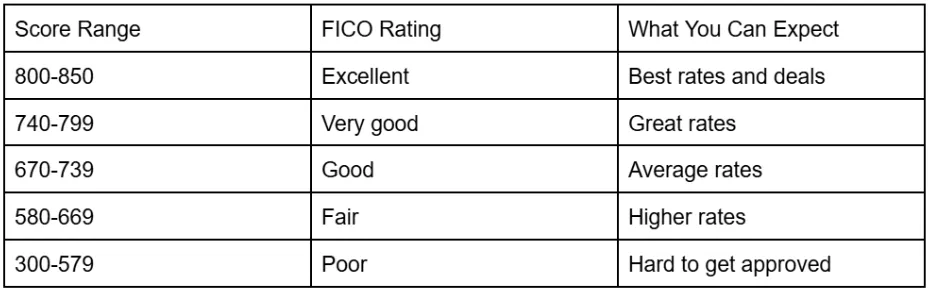

Countless citizens think of how well we fulfill debt obligations as being rather inconsequential. We can hardly resist buying flashy corvettes and playoff game tickets. Considering the overtime hours we do, we deserve it. Some of us manage to live within our means while others make a late payment here and pay off items in collections there. It ends up rearing its ugly head or rolling out a red carpet to us later. In reality, there are few things that are used so ubiquitously in such important areas of our lives as our credit score.

If you’ve paid responsibly before, that’s going to determine whether you’ll end up saving thousands in interest on a mortgage as a result, even whether you can get certain jobs.. So this is no laughing affair.

