How Technology Is Powering the Growth of Peer-to-Peer Lending Platforms

02.09.2025

5

Updated:

29.07.2026

Borrowing money should be as simple as texting a friend who never leaves you on “read”: no piles of paperwork, no hordes of bank tellers, just a few clicks and a promise struck between strangers. That's the promise of P2P lending.

Peer-to-peer lending is changing modern finance and closing the distance between the haves and have-nots. It's guiding us towards a new age of financial access for everyone. Let's highlight how technology is helping drive this growth, a fact that's changing what was once an esoteric concept into a global phenomenon.

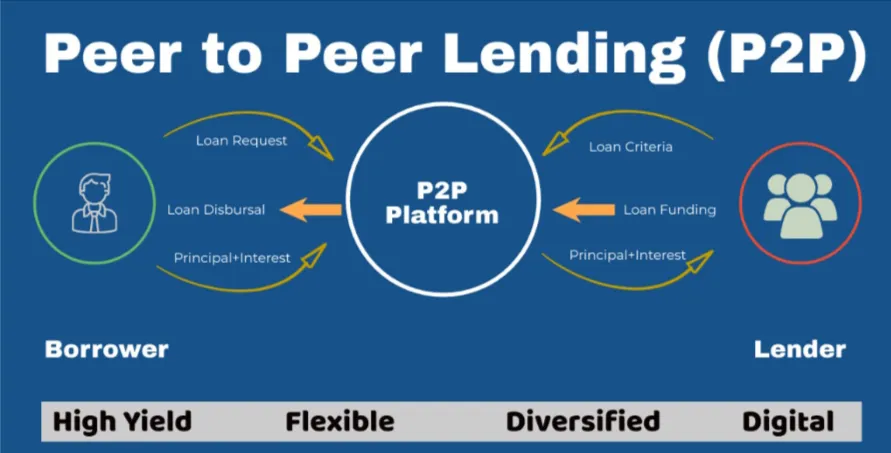

P2P lending promises less expensive interest rates for borrowers and better returns for investors by eliminating intermediaries.

Although it may seem new, the peer-to-peer or P2P lending concept is as old as sliced bread. Throughout history, people have borrowed from each other, their neighbors in villages and tight communities, relying on connection and trust. However, the Internet age has transformed this ground-level tradition into a global marketplace.

In the mid-2000s, Zopa, Lending Club, and Prosper went online and immediately became a new alternative to bank-based lending. As you would expect, the early days of P2P lending were modest and constrained by technological challenges and skepticism.

That all changed when technology-driven conveniences took center stage in society, especially after the post-2008 financial crisis that diminished trust in traditional financial systems.

When P2P lending and borrowing platforms went mainstream during this period, they positioned themselves as transparent, democratic alternatives to traditional borrowing and lending. However, the idea's uptake really skyrocketed when technology finally caught up with the ambitious idea behind P2P lending.

Building Bridges In A Digital Landscape

P2P lending is all about matchmaking on the back of technological advancements.

The algorithms that run P2P systems are like matchmakers connecting lenders and borrowers based on financial history, loan purpose, and risk appetite.

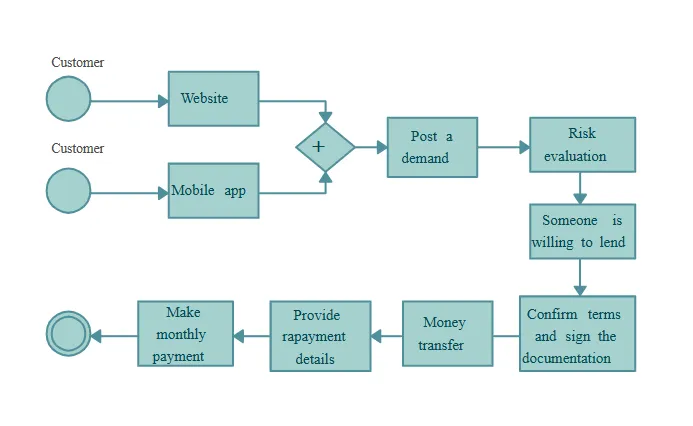

Thanks to advanced cloud computing, automated credit scoring, and secure payment gateways, it's easy to scale P2P platforms to a point where one system can handle millions of daily transactions without crashing. These systems replace hour-long manual checks with automated verifications that happen in seconds, thanks to API integration with credit bureaus and payment gateways.

Efficiency is not the only magical aspect of P2P lending platforms. The best thing about them is their accessibility. For example, investors in Tokyo can now provide microloans to Kenyan farmers, and numerous lenders from different parts of the world can stake small amounts to facilitate education for Brazilian students.

The P2P technology eliminates geographical boundaries and makes the world a village where ideas and money thrive in a peer-to-peer setting. One of the front-running DeFi crowdlending platforms is Maclear, which offers collateral backing for investors, lucrative profits, and more accessible loans than before for promising borrowers.

