Investing at a young age is one of the wisest decisions you can ever make, especially if the investment is in low-risk ventures with high returns. Investing at a young age is important if you care about your financial stability as you age. The truth is, even if you work into your 60s, at some point you would have to retire. The dividends from some of the investments you made in your youth will go a long way into contributing to the financial independence you desire as you age.

One of the major benefits of investing at a young age is that the interest or dividends on your investment compound over time, which translates to big money over the long term. Compounding is the result of reinvesting the returns earned on investments in a bank account and thus generating a whole other level more.

To gain a more vivid understanding of compounding interest, say an investor puts $1,000 in an investment that earns 5% returns, or $50, over the first year, which then gets reinvested, bringing the total to $1,050. In the second year, that money earns another 5% return, or $52.50, resulting in a new total of $1,102.50. The third year yields another 5%, or $55.13, in returns, rendering the total $1,157.63. The income continues to grow higher and higher with each passing year.

The chart below illustrates the earnings an investor could accrue by age 65 with a per-year investment of $3,000, starting at age 25, 35, and 45, with a 6% compounding annual return rate.

Investing 101

Investing entails the process of allocating money to purchase assets with the intent of keeping them for a long period of time holding the expectation that they will either appreciate in value or generate returns in the form of income payments or capital gains.

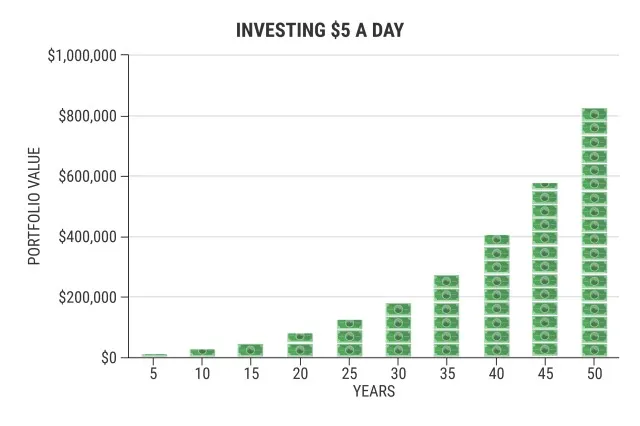

The power of investing is the ability to turn seemingly inconsequential amounts into significant sums of money, especially over a long time. For instance, the chart below shows what investing a paltry $5 a day could give you 5 years down the road.

Credit: Coryanne Hicks & Nate Hellman

Risk

Like almost any concentrated effort in life, investing involves risks. So by investing in buying any type of asset, beware that there is going to be some degree of risk involved. There are three types of investment risks:

low

medium

high

A major caveat to this though is these risk levels entail different return rates. Studies have shown that young investors have better risk-taking ability than their seniors. Older-generation investors are known to be generally conservative and prefer stability, thus electing to evade high-risk investment ventures as a result. There’s an old saying: “The greater the risk, the greater the reward,” which means the likelihood of earning ample returns at a young age is enhanced that much more by a willingness to take bigger risks.

Return

Return is the amount of money that you earn on your investment over time. The returns you earn depend on factors such as the amount you invest, the assets you buy, the number of years you sustain the investment for, and the risk level associated with the investment.

If left in place for years, returns can compound and yield even more returns. So investing at a young age and leaving it till past your retirement can give you compounded returns that will afford you financial independence.

Investment Options for Beginners

Here are a few investment options to start with.

Low-risk options (high-yield savings account)

This is one of the most beginner-friendly options to start with, in particular a high-yield savings account. Here’s how it works:

Open a savings account with a bank that has a verified history of paying interest.

Deposit a good amount of money in the account.

Depending on the bank, the money in your account earns interest either daily or monthly.

Adding extra money and also keeping the money in the account can earn you huge interest over a long time.

The best part of going the savings account route is that it involves no or minimal risks. You wont’ end up losing your money because it is safe with the bank. While your money is in your account, the bank uses it for business operations.

Investing in Realty

For a beginner, the funds may not exist to purchase properties. This is where investing in real estate comes in. Realty companies manage a real estate and other landed properties portfolio for everyone. Traditionally, realty companies pay higher dividends to their stakeholders when compared to many other assets like stocks.

Buying Stocks

Buying into a company's stock makes you a partial owner and allows the company to raise money to fund their springboard their operations. So this allows you to share in the company's gains, as well as its losses. Also, some stocks pay dividends to their stakeholders – small but regular payments of companies’ profits.

With their unpredictable returns, individual companies may fold, and buying stocks comes with a higher risk than other kinds of investments.

Managed Funds and Exchange Traded Funds (ETFs)

Following a particular strategy, managed funds and ETFs invest in a portfolio of stocks, bonds, and commodities. These funds (particularly managed funds and ETFs) allow you to invest in hundreds or thousands of assets at a time when you buy their shares. This easy investment diversification makes managed funds and ETFs generally less risky compared to individual investments, such as pure stocks.

Managed funds and ETFs are types of pooled funds, but they operate slightly differently. Managed funds buy and sell a broad range of assets and are usually actively managed by an investment professional, who chooses what they invest in. For the most part, they try to do better than a benchmark index.

Instead of trying to beat a particular index, ETFs generally try to copy the performance of a specific benchmark index. Following this passive investing approach means your investment returns may never surpass the average benchmark performance.

Broker

NerdWallet Rating

Fees

Account Minimum

Charles Schwab

4.8/5

$0 for online equity trades

$0

J.P. Morgan

4.5/5

$0 per trade

$0

Vanguard

4.5/5

$0 per trade

$0

Robinhood

4.5/5

$0 per trade

$0

SoFi

4.4/5

$0 per trade

$0

Retirement Accounts (401(k)s, IRAs)

As a young, working individual, opening retirement accounts such as Individual Retirement Accounts (IRAs) and 401(k) can help secure your financial future after you retire and provide you greater investment flexibility if you stick to the rules. The most notable difference between 401(k)s and IRAs is that 401(k)s are retirement savings schemes offered through employers, while IRAs can be opened by individuals with earned income through a broker or a bank.

Also, another major difference between both is that a 401(k) offers higher contribution limits and lower investment options, while an IRA offers more investment options and tax benefits but entails much lower contribution limits.

Conclusion

Reflecting No one can assessyour financial situation better than yourself. You are the one todecide how much you plan to invest on a daily, weekly, monthly, oryearly basis. You have micro-investing apps to choose from as well.Start small and stay consistent at first. You don't have to invest alarger percentage or all of your salary to be on the right track forinvestment. Over time, those small investments will compound to giveyou high returns in the future.