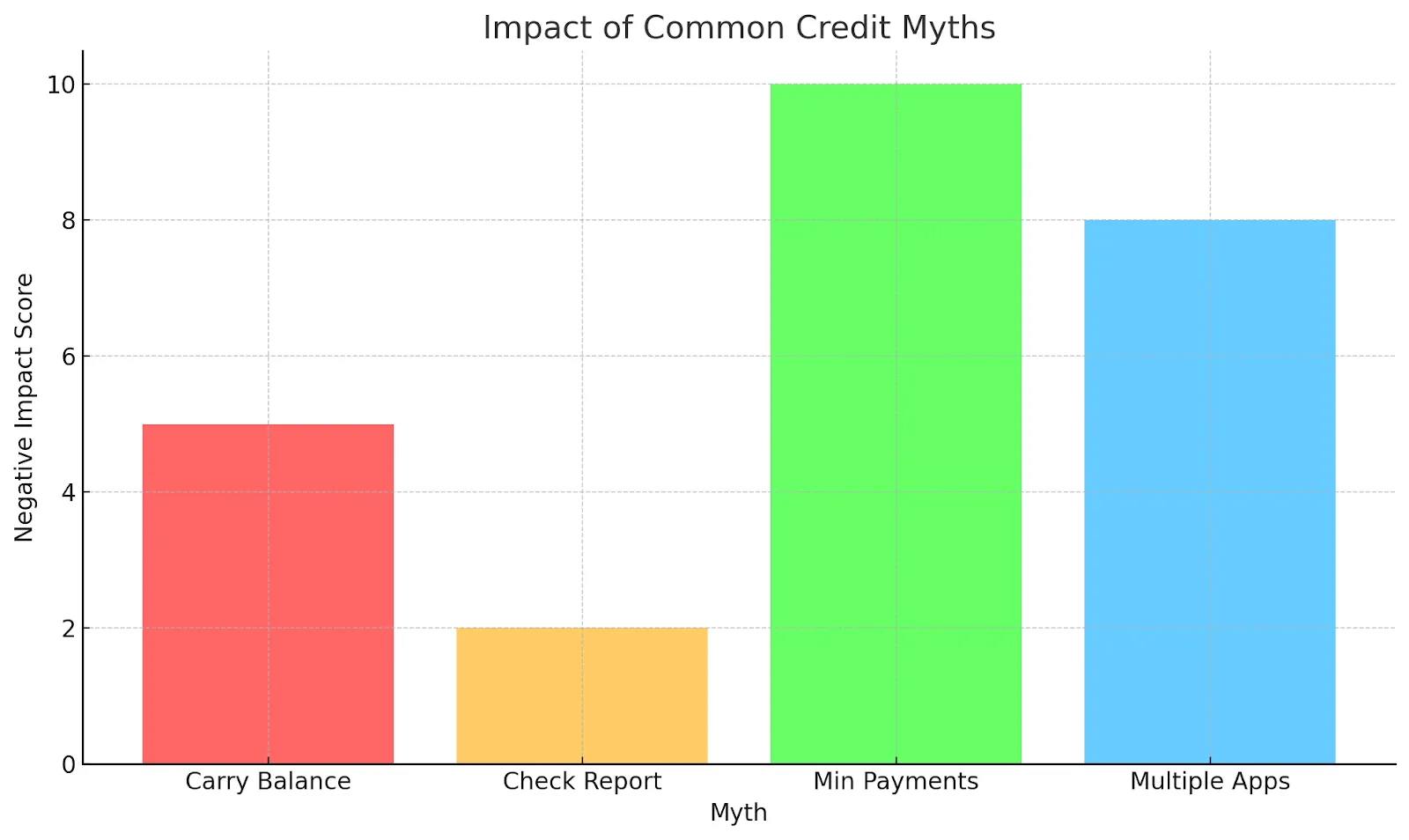

So you know how you score. The essential thing now is the way you harness and enhance that or let it tumble. Wherever it is now, you can direct it in a favorable direction or kick it up even higher. That’s where we get into the myths and realities. Many falsely believe obtaining their rating will screw them, or that building it would demand a certain quantity borrowed on a card.

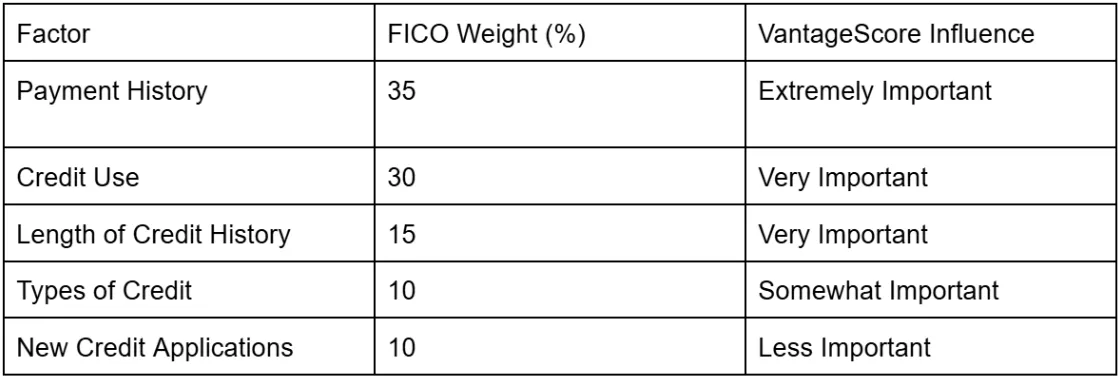

Several credit bureaus exist and each company counts them differently. FICO is used by a whopping ninety percent of lenders when you apply for credit. Still keep others in mind like:

VantageScore

Experian PLUS

Equifax

TransUnion

Meet Sofia, a 26-year-old teacher. She ignored her credit for years because she feared checking it would lower her score. Once she learned that checking her own report is a “soft inquiry” that has no effect, she found two errors from an old cell phone account and had them removed—her score jumped 40 points in one month.

Moving On Up

Moving onto some robust strategies accompanied by their FICO rating weight.

Being on Time (35%)

Timeliness in paying is number one. Fortunately, the sting eventually goes away after 7 years, a golden chance to correct yourself.

