a 100% gain to recover. Many alternative strategies are structured with downside protection in mind — collateral, seniority in the capital stack, or active risk management — precisely because the mandate is preservation, not maximisation.

Why contractual cash flows became the prize

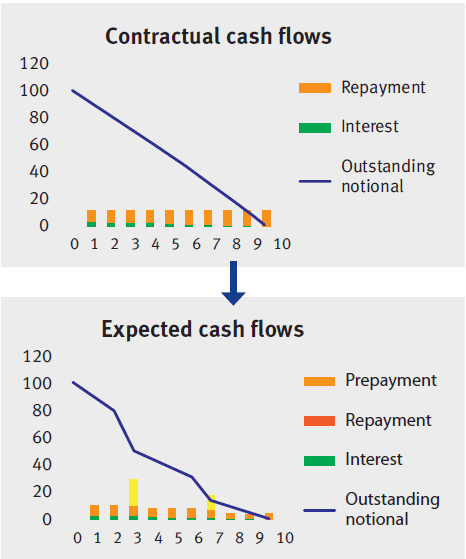

The single most cited reason institutional allocators give for reallocating into alternatives is the durability of income. Public-market dividends and bond coupons exist, but they are repriced continuously alongside the underlying instrument. A contractual cash flow from a private loan, an infrastructure concession, or a farm lease behaves differently — it accrues to the holder regardless of where the secondary market thinks the asset should trade.

Contractual versus expected cash flows on a private loan. Interest accrues regardless of market sentiment; prepayment timing affects the realised duration. Source: industry illustrative.

For an institution managing a stream of obligations, this matters in three concrete ways:

VisibilityContractual schedules let asset–liability planners forecast inflows quarter-by-quarter, reducing the reliance on capital appreciation that may or may not arrive when needed.

InsulationIncome from regulated infrastructure or senior secured loans is less sensitive to short-term sentiment, which dampens portfolio volatility through periods when public markets are repricing on macro headlines.

Inflation linkageMany alternative cash-flow assets — utilities, toll roads, lease-indexed real estate — embed inflation linkage directly into the contract. Given that realised inflation has exceeded expectations 82% of the time over the last 17 years, this linkage is not optional for a long-duration liability.

CompoundingWhen a meaningful share of returns arrives as cash income rather than mark-to-market gain, drawdowns become shallower and recoveries faster — because the cash flow continues to compound through the dip.

This is the same income-driven logic that underlies a sound diversification strategy at any scale. The institutional version is simply larger, longer-dated, and more rigorous about how the cash flow is sourced.

Which alternative asset classes do institutions favour, and at what scale?

