Crowd & Crypto Lending in the UK: Regulations, Taxation, and Future Developments

30.09.2025

6

The UK, a longtime leader in financial innovation, is now breaking new ground and redefining its crowdlending and cryptocurrency space.

In this guide, we’ll examine the most recent regulatory actions, changing tax laws, and new developments that promise to influence the UK’s digital finance landscape. We’ll use data, business case studies, and international comparisons to ensure you have a clear picture of the primary tax regulations and future developments in the UK.

Crowdlending is more than just a catchphrase; it's a valuable financial tool that connects entrepreneurs and small businesses with investors eager to support innovation.

For example, some crowdlending platforms have facilitated the disbursement of billions of pounds in loans, having a significant social and economic impact; after all, they effectively transform the lending landscape for UK businesses.

In this evolving market, one such standout is Maclear, which combines transparent risk-sharing with advanced credit evaluation tools. Their platform empowers investors to participate confidently in crowdlending opportunities, leveraging technology to bridge gaps left by traditional financing.

The UK’s Regulatory Framework

The Financial Conduct Authority (FCA) is the UK’s body entrusted with ensuring that innovation proceeds alongside investor protection. Consider these key protective measures:

Regulatory pillar

What it means for investors

Capital adequacy

Platforms must maintain robust financial reserves – a "rainy day" fund that cushions your investments during downturns.

Risk disclosures

These detailed reports give investors insight into borrower creditworthiness and historical default rates.

Operational transparency

Regular, open disclosures on borrower profiles and performance build trust and enable self-informed decisions.

These FCA-implemented controls go beyond simple administrative checkboxes.

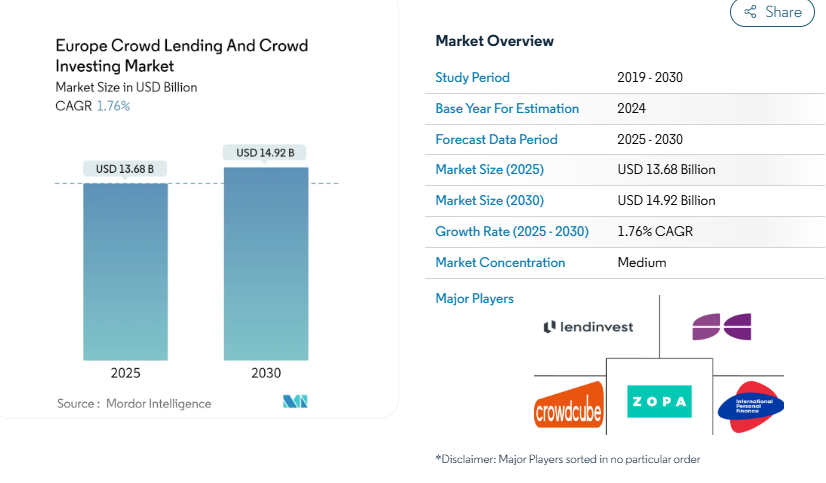

According to research from Mordor Intelligence, regulated crowdlending and crowd investing in Europe are expected to grow at an annual 1.76% CAGR from 2025 to 2030.

This figure illustrates that these controls are a market-stabilizing, living safety net.

Crypto in the UK

Cryptocurrencies have a reputation for being an uncharted, exciting, but uncertain territory of finance. The UK is taking significant action to steer these digital assets into a transparent and strong framework as they evolve.

Let’s focus on that for a moment.

Important Advances in Crypto Regulation

Although the UK has not yet passed a stand-alone crypto legislation, it’s working hard to enact guidelines for regulating digital banking. Below are a few of the crucial actions the country has taken:

Expanded FCA oversight: The FCA now requires crypto exchanges, custodians, and other crypto asset service providers (CASPs) to register and adhere to strict Know Your Customer (KYC) and anti-money laundering (AML) regulations. This requirement guarantees that innovative businesses function responsibly.

The Property (Digital Assets) Bill: The UK introduced this measure in 2024. It establishes a new category for digital assets as personal property, giving cryptocurrency owners more precise legal rights and stronger protections against fraud and theft.

Stablecoin and crypto lending regulation: The UK Treasury is creating custom regulations as stablecoins become a commonplace payment method and cryptocurrency lending soars. These rules will require prospectus-style disclosures and appropriate backing asset protection, treating stablecoins in a manner akin to those of conventional securities.

