Prêts participatifs et cryptographiques au Royaume-Uni : réglementations, fiscalité et développements futurs

30.09.2025

6

Le Royaume-Uni, leader de longue date en matière d'innovation financière, innove aujourd'hui et redéfinit son espace de crowdlending et de cryptomonnaies.

Dans ce guide, nous examinerons les mesures réglementaires les plus récentes, l'évolution des lois fiscales et les nouveaux développements qui devraient influencer le paysage de la finance numérique au Royaume-Uni. Nous utiliserons des données, des études de cas et des comparaisons internationales pour vous donner une idée claire des principales réglementations fiscales et des développements futurs au Royaume-Uni.

Le crowdlending est bien plus qu'un simple slogan ; c'est un outil financier précieux qui met en relation les entrepreneurs et les petites entreprises avec des investisseurs désireux de soutenir l'innovation.

Par exemple, certaines plateformes de financement participatif ont facilité le versement de milliards de livres sterling sous forme de prêts, ce qui a eu un impact social et économique significatif ; après tout, elles transforment efficacement le paysage des prêts pour les entreprises britanniques.

Sur ce marché en pleine évolution, l'une de ces caractéristiques est Maclear, qui associe un partage transparent des risques à des outils avancés d'évaluation du crédit. Leur plateforme permet aux investisseurs de participer en toute confiance aux opportunités de financement participatif, en tirant parti de la technologie pour combler les lacunes laissées par le financement traditionnel.

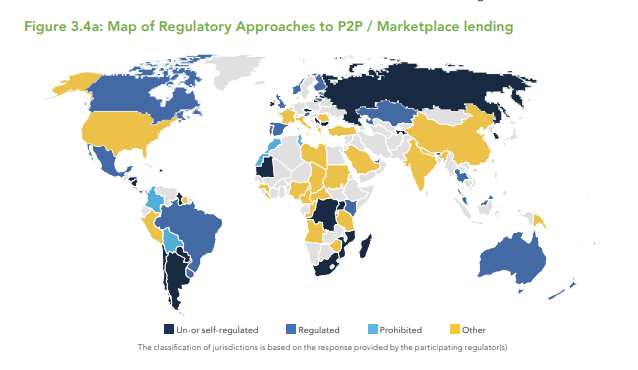

Le cadre réglementaire du Royaume-Uni

Le Autorité de conduite financière (FCA) est l'organisme britannique chargé de veiller à ce que l'innovation aille de pair avec la protection des investisseurs. Tenez compte des principales mesures de protection suivantes :

Pilier réglementaire

Ce que cela signifie pour les investisseurs

Adéquation des fonds propres

Les plateformes doivent maintenir des réserves financières solides – un fonds de prévoyance qui protège vos investissements en période de ralentissement.

Divulgation des risques

Ces rapports détaillés donnent aux investisseurs un aperçu de la solvabilité des emprunteurs et des taux de défaut historiques.

Transparence opérationnelle

Des divulgations régulières et ouvertes sur les profils et les performances des emprunteurs renforcent la confiance et permettent des décisions éclairées.

Ces contrôles mis en œuvre par la FCA vont au-delà des simples cases à cocher administratives.

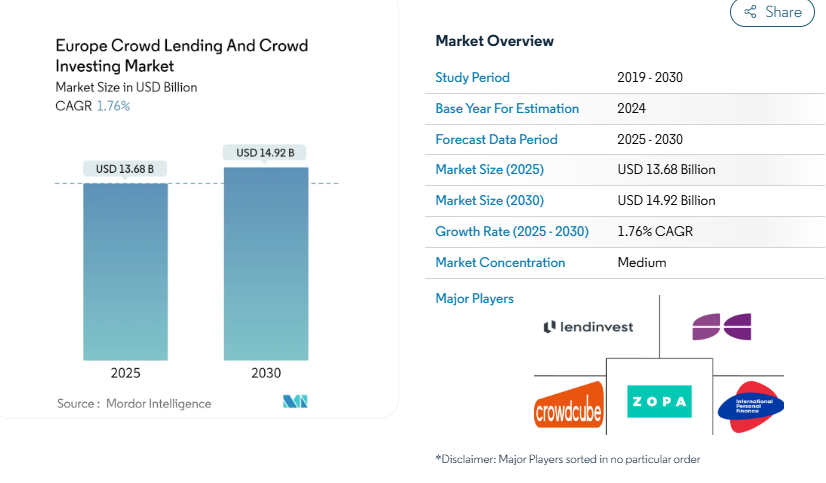

Selon une étude de Mordor Intelligence, le crowdlending réglementé et l'investissement participatif en Europe devraient augmenter à un TCAC annuel de 1,76 % entre 2025 et 2030.