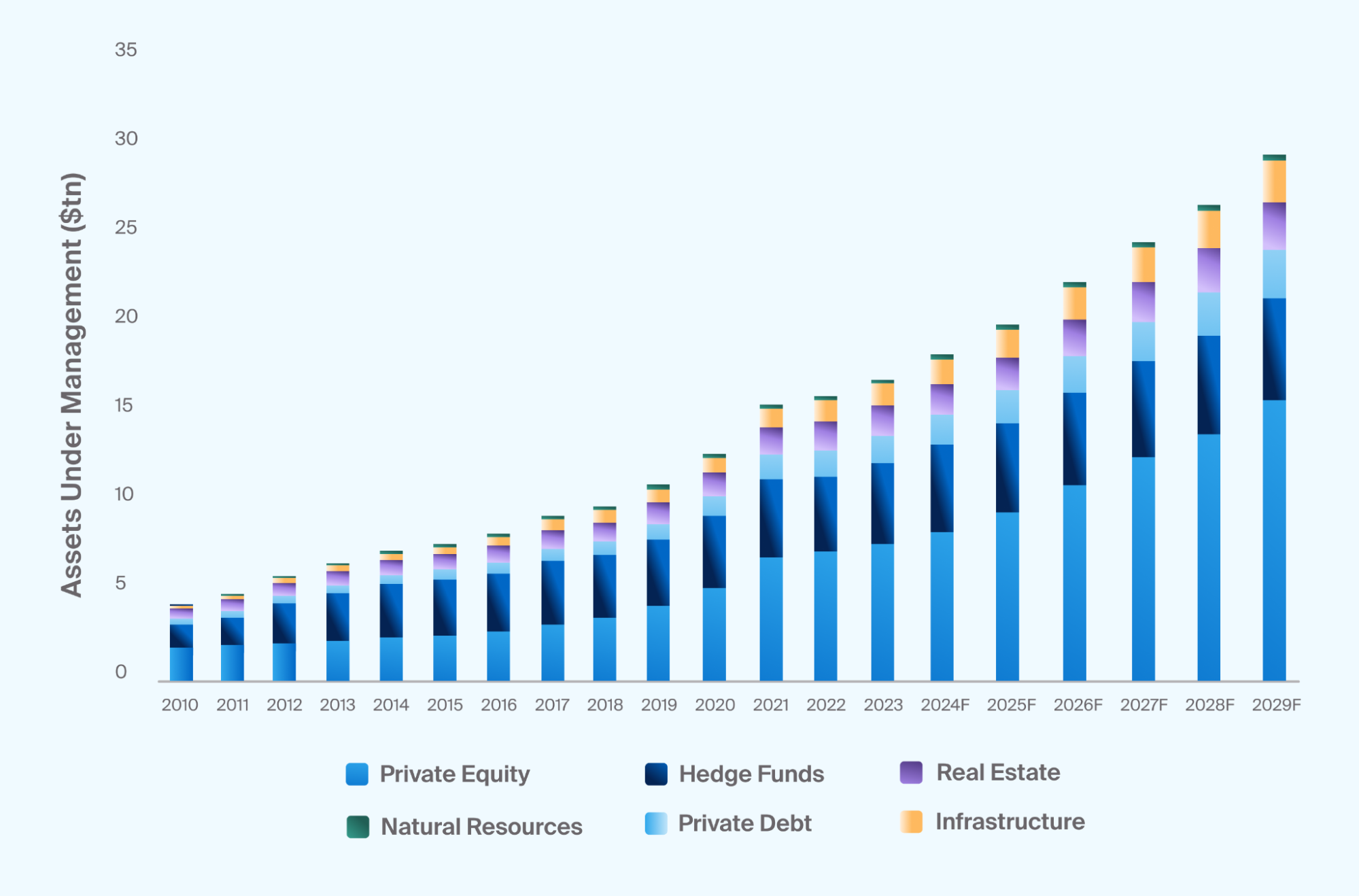

The reallocation is not a forecast — it is already in the data. Global alternative assets under management have grown from roughly $4 trillion in 2010 to over $20 trillion today, with industry projections approaching $30 trillion by 2029. Private debt and infrastructure have grown fastest, because their income profile is exactly what liability-driven mandates need.

Global alternative AUM by asset class, 2010–2029F (USD trillions). Private equity remains the largest category by AUM, but private debt and infrastructure are growing fastest. Source: Preqin / industry estimates.

~$20T

Global alt AUM today

~$30T

Projected 2029

82%

Of time inflation beat expectations (2006–23)

40–60%

Alts in major endowments & Canadian pensions

Allocations themselves vary by mandate. Large US endowments and Canadian pension plans hold 40–60% of portfolios in alternatives. Corporate pension funds and life insurers typically hold 15–30%. Sovereign wealth funds vary widely by jurisdiction. The direction across all categories is the same: up.

What are the six categories institutions allocate to?

"Alternatives" covers six broad categories at institutional scale. They serve different roles inside a portfolio — and an institution typically allocates across several rather than concentrating in one.

Equity ownership

Private equity

Buyouts, growth equity, secondaries. Returns generated through operational improvement and strategic execution rather than public-market multiple expansion. Long lock-ups, but historically the highest expected return inside the alternatives bucket.

Contractual lending

Private credit

Direct lending to mid-market businesses, asset-backed lending, specialty finance. Floating-rate, often senior secured. The fastest-growing alternatives category since 2015 — driven by exactly the income profile institutions need.

Direct private lending at retail scale

Crowdlending

A private-credit instrument structured for direct investor access. When the platform applies institutional discipline — collateral, structured underwriting, tranche release, recovery — the return profile mirrors private credit at smaller ticket sizes.

Long-duration real assets

Infrastructure

Utilities, toll roads, energy transmission, data infrastructure. Long-duration concession revenue, often regulated and inflation-linked. A near-perfect liability match for pension funds with 30-year obligations.

