How Digital Identity Will Reshape Credit Scoring and Lending

18.09.2025

4

If you’ve ever applied for a loan or checked your credit score, you have probably felt the frustration of a system that seems stuck in the past. Maybe you’ve always paid your rent on time, covered your utility bills like clockwork, or sent money home regularly, but it turns out none of that counts toward your creditworthiness. That’s because the traditional credit system primarily focuses on a narrow set of financial behaviors. But this is starting to change, thanks to something called digital identity.

Digital identity isn’t about tech buzzwords or futuristic promises. Instead, it’s about bringing your real-world behavior into the conversation. It’s about recognizing that you’re more than just your credit card history or the length of your mortgage. And as more lenders start to embrace this broader picture, we’re likely to see a big shift in how borrowing works for millions of people.

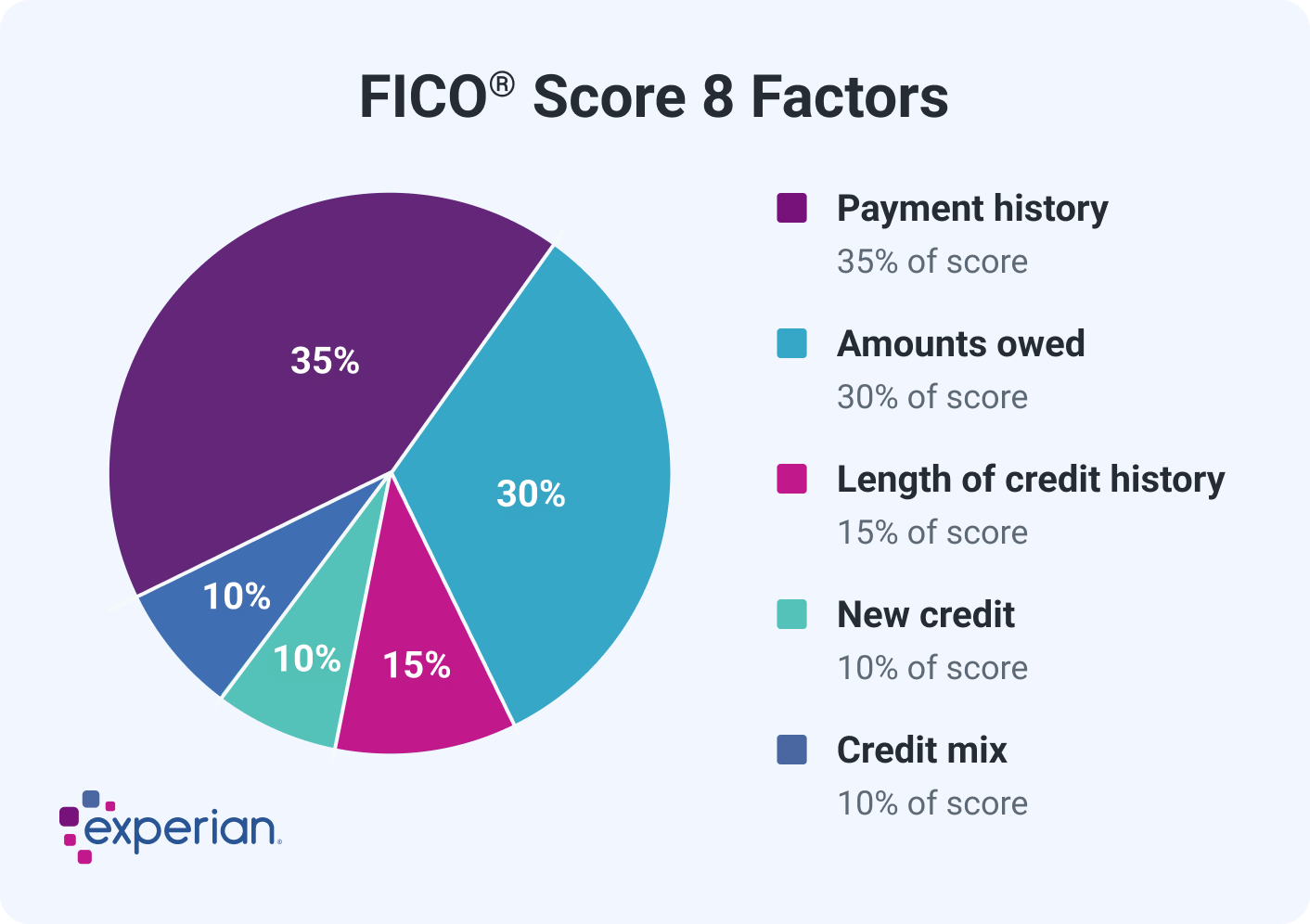

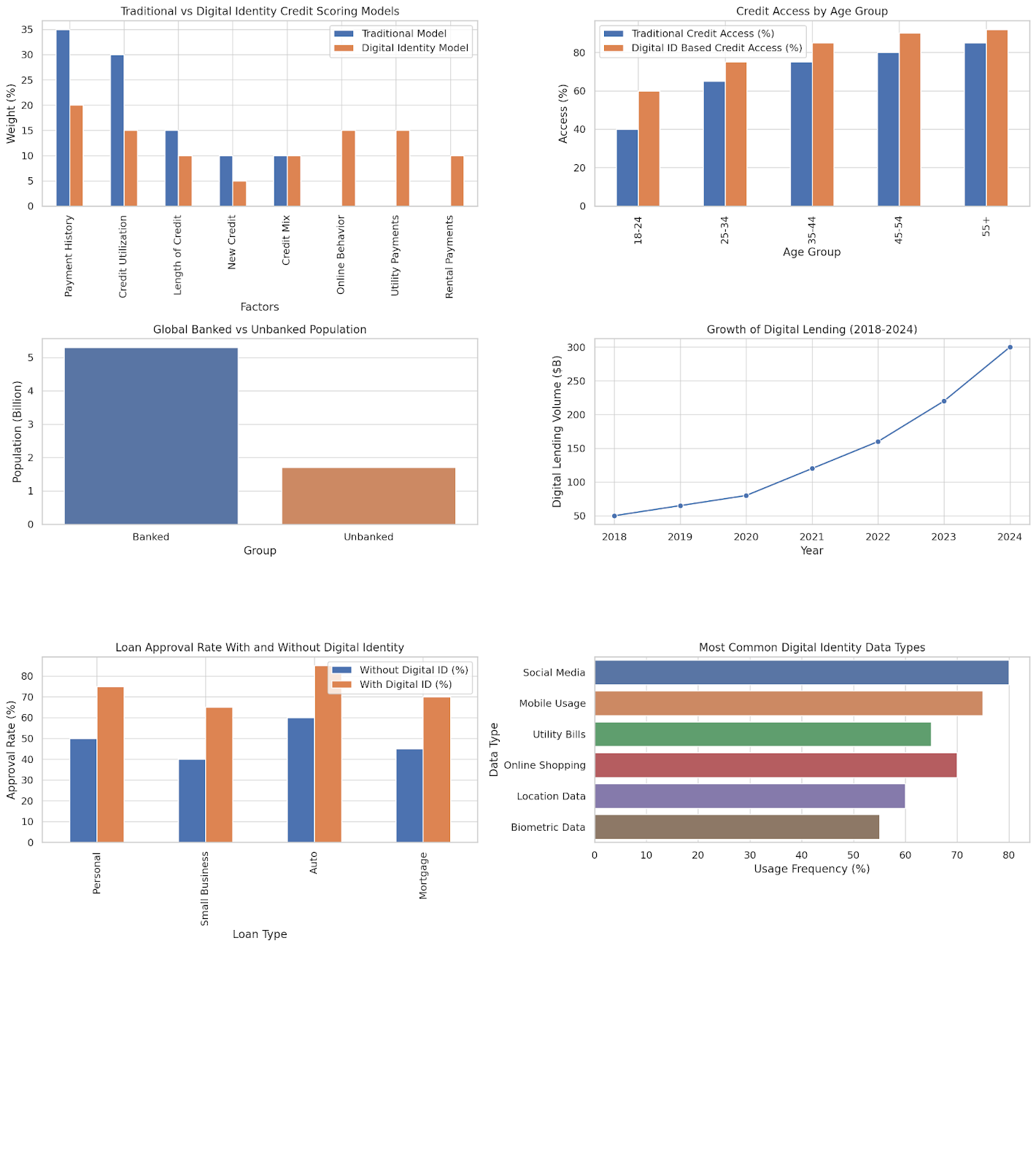

In the traditional model, your credit score is made up of just a few key factors, which High Radius broke down in detail. These include payment history, credit utilization, length of credit, new credit applications, and the combination of accounts you have. Good luck getting a decent score if you are young or haven't used much credit before. It’s an uphill task no matter how responsible you are.

Payment history and credit utilization make up a whopping 65% of your score. But what if you always pay your rent on time or consistently top up your phone and data plans? Those don't count. At least not yet.

Digital Identity Expands the Picture

Now imagine a model that includes your mobile phone payments, utility bills, rent history, and even your online financial behavior. That’s where digital identity comes in.

The chart above shows a comparison of how much weight traditional credit scoring places on limited data versus how digital identity models spread that weight across a broader set of behaviors. In the digital model, things like mobile payments and rental history aren’t ignored. Far from it – they’re actually central to it.

This expanded view makes it possible to evaluate people more fairly, especially those who’ve traditionally been left out of the system.

