The snowball effect: How reinvesting income accelerates wealth building

10.06.2025

5

Attaining and preserving wealth has always been about being clever and aware of the opportunities available. You either overachieve in your profession or invest to make money work for you. You might not see the magnitude of the results right out the gate, but reinvesting your extra dough makes your wealth snowball in a surprising way.

This article shows how small, regular investments can evolve into a big portfolio. You’ll learn easy methods, such as dividend reinvestment plans, automatic transfers, and budgeting apps. We’ll also show you how to track your progress with a simple spreadsheet.

Follow these steps to set up automatic investments, stick to your plan, and see your cash grow more quickly than you expected.

This is when the banknotes you earn, like dividends, interest, or savings, are reinvested to create more cash for you over time. Think of it like a snowball rolling down a hill. It starts small but grows bigger and faster as it picks up more snow.

Making small, regular investments are able to become a large sum because of this “compounding” power. Reinvesting your earnings is important as it speeds up growth, while spending gives you instant gratification, but leaves nothing for the future.

How It Works in Personal Finance

When you reinvest your earnings, you earn returns not just on your original funds, but on the returns themselves. Rather than spending on things in the vein of luxury purses or suits, you could grow your wealth instead by reinvesting, such as via dividends from buying more shares.

You need to be patient, as time and regular contributions matter. The longer you leave your cash invested and the more you add to it, the faster your accumulation grows. For instance, reinvesting dividends for ten years might easily double or triple what you began with. Angel Stock depicted how long to hold assets.

The Power of Compound Growth

Compound growth is the true power behind the snowball effect, thanks to earning a percent on both your initial funds plus the interest you’ve already earned at the same time. The math behind it is explained in this formula: A = P (1 + r/n)^(nt).

A = total money you’ll have

P = initial amount (say, $10,000)

r = yearly percent rate (e.g., 5% or 0.05)

n = how often interest is added (monthly, yearly, etc.)

t = number of years

For example, if you invest $10,000 at 5% once a year for 3 years, you’ll earn $1,576.25 in interest.