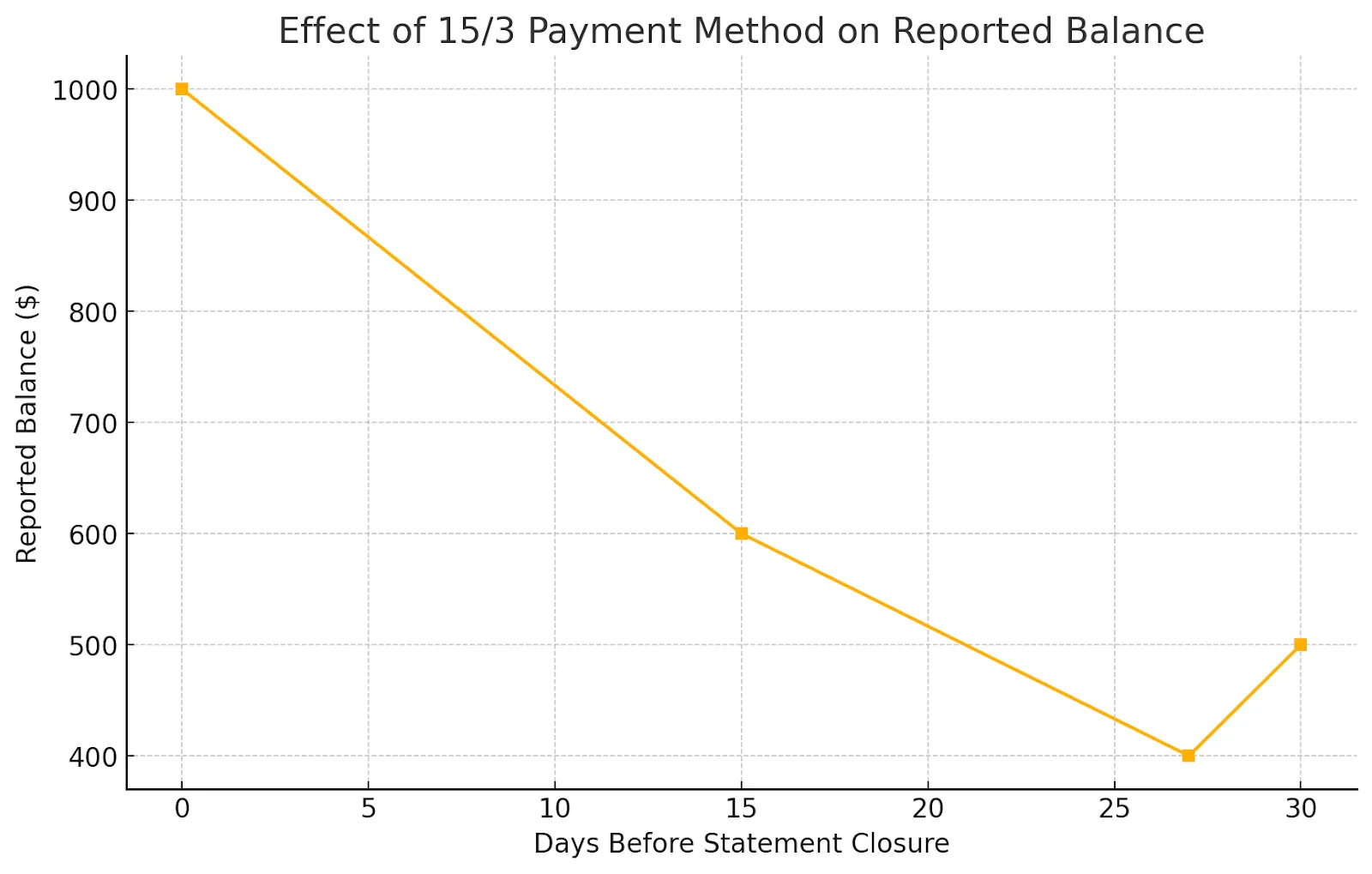

One wise practice is to set up autopayments for greater than the minimum and let those pay for themselves. Don’t leave your busy memory in charge. Google or iPhone reminders is a great way to maintain you up to speed. Consider trying a service like Experian Boost too to add your heating bill to the rating.

Marcus, a small business owner, set up autopay for all his accounts after missing a $60 credit card bill by just two days. That tiny mistake dropped his score by 50 points. Since setting reminders and using autopay for the minimums, he’s never been late again, and within a year, his score recovered—and then some.