Cette figure montre que ces contrôles constituent un filet de sécurité durable qui stabilise le marché.

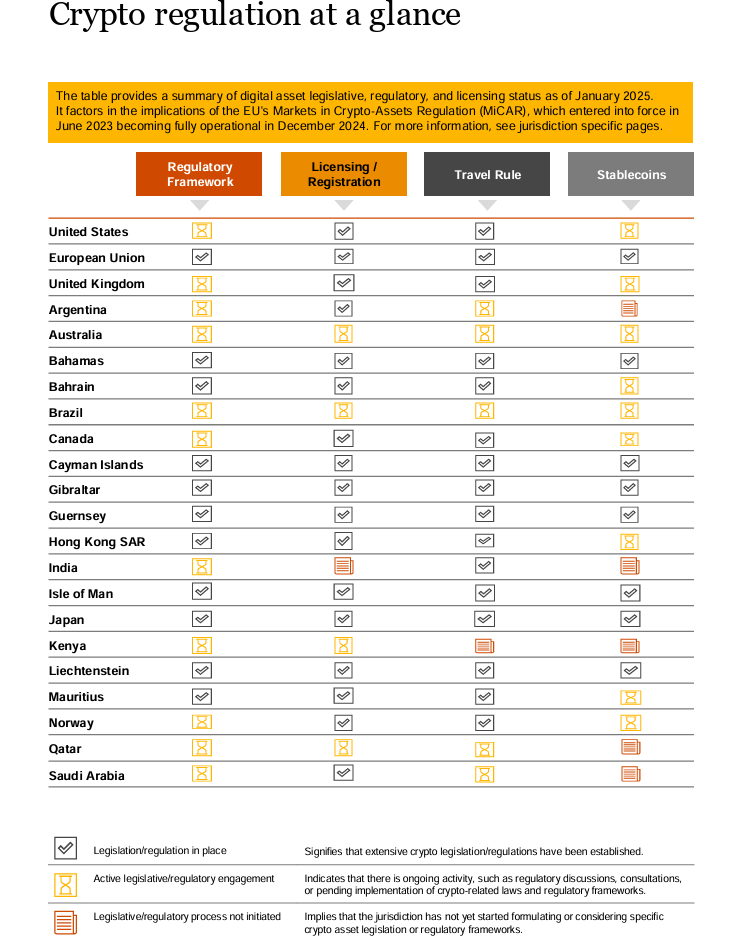

Crypto au Royaume-Uni

Les cryptomonnaies ont la réputation d'être un territoire financier inexploré, passionnant mais incertain. Le Royaume-Uni prend des mesures importantes pour orienter ces actifs numériques dans un cadre transparent et solide au fur et à mesure de leur évolution.

Concentrons-nous là-dessus pendant un moment.

Avancées importantes en matière de réglementation des cryptomonnaies

Bien que le Royaume-Uni n'ait pas encore adopté de législation autonome sur la cryptographie, il travaille d'arrache-pied pour promulguer des directives visant à réglementer les services bancaires numériques. Voici quelques-unes des mesures cruciales prises par le pays :

Supervision élargie de la FCA : la FCA exige désormais que les échanges cryptographiques, les dépositaires et les autres fournisseurs de services d'actifs cryptographiques (CASP) s'enregistrent et respectent les réglementations strictes en matière de connaissance du client (KYC) et de lutte contre le blanchiment d'argent (AML). Cette exigence garantit que les entreprises innovantes fonctionnent de manière responsable.

Le projet de loi sur la propriété (actifs numériques) : Le Royaume-Uni a introduit cette mesure en 2024. Il établit une nouvelle catégorie pour les actifs numériques en tant que biens personnels, donnant aux propriétaires de cryptomonnaies des droits juridiques plus précis et des protections plus strictes contre la fraude et le vol.