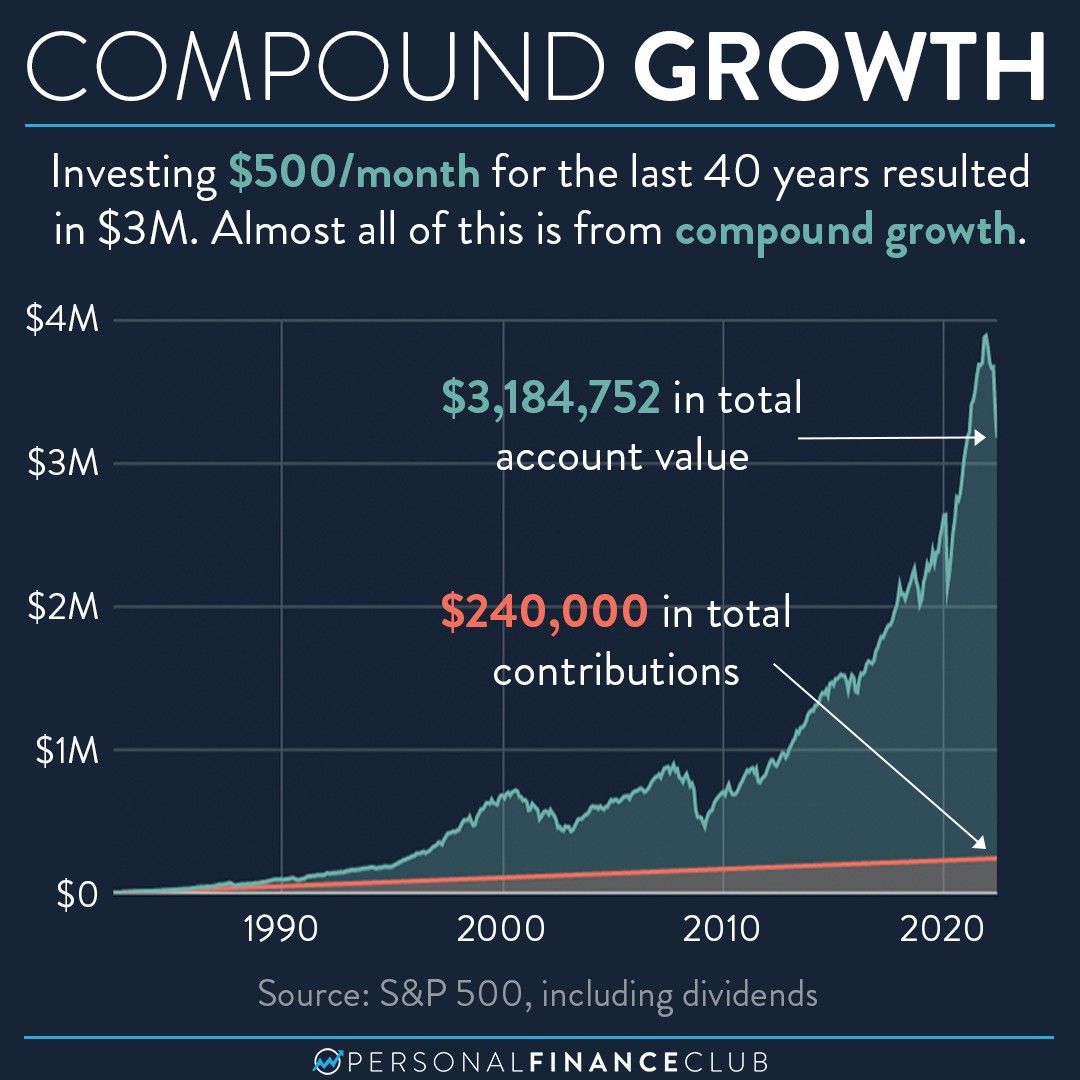

How often interest is added matters. Monthly compounding gives more dough over time than yearly compounding. For example, after 30 years, the earned percent may grow larger than the original deposits. For realistic long-term estimates, go with 6-8% growth rates.

The S&P 500 stock index has averaged 10% annually, excluding inflation. In short, the more time and the more often gains are added, the faster your funds increase. Below, a line chart compares a 6% vs. 10% annual growth rate (with a $10,000 initial investment and a $500 annual deposit). Notice how the higher rate dramatically accelerates your accumulation over time.

How to Identify and Maximize Your Accumulation Source

The great thing about reinvesting your earnings is that you don’t need to be making millions before you begin. But, of course, it will take some effort on your part. To identify and maximize your investable takings, follow the steps below.

Track Your Money

You’re going to need to know where it's all coming in from. List all your proceeds you get from any sources (salary, side jobs, etc.) and expenses (rent, bills, groceries). Utilize a simple table to keep track of it.

Automate Your Savings

With the day-to-day activities and busy schedule that you have to handle, it’s easy to forget that you need to save to invest. A simple hack is to save part of your leftover cash automatically. For example, set aside 20% of your monthly takings to be invested. If you wish, you can set up apps or banks to do this automatically for you. Microsoft detailed the best methods.

Achieve a Higher Salary

Yes, we know that we said you don’t need to be making millions to reinvest your earnings. However, it will be very difficult to achieve if your responsibilities outweigh your income. Focus on boosting your gains sources.