5 Technologies Powering The Growth of Peer-to-Peer Lending

Here are the technologies driving the bullish growth of P2P lending:

AI and Machine Learning

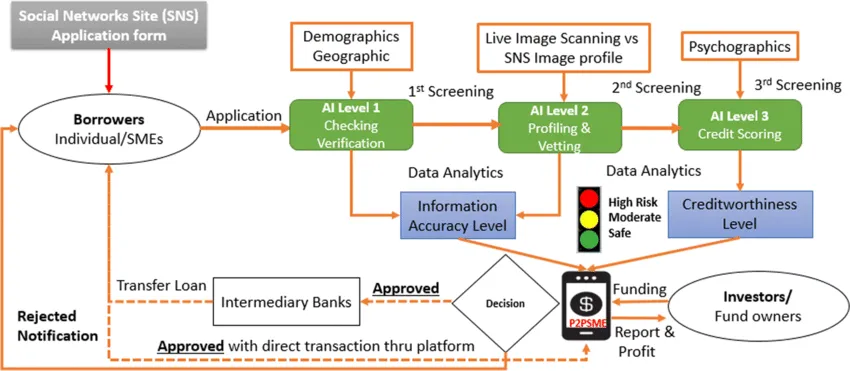

Risk assessment is crucial in the lending business. Traditional banks use credit ratings, a flawed system, particularly for the “unbanked”.

P2P sites, on the other hand, use machine learning and artificial intelligence to provide a more comprehensive perspective.

AI algorithms predict trustworthiness with surprising accuracy by scouring thousands of data points, from social media activity and online shopping behavior to smartphone usage patterns.

Consider a gardener who has studied the dirt, seasons, and weather to understand what crops would do well.

That's what machine learning does for P2P loans: AI detects small patterns like how quickly borrowers pay their power bills, the steadiness of their work history, etc.

These algorithms learn and improve over time, which helps shield lenders and minimize loan defaults. The outcome is lower investor losses and cheaper interest rates for solid borrowers.

Blockchain and Smart Contracts: Trust Coded into Every Transaction

In online settings, trust is tenuous.

P2P gets around this by using blockchain technology to generate transparent, tamper-proof records. All loans, payments, and exchange agreements are on a decentralized ledger that no one can change. This openness generates trust and discourages deceit.

Then there are smart contracts, self-executing agreements that enforce themselves and only go into effect upon meeting certain terms.

Think of a vending machine. The contract initiates payments upon receiving collateral. Likewise, when a borrower misses a payment, the contract terms mechanically change to reflect that. No waiting, no lawsuits.

Big Data and the Art of Personalization

Big data is the unsung hero of P2P lending platforms. Quantity is important, but so is perspective.

P2P lending platforms can customize loan offerings to the requirements of each individual by consolidating data from hundreds of sources, such as:

bank statements;

online transactions;

marital status;

dependents

educational attainment.

For example, the system can offer a freelance graphic designer a repayment plan with some accommodation based on project revenues. Similarly, a small business owner can obtain a loan offer that adequately accommodates seasonal cash flow.

Lenders also benefit from this customization by filtering lending opportunities based on industry, social impact, or risk level for investors. Want to back women entrepreneurs or invest in green energy projects? It's big data that enables it. Iron-air batteries by Form Energy can store energy for 100 hours.

As a result, financial decisions are context-bound rather than based on just credit scores, leading to a more compassionate system.

Mobile Technology

P2P lending is a pocket-sized service. Due to the prevalence of smartphones, customers can check investments, transfer money, or apply for loans through mobile apps during their commute or over their morning cup of Joe.

Mobile technology is nothing less than revolutionary in less developed countries that struggle with poor banking infrastructure. Companies such as Tala and Branch use smartphone data to determine creditworthiness and provide loans to individuals whom banks might overlook.

Lenders receive push notifications when borrowers reach milestones, and chat functionality provides direct communication between counterparts. This turns modern finance into a conversation instead of a transaction.

Regulatory Technology

With growth comes regulation. P2P platforms operate under loan provisions, data privacy laws, and anti-money laundering laws.

Along comes RegTech, or compliance automation technology, where algorithms monitor for red flags in deals, digital IDs check users' identity, and real-time reporting software alerts authorities.

Regulations vary globally, but technology allows platforms to adhere across the board. Within the EU, open banking laws enforce the secure sharing of financial data—a challenge resolved via encrypted APIs.

For example, Aadhaar's biometric identity makes KYC verification simpler in India. RegTech ensures that innovation does not outstrip responsibility.

Challenges and the Way Forward

That said, there are bumps along the way. They include:

Although declining, default rates still exist.

Uncertainty in regulation is a concern in certain territories.

Cybersecurity threats demand vigilant attention to detail at all times.

Critics also say that as P2P lending platforms proliferate in the market; 'faceless' finance can lose its sense of community.

Yet the trend is encouraging.

Breakthroughs in quantum computing may transform risk modeling. P2P lending and DeFi can merge to form completely independent networks. Ethical AI projects can also help eliminate bias and promote inclusive and equitable lending.

Conclusion

Peer-to-peer lending is a testament to human ingenuity and is more than just a financial tool. Besides powering its expansion, technology has also given it new potential.

P2P websites remind us that, at its core, finance is human by bringing together data and empathy, algorithms, and trust. One thing is certain as we move through this changing landscape: stark, marble banks are not the future of lending. The future of lending is P2P.