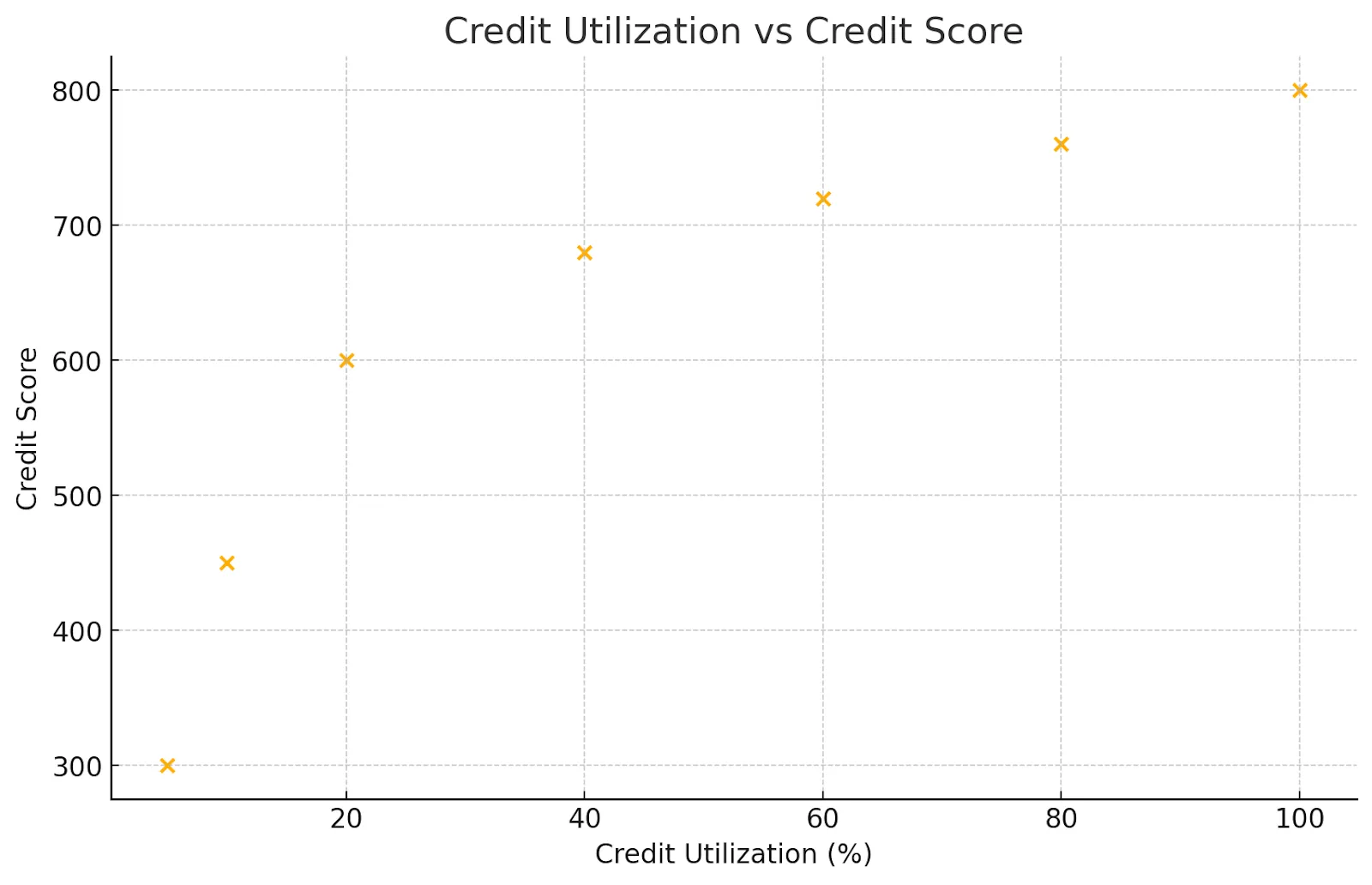

Given higher limits though, your score will consequently benefit. Making a few payments monthly.

Danielle, a freelance photographer, had a $5,000 credit limit and routinely carried a $2,500 balance, thinking paying on time was all that mattered. Once she learned her utilization was at 50%, she began making mid-month payments and keeping balances under $500. Her score climbed from 690 to 760 in under a year.

Keep Old Credit Cards Open (15%)

Card age stands for miles of difference. Don’t toss those old lingering cards. Consider asking a family member to add you as an authorized user on their old account. Also use old cards for transactions once in a blue moon so the bank will keep them operating.

Ethan, a 34-year-old engineer, almost closed his first credit card from college because it had a small limit and no rewards. Instead, he kept it open and put a small recurring subscription on it to keep it active. This helped maintain his 12-year credit history, which cushioned the impact when he opened a new mortgage.