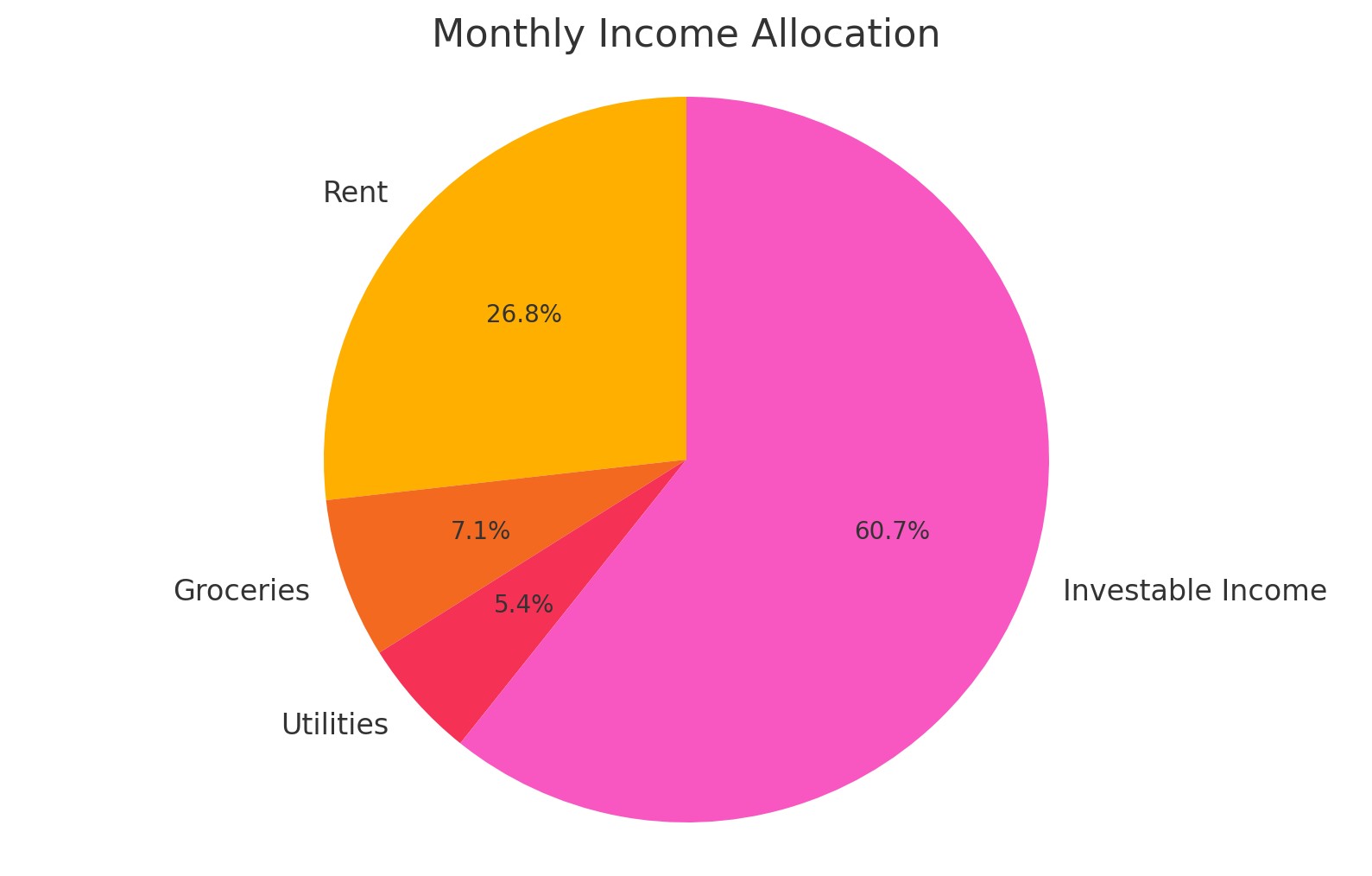

You could ask for a raise or launch a side business. Doing this will give you more funds to reinvest. Here’s a template table you can follow to calculate your disposable cash for reinvestment.

Source

Amount ($)

Expense Category

Amount ($)

Salary

5,000

Rent

1,500

Side Gig

500

Groceries

400

Dividends

100

Utilities

300

Total Amount

5,600

Total Expenses

2,200

Disposable Income

3,400

This pie chart shows how your takings divide into expenses, and what you have left to invest. The larger “investable cash” slice underscores the power of redirecting spending into reinvestment.