Credit Access by Age Group

Young adults between 18 and 24 often take the greatest hit. They haven’t had time to build credit, but that doesn’t mean they’re irresponsible with their money. The chart below shows that only 40% of people in that age group have access to traditional credit products. But when you factor in digital identity, that number jumps to 60%.

For the 25-34 group, digital identity lifts access from 65% to 75%. That’s a major shift; one that could lead to more financial independence earlier in life.

The Global Picture: 1.7 Billion Still Left Out

Let's now examine people all over the Earth from a wider angle. There are still over 1.7 billion unbanked persons in the globe. This indicates that they lack access to official financial systems and a bank account.

That is a sizable population, and a large portion of them do own phones, utilize mobile money, and make frequent payments. They just don’t have a paper trail that traditional credit scoring can use. Digital identity helps bridge that gap, pulling in data from their day-to-day lives and giving them a financial voice. The World Economic Forum broke down the limitations being unbanked causes for regions.

The Rise of Digital Lending

As you might expect, digital lending is already growing fast. Far back in 2018, it was a $50 billion industry. By 2024, it’s projected to hit $300 billion. A big part of that growth comes from expanding credit access to people who were previously invisible to banks.

This isn’t just happening in the U.S. or Europe. In countries like Kenya, Colombia, and India, digital lenders are using mobile data and payment history to assess loan eligibility. And it’s working. In fact, investors are starting to replace banks in terms of providing lending. One of the rising media for doing so is crowdlending.

In this case, a bunch of investors share the risk in investing in a particular project while enjoying quite lucrative interest rates. One such platform is Maclear, which also safeguards such investments by way of collateral.

Better Approval Rates

Higher loan approval rates are one of the most significant benefits of digital identity.

Varying approval rates exist for different types of loans. For personal loans, the rate jumps from 50% without a digital identity to 75% with it. For small business loans, it’s even more dramatic, skyrocketing from 40% to 65%.

This absolutely matters. People can start businesses, buy vehicles, or cover emergencies without jumping through endless hoops. This means that the credit system will become a little more humane.

What Kind of Data Are We Talking About?

So what exactly goes into a digital identity?

Social media activity

Mobile usage

Utility bills

Online shopping habits,

Location data

Biometrics.

None of this data is particularly new, but the way it’s being used is. Instead of focusing only on debt and repayment, lenders are looking at patterns of consistency and responsibility across a range of behaviors.

Without a doubt, there are privacy concerns. Not everyone is comfortable with their phone usage or online shopping habits being factored into a loan decision. But with the right safeguards, this kind of data can open up new opportunities, especially for people who’ve never had access to traditional credit.

Real People, Real Experiences

Think of a freelance designer who earns income irregularly but always pays her phone and internet bills on time. Or a delivery driver who’s never missed a rent payment but doesn’t have a credit card. In the old system, they are ghosts. However, in the new one, they are creditworthy.

That’s what digital identity really changes. It doesn’t just give banks more data; it gives people a chance to be seen.

Additionally, If you want proof that this works, look at Kenya. Platforms like M-Pesa and Tala have changed the game. Millions of people now access credit via mobile phones, with decisions made based on mobile usage, repayment patterns, and even contact list stability.

And it is working. Small businesses are growing. Emergency needs are met without borrowing from friends or loan sharks. And the repayment rates? They are surprisingly high.

Challenges and What Comes Next

It’s not all smooth sailing, of course, otherwise, we’d be building castles in the air. There are questions around data accuracy, consent, and standardization. How do we make sure the information being used is fair and verified? Who decides what behaviors are considered “creditworthy”? And what happens if someone’s phone gets stolen or their digital footprint is incomplete?

Regulators are still figuring that out. However, the direction is clear: digital identity is becoming a crucial part of understanding financial behavior. It’s not about replacing the old model. Instead, it is about improving it.

What Else Can Change?

When your digital identity becomes part of your financial life, credit scores are just the beginning. Here’s what else could change:

Faster loan approvals: Lenders can process your application in minutes, not days.

Fairer interest rates: If you’re low risk, your rate should reflect that—even without a credit card history.

Global mobility: Imagine being able to prove your creditworthiness when you move to another country, just using your digital profile.

More personalized offers: Lenders can tailor products to your behavior, not just your income.

A More Inclusive Future

At its core, lending is about trust. And trust is built on knowing someone’s story, and not just their score. Digital identity helps tell that story in full. It opens the door to millions of people who’ve been shut out, not because they’re risky, but because the system hasn’t figured out how to read their lives. It gives lenders a better way to understand risk, and borrowers a fairer chance to succeed.

If we get it right, this shift could reshape credit and lending in a way that feels more human. We’ll achieve this; one mobile bill, utility payment, and digital footprint at a time.

If you’re interested in taking advantage of your own digital identity for credit or you’d like to profit off of investing in crowdlending, Maclear is one of the front-running vehicles to do so wherever you are in the globe.