According to a recent draft framework mentioned in PwC's Global Crypto Regulation Report 2025, industry experts anticipate that a clear regulatory framework will enhance investor confidence in the UK's digital asset market.

The Changing Regulations Landscape

Here’s a glance at the new framework.

Aspect

Current Framework

Future Developments

Registration & Licensing

FCA registration for crypto exchanges and custodians.

Advanced AML/KYC protocols under a new Cryptoassets Order integrated with FSMA to offer deeper oversight.

Stablecoin Regulation

Treasury guidelines pending full framework integration.

Stablecoins will be regulated as securities with robust backing and disclosure requirements.

Prudential Requirements

Ad hoc provisions via existing FCA guidelines (e.g., CASS).

Introduction of specialized guidelines (e.g., CRYPTOPRU) to standardize capital, governance, and risk disclosures.

UK Crypto and Crowdlending Taxation: a Double-Edged Sword

Crowdlending and crypto carry distinct tax obligations that every responsible and successful investor must know.

Crowdlending Taxes

When you invest in crowdlending platforms, your tax responsibilities typically include:

Interest income: The UK government treats income from loans as personal income and taxes it at rates ranging from 20% to 45%, depending on your total earnings.

Capital gains: The government may subject profits from trading loans in secondary markets to Capital Gains Tax (CGT).

Loss offsetting: The system enables loss reporting to offset gains, thereby protecting your overall portfolio during periods of volatility.

Emerging Crypto Taxes

The UK’s Crypto tax landscape is ripe for significant updates driven by international standards and domestic policy adjustments:

Capital gains for crypto transactions: Profits from selling crypto attract either a 10% or 20% tax rate, contingent on your income bracket.

Income tax on crypto earnings: Crypto earned from staking or mining is considered regular income.

Enhanced reporting under OECD CARF: Providers will need to gather detailed information on cryptocurrency transactions starting in early 2026. Thus, they must maintain accurate records to avoid severe fines.

The aim behind these changes is to level the playing field, promote innovation and accountability, and ensure that digital transactions comply with established standards.

Insights from Academic and Empirical Research

Researchers from academia and business are increasingly examining the impact of transparency and regulation on market stability in cryptocurrency and crowdlending.

According to a multi-year study conducted by the Cambridge Centre for Alternative Finance, platforms with greater levels of transparency and capital sufficiency had default rates that were between 12 and 15 percent lower. Strong risk disclosures were strongly associated with higher investor confidence and market expansion.

The London School of Economics (LSE) and other institutions state that transparent regulatory frameworks lower cryptocurrency market volatility. For example, nations with stricter AML/KYC regulations report higher consumer protection ratings and a 10% increase in total cryptocurrency asset trading volume.

Meanwhile, the Journal of Financial Stability says that investors are likelier to actively engage in crowdlending and cryptocurrency investments when they are well-informed through improved disclosures and a balanced regulatory environment.

Policy Impact and Investor Behavior

Besides affecting market dynamics, recent regulatory advancements and policy changes also affect investor behavior. Due to increased openness and thorough reporting, investors are shifting away from short-term speculation to longer-term, reliable crowdlending and cryptocurrency investments.

Thanks to streamlined tax regulations and enhanced disclosures, investors can now evaluate and mitigate risks. According to surveys, investor confidence in cryptocurrency markets has increased by approximately 8% due to recent transparency.

We’re also witnessing a wider distributive impact across the economy as more ordinary investors make their initial forays into these markets, thanks to increased investor education programs supported by government policy and research.

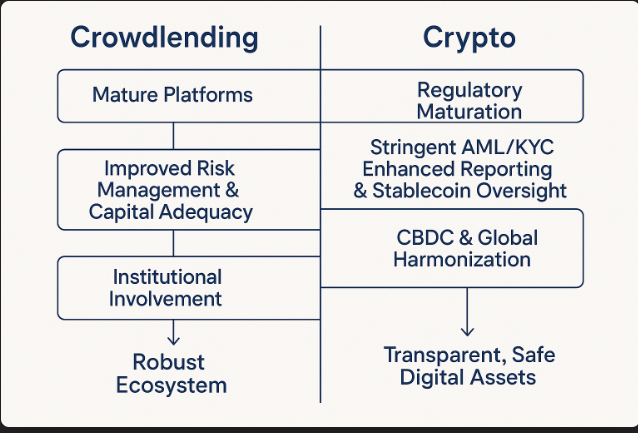

Visualizing the Future

Here is an updated ASCII figure that charts the evolution to help you understand how these patterns and research findings have come together:

Future Developments: Charting the Road Ahead

Both crowdlending and cryptocurrency present exciting prospects as the UK's financial landscape changes, but they also require flexibility and foresight. Think about these upcoming developments:

As more crowd lending and crypto lending platforms adopt artificial intelligence and machine learning to enhance borrower evaluation methods, expectations are high that default rates will continue declining and investors’ confidence will increase.