Crypto Peer-to-Peer Crowdlending

An amazing new opportunity to reap big profits nowadays is by pooling money together with other investors, sharing the risk, while raking in returns at exorbitant rates. Meanwhile, businesses and projects get much-needed funding that they’d be hard-pressed to acquire otherwise.

Top Strategies for Reinvestment

Beginning your reinvestment journey may seem daunting, especially if you have no idea or strategy for going about it. We’ve listed some basic strategies you could start with and eventually build on:

Dividend Reinvestment Plans (DRIPs)

Some companies let you automatically use dividends (cash payments from stocks) to buy more shares, often without any fees.

Example: Suppose you own 3M stock and their DRIP (via EQ shareowner services) turns your quarterly dividends into extra shares.

Set Up Regular Acquisitions

Employ auto-transfers to send cash monthly to accounts like a 401(k) or IRA. This helps you invest steadily, even as prices change (by way of dollar-cost averaging).

Gaining Additional Business or Rental Proceeds

Reinvest your profits from rentals or side businesses. For example, redirect your rental earnings to buy more properties, or your business profits to expand your operations. This builds wealth faster over time.

Automating with Tools and Platforms

Whatever you can automate, never hesitate. Automation helps keep your activities growing on their own. For example, some platforms will automatically reinvest your dividends and rebalance your portfolio for you. That way, your portfolio stays on track.

Other platforms can round up your everyday purchases to the nearest dollar and invest the spare change for you. Some brokerages, like Robinhood’s IntraFi sweep service, move any uninvested cash into interest‑earning accounts that are FDIC‑insured, up to $2.5 million. Together, these features make it easy to stay invested without requiring extra effort.

DIY Projections and Tracking Progress

You’ll have no way to know if your money is growing unless you track it. Here are some simple ways you could track your progress.

Create a simple spreadsheet

Use these columns:

Year

Starting Balance (what you have at the start of the year)

Total at Year-End (Initial Balance + Savings + Interest)

Example – suppose you:

Start with $10,000

Add $500 per year

Earn 7%

In the first year:

Interest Earned = $10,000 × 7% = $700

Ending Balance = $10,000 + $500 + $700 = $11,200

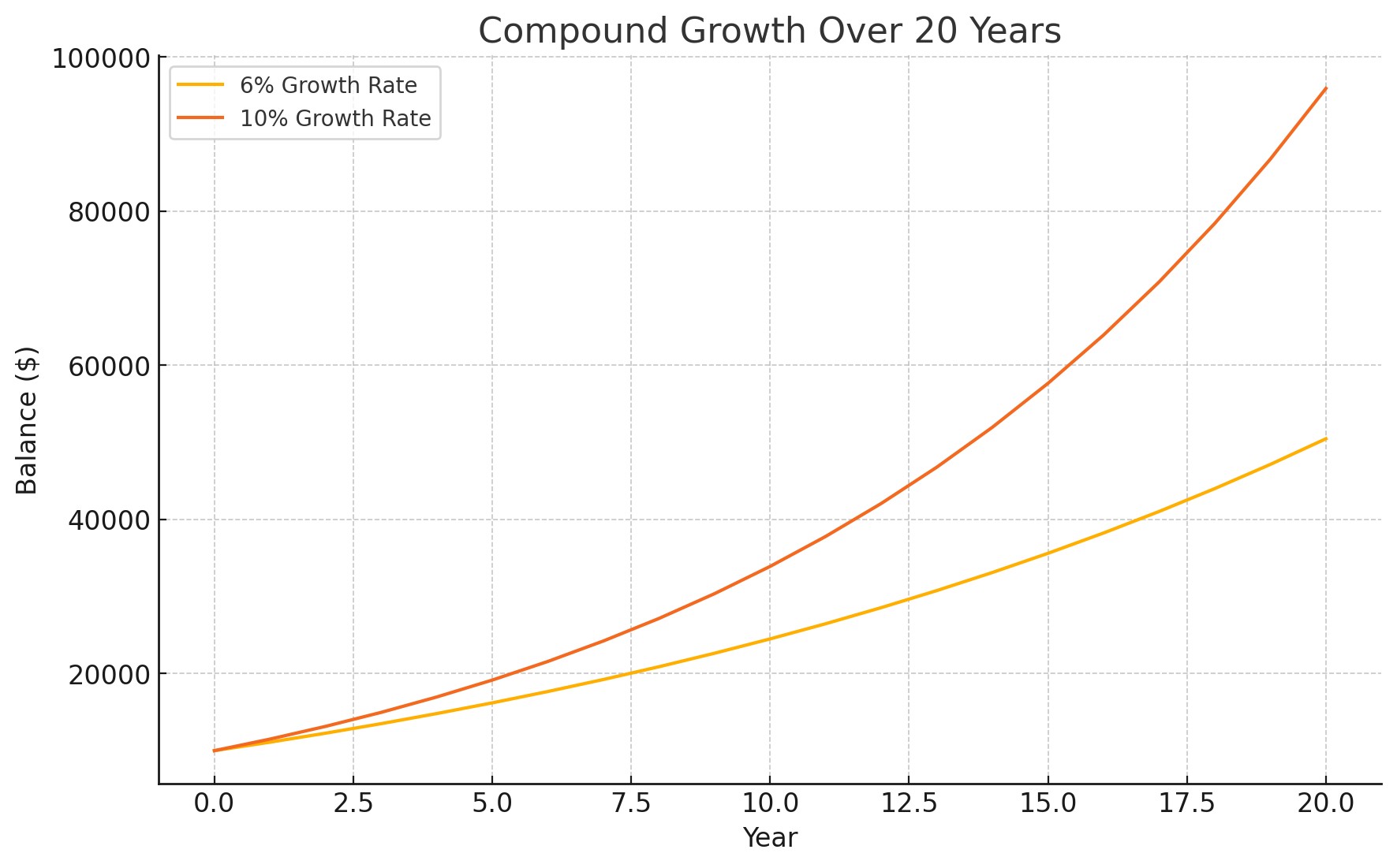

Test Different Plans

Compare “safe” vs “risky” growth:

Safe: 6% → grows more slowly.

Risky: 10% → grows faster (but riskier).

Compare both plans to determine how your funds could grow over 20 years.

Track Your Progress Automatically

Use free tools to be sent updates on your assets. Using these tools helps you stay on track with your goals, for instance, retirement or buying a home.

Common Pitfalls and What You Can Do to Avoid Them

There are a few common mistakes to keep an eye out for.

Don’t let fear or greed make you sell when markets dip. Your automatic purchases will help you to stay on track.

Taxes on reinvested gains tend to eat into your returns, so utilize tax‑friendly accounts like IRAs to keep more of your dough working for you.

Don’t spread your money too thin across too many investments or pile it all into one. Aim for a balanced mix of stocks, bonds, and real estate.

Maximizing Your Snowball Over Time

As your earnings grow, put more of it into holdings. Try investing half of any pay raise you get. Check your portfolio at set times (say, once a year) and adjust it to keep your assets balanced. Use simple charts to spot big shifts.

Decide to cash out only if an asset seems overpriced, or you need the money. Otherwise, leave your gains invested so they keep compounding over time.

Conclusion

When reinvesting, start small. Set up automatic investment, and let compound growth boost your savings. Use tools like dividend reinvestment plans (DRIPs), automatic transfers, and robo‑advisors. Track your progress with a simple spreadsheet. With a clear plan and steady discipline, you will be floored by how fast your portfolio manages to grow.

If you’re interested in snowballing your money fast and fueling it with profits, crowdlending is certainly a lucrative way to generate that with minimal risk.