Income-producing real assets

Real estate & farmland

Rents and lease income, often with inflation pass-through. Demand for housing and food production is structurally inelastic, which dampens cyclical volatility relative to listed REITs.

Absolute return

Hedge funds

Market-neutral, arbitrage, macro, and event-driven strategies. Used primarily as a diversifier rather than a return engine. Highly manager-dependent — outcomes depend more on selection than on category exposure.

Of the six, private credit and infrastructure carry the strongest fit for an LDI mandate, because both produce contract-anchored cash flows over multi-year horizons. Crowdlending, when properly structured, sits inside the private-credit category at smaller ticket sizes — making it accessible to allocators that cannot underwrite a single $50 million private loan but want the same return drivers.

How does a 20% alternatives sleeve actually shift portfolio volatility?

The math is straightforward. Replacing public-market exposure with assets that have low correlation to the existing portfolio reduces total variance, because the cross-term in the variance formula shrinks when correlation is low.

Worked example — illustrative only

Volatility of a 60/40 versus a 50/30/20 (alts at ρ = 0.2)

Allocation

Composition

Estimated portfolio volatility

Baseline

60% equities · 40% bonds

~10.0%

BlackRock framework

50% equities · 30% bonds · 20% alts

~8.3%

Endowment-style

40% equities · 20% bonds · 40% alts

~7.1%

Inputs: equity vol 16%, bond vol 6%, alts vol 5%, equity–bond correlation 0.4, alts–public correlation 0.2. Estimates only — actual outcomes depend on the specific instruments, weights, and realised correlations.

The volatility reduction does not come from the alts being safer in absolute terms. It comes from low correlation: a 5% volatility asset that moves independently of the rest of the portfolio reduces total variance more than a 4% volatility asset that moves with everything else.

How Maclear brings institutional discipline to crowdlending

The benefits described above only materialise on platforms whose structure matches the theory. A crowdlending platform that under-prices risk, skips collateral, or has no recovery mechanism does not behave like private credit — it behaves like an unsecured high-yield position. Institutional allocators do not buy that, and individual investors looking for institutional-style cash-flow exposure should not either.

Swiss-based Maclear is built specifically around the discipline institutional allocators apply to private credit. Four elements define how Maclear manages risk:

Disciplined underwriting

Every borrower runs through Maclear's published AAA-to-D borrower scoring system, modelled on international credit-agency standards, and is assigned an internal risk score on a 1–10 scale before being released to investors.

Two-layer protection

Each Maclear loan is backed by reserved collateral. A separate Provision Fund — formed from project commissions — sits behind that, designed to cover temporary repayment difficulties before they touch investor returns. The Provision Fund is not a buyback guarantee on individual claims.

Staged capital deployment

Maclear loans release in defined tranches. Performance on each tranche is observed before the next is released — so investors compound exposure into projects already proving themselves.

Cross-border recovery

In the event of default, Maclear acts directly as the collateral recovery agent and manages legal proceedings across jurisdictions on behalf of investors. Recovery is part of the platform, not outsourced.

The combined effect is a return profile that lives on the income-driven side of the alternatives spectrum: contractual interest, defined repayment schedule, collateral, and a manager who acts when something goes wrong. That is exactly the profile institutional allocators look for when sizing private credit. The mechanics — fees, scoring, Provision Fund, Secondary Market — are documented in the Maclear FAQ knowledge base.

Spotlight — Maclear AG

Swiss-based crowdlending with institutional-grade discipline

Maclear AG is a Swiss-based P2P lending and crowdlending platform that operates as a financial intermediary in the non-banking sector under Swiss financial regulations and is a member of PolyReg SRO. The platform focuses on European business loans — borrowers, jurisdictions, and recovery options spread across Europe so that a single-country shock does not concentrate losses.

Each project is graded, collateralised, and offered to investors in tranches with full transparency on terms, grade, and repayment schedule. Returns come from contractual interest payments — not from market repricing.

The 60/40 portfolio assumed bonds would hedge equities. In 2022 both asset classes fell together (bonds 10–15%, S&P 18%+) and the assumption broke. Institutions need a new framework — most large allocators are moving toward a 50/30/20 mix or further.

Institutional mandates are defined by long-dated liabilities, not annual returns. Liability-driven investing (LDI) requires assets that produce contractual or regulated cash flows — exactly the profile that public markets no longer reliably deliver.