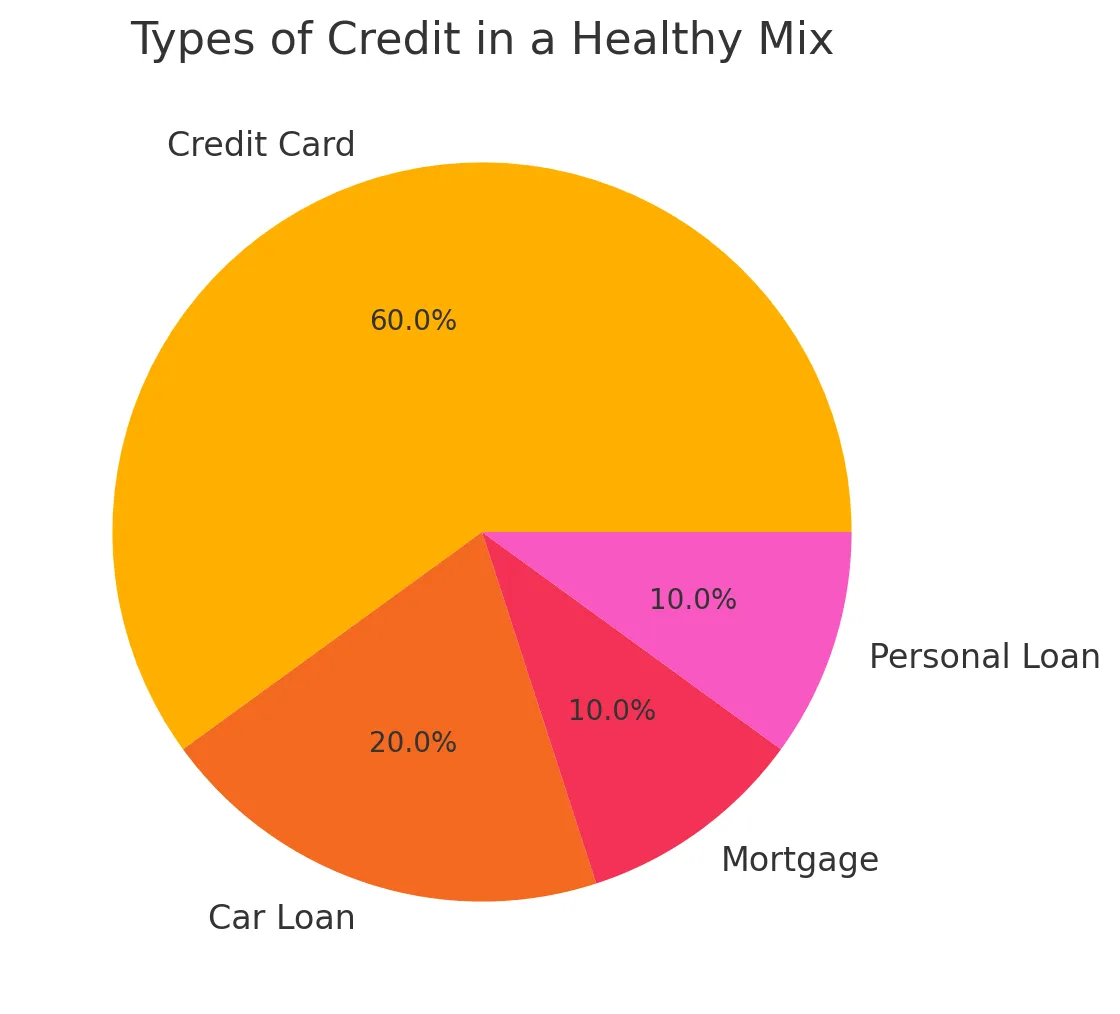

Have Different Types of Credit (10%)

Don’t go into debt just to add another account though. Use credit cards, car loans, the works.

Rita, just out of grad school, only had student loans in her credit history. She took out a small credit-builder loan from her credit union and opened a secured credit card. Within 8 months, her score rose by over 60 points as her credit profile diversified.

Improving your credit profile unlocks access to new financial opportunities too. Crowdlending platforms like Maclear use next-generation credit scoring models to connect responsible borrowers with mission-driven funding. By assessing applicants with innovative tools beyond traditional credit scores, Maclear helps both individuals and small businesses gain access to financing that banks often deny—all while delivering attractive returns to investors.

Maya started at 580 after medical debt went to collections. She set up payment plans, disputed an error, and kept new balances under 10%. Two years later, she’s at 745 and qualified for a mortgage with a low interest rate.

Dispute Errors on Your Credit Report

Inaccurate negative information can weigh down your score unnecessarily. By law, you can dispute incorrect entries with the credit bureaus. Get free copies of your reports from AnnualCreditReport.com. Highlight inaccuracies such as accounts you never opened, wrongly reported late payments, or balances that are higher than they should be. File disputes online with each bureau that reports the error.

Use a Secured Credit Card or Credit Builder Loan

A secured card requires a cash deposit that acts as your credit limit. Use it for small, manageable purchases and pay in full each month. A credit builder loan locks away borrowed funds in a savings account until you finish payments, creating a record of timely repayment.

Avoid New Hard Inquiries Unless Necessary

Every hard inquiry — triggered by applying for new credit — can temporarily drop your score by a few points. Multiple inquiries in a short time can add up. Only apply for credit when it’s truly needed. Rate-shop for loans (like a mortgage) within a 14–45 day window to minimize scoring impact.

Your Next Steps

Knowing your credit score guides your money moves. You should pay your bills on time and keep card balances low if you want to see real change over months and years. Stick to a simple plan and work at it steadily so that your credit gets better. Better credit brings lower interest rates, more accessible loans, and better opportunities.

Want to put your improved credit to use where it really counts? Maclear empowers borrowers and investors alike through a Swiss crowdlending platform that values innovation, inclusion, and impact.