Increased involvement on the part of banks and asset managers would lead to even stronger governance and risk management standards. The FCA will continue to modify its supervisory structures to create robust investor protection programs that can keep pace with rapid innovation.

Final Thoughts: Embracing a Future of Responsible Innovation

The UK’s financial ecosystem is undergoing a challenging yet exciting transformation. In the digital era, crowdlending and cryptocurrency are more than just trendy terms; they are reshaping how we raise, handle, and expand capital. Investors, innovators, strong regulatory frameworks, well-considered tax laws, and insights supported by research are the surest way to secure a prosperous future.

For UK investors seeking a reliable, tech-forward platform aligned with strong regulatory values, Maclear offers a Swiss-rooted alternative designed for transparency, risk mitigation, and consistent returns.

FAQ

What is crowdlending and how does it work in the UK?▼

Crowdlending is a financial tool that connects entrepreneurs and small businesses with investors who want to support innovation. In the UK, crowdlending platforms have facilitated billions of pounds in loans, significantly impacting the lending landscape.

Platforms like Maclear combine transparent risk-sharing with advanced credit evaluation tools, allowing investors to participate confidently in crowdlending opportunities while leveraging technology to bridge gaps left by traditional financing.

What regulatory protections exist for crowdlending investors?▼

The Financial Conduct Authority (FCA) oversees crowdlending in the UK with three key protective measures:

Capital adequacy: Platforms must maintain robust financial reserves to protect investments during downturns

Risk disclosures: Detailed reports provide insight into borrower creditworthiness and historical default rates

Operational transparency: Regular disclosures on borrower profiles and performance enable informed decisions

Research shows that regulated crowdlending in Europe is expected to grow at 1.76% CAGR from 2025 to 2030.

What are the current crypto regulations in the UK?▼

The UK is developing a comprehensive framework for cryptocurrency regulation:

FCA oversight: Crypto exchanges and custodians must register and adhere to strict KYC and AML regulations

Property (Digital Assets) Bill (2024): Establishes digital assets as personal property with legal protections

Stablecoin regulation: The Treasury is creating regulations requiring disclosure and asset backing similar to securities

Future developments include advanced AML/KYC protocols and specialized guidelines (CRYPTOPRU) for capital and risk management.

How is crowdlending income taxed in the UK?▼

Crowdlending investments have specific tax obligations:

Interest income: Treated as personal income, taxed at 20% to 45% depending on your total earnings

Capital gains: Profits from trading loans in secondary markets may be subject to Capital Gains Tax (CGT)

Loss offsetting: You can report losses to offset gains, protecting your portfolio during volatility

What are the tax implications for cryptocurrency in the UK?▼

Cryptocurrency taxation in the UK includes:

Capital gains: Profits from selling crypto are taxed at 10% or 20% depending on your income bracket

Income tax: Crypto earned from staking or mining is treated as regular income

Enhanced reporting: Under OECD CARF standards, providers must gather detailed transaction information starting in early 2026

These changes aim to promote innovation, accountability, and ensure digital transactions comply with established standards.

How do regulations impact market stability and investor confidence?▼

Academic research demonstrates significant benefits of regulation:

Platforms with higher transparency and capital sufficiency have 12-15% lower default rates (Cambridge Centre for Alternative Finance)

Countries with stricter AML/KYC regulations report a 10% increase in crypto trading volume and higher consumer protection ratings

Recent transparency improvements have increased investor confidence by approximately 8%

Investors are shifting from short-term speculation to longer-term, reliable investments thanks to enhanced disclosures and balanced regulations.

What future developments can we expect?▼

The UK's financial landscape is evolving with exciting prospects:

AI and machine learning: Platforms are adopting advanced technologies to enhance borrower evaluation and reduce default rates

Institutional involvement: Increased participation from banks and asset managers will strengthen governance and risk management standards

Enhanced FCA oversight: Continued modifications to supervisory structures for robust investor protection

These developments promise to make crowdlending and cryptocurrency more secure, transparent, and accessible for all investors.