Global alternative AUM has grown from roughly $4 trillion in 2010 to over $20 trillion today, with $30 trillion projected by 2029. Private debt and infrastructure are growing fastest because their income profile is the closest match to liability-driven mandates.

Realised inflation has exceeded expectations 82% of the time since 2006, with an average overshoot of 1.41 percentage points. Inflation-linked income from infrastructure, real estate, and floating-rate private credit is no longer optional for long-duration portfolios.

A 20% alternatives sleeve at ρ = 0.2 trims roughly 17% off a 60/40 portfolio's volatility. The reduction comes from low correlation, not from individual-asset safety.

Crowdlending fits inside the private-credit bucket — but only when the platform applies institutional discipline: collateral, structured underwriting, tranche release, and active recovery. Maclear's Swiss-based platform is built around exactly that discipline.

Frequently asked questions

Why are institutional investors moving away from the 60/40 portfolio?

The 60/40 portfolio relies on bonds rallying when equities fall. That negative correlation broke down in 2022, when global bond indices fell 10–15% alongside an 18%+ equity drawdown. Institutions also face long-dated liabilities that public-market repricing makes difficult to match, which is why they are reallocating to private credit, infrastructure, and other contractual cash-flow assets.

What allocation to alternatives do institutional investors hold?

Allocations vary by mandate, but global alternative AUM has grown from roughly $4 trillion in 2010 to over $20 trillion today, with industry projections approaching $30 trillion by 2029. Large endowments and Canadian pension plans hold 40–60% of their portfolios in alternatives; corporate pension funds and insurers typically hold 15–30%.

What is liability-driven investing and how do alternatives fit?

Liability-driven investing (LDI) aligns the timing and nature of an institution's assets with the cash flows it must pay out — pensions, claims, endowment distributions. Public equities introduce short-term volatility that complicates that match. Income-driven alternatives such as private credit, infrastructure, and farmland produce contractual or regulated cash flows, often inflation-linked, which fits the LDI mandate better than mark-to-market public assets.

Which alternative asset classes do institutions favour most?

The largest categories by global AUM are private equity, hedge funds, real estate, private debt (including direct lending and crowdlending), infrastructure, and natural resources. Private debt and infrastructure have grown fastest in the last decade, driven by their contractual income profile and inflation linkage — the two features institutions need most in the current macro regime.

Is crowdlending suitable for institutional-style portfolios?

Crowdlending is a form of private credit. It is suitable for institutional-style portfolios when the platform applies institutional-grade discipline — collateral, structured underwriting, staged capital deployment, a provision fund, and active recovery. Without those, crowdlending behaves like an unsecured high-yield position. Maclear's Swiss-based platform is built around exactly that discipline.

Does Maclear guarantee returns or buyback?

No. Maclear does not offer a buyback guarantee, and returns are not guaranteed — they depend on borrower performance. Maclear mitigates risk through collateral, a Provision Fund (a reserve formed from project commissions used to cover temporary repayment difficulties), and continuous borrower monitoring. The Provision Fund is not a buyback guarantee on individual claims.

Is Maclear regulated by FINMA?

No. Maclear AG is a Swiss-based platform that operates as a financial intermediary in the non-banking sector under Swiss financial regulations. Maclear is a member of PolyReg SRO and complies with AML, KYC, and GDPR requirements. A FINMA Fintech License is part of the company's future plans, not its current status.

About Maclear

Maclear AG is a Swiss-based P2P lending and crowdlending platform headquartered in Switzerland. The company operates as a financial intermediary in the non-banking sector and is a member of PolyReg SRO, in compliance with Swiss financial regulations including AML, KYC, and GDPR. Maclear offers retail and qualified investors access to vetted business loan opportunities, with built-in risk assessment, a Provision Fund, and a Secondary Market for liquidity.

Disclaimer

The content of this article is provided for informational and educational purposes only. It does not constitute investment, financial, tax, or legal advice. P2P lending and crowdlending investments carry a risk of partial or total capital loss. Past performance is not indicative of future results. Liquidity on a secondary market is not guaranteed. Readers should conduct independent research and consult qualified advisors before making any financial decisions. Availability of products and services may be restricted in certain jurisdictions.

Ready to access institutional-style private credit at retail scale? Browse Maclear's current projects — each with full grading, collateral details, and tranche structure.