Réglementation des Stablecoin et des prêts cryptographiques: Le Trésor britannique crée des réglementations personnalisées alors que les pièces stables deviennent un mode de paiement courant et que les prêts de cryptomonnaies explosent. Ces règles exigeront des informations de type prospectus et une protection appropriée des actifs de soutien, en traitant les pièces stables de la même manière que les titres classiques.

Selon un récent projet de cadre mentionné dans le Rapport mondial sur la réglementation cryptographique 2025 de PwC, les experts du secteur prévoient qu'un cadre réglementaire clair renforcera la confiance des investisseurs dans le marché britannique des actifs numériques.

L'évolution du paysage réglementaire

Voici un aperçu du nouveau cadre.

Aspect

Cadre actuel

Développements futurs

Enregistrement et licences

Enregistrement FCA pour les plateformes d'échange de cryptomonnaies et les dépositaires.

Protocoles avancés AML/KYC dans le cadre d'une nouvelle ordonnance sur les cryptoactifs intégrée à la FSMA pour offrir une surveillance plus approfondie.

Réglementation des stablecoins

Lignes directrices du Trésor en attente d'intégration complète du cadre réglementaire.

Les stablecoins seront réglementés comme des valeurs mobilières avec des exigences solides en matière de garantie et de divulgation.

Exigences prudentielles

Dispositions ad hoc via les lignes directrices existantes de la FCA (par ex., CASS).

Introduction de lignes directrices spécialisées (par ex., CRYPTOPRU) pour normaliser le capital, la gouvernance et les divulgations de risques.

Fiscalité britannique de la cryptographie et du crowdlending : une arme à double tranchant

Le crowdlending et la cryptographie comportent des obligations fiscales distinctes que tout investisseur responsable et prospère doit connaître.

Taxes sur le financement participatif

Lorsque vous investissez dans des plateformes de crowdlending, vos responsabilités fiscales incluent généralement :

Revenus d'intérêts : le gouvernement britannique considère les revenus des prêts comme des revenus personnels et les impose à des taux allant de 20 % à 45 %, en fonction de vos revenus totaux.

Plus-values : Le gouvernement peut soumettre les bénéfices des prêts commerciaux sur les marchés secondaires à l'impôt sur les plus-values (CGT).

Compensation des pertes : le système permet de déclarer les pertes pour compenser les gains, protégeant ainsi l'ensemble de votre portefeuille en période de volatilité.

Taxes cryptographiques émergentes

Le Royaume-Uni Paysage fiscal des cryptomonnaies est mûr pour des mises à jour importantes motivées par les normes internationales et les ajustements des politiques nationales :

Plus-values pour les transactions cryptographiques : les bénéfices provenant de la vente de crypto-monnaies sont soumis à un taux d'imposition de 10 % ou 20 %, en fonction de votre tranche de revenus.

Impôt sur le revenu sur les revenus liés aux cryptomonnaies : les cryptomonnaies obtenues grâce au staking ou au minage sont considérées comme des revenus réguliers.

Rapports améliorés en vertu de CARTE OCDE : Les fournisseurs devront recueillir des informations détaillées sur les transactions de cryptomonnaies à partir du début de 2026. Ils doivent donc tenir des registres précis pour éviter de lourdes amendes.

L'objectif de ces changements est d'uniformiser les règles du jeu, de promouvoir l'innovation et la responsabilité, et de garantir que les transactions numériques sont conformes aux normes établies.

Perspectives issues de la recherche universitaire et empirique

Les chercheurs du monde universitaire et du monde des affaires examinent de plus en plus l'impact de la transparence et de la réglementation sur la stabilité du marché des cryptomonnaies et du crowdlending.

Selon une étude pluriannuelle menée par le Cambridge Centre for Alternative Finance, les plateformes présentant des niveaux de transparence et de suffisance en capital plus élevés affichaient des taux de défaut inférieurs de 12 à 15 %. De solides informations sur les risques étaient étroitement associées à une confiance accrue des investisseurs et à l'expansion du marché.

La London School of Economics (LSE) et d'autres institutions affirment que des cadres réglementaires transparents réduisent la volatilité du marché des cryptomonnaies. Par exemple, les pays dotés de réglementations plus strictes en matière de lutte contre le blanchiment d'argent et de connaissance de la clientèle enregistrent des taux de protection des consommateurs plus élevés et une augmentation de 10 % du volume total des transactions d'actifs en cryptomonnaies.

Dans le même temps, le Journal of Financial Stability indique que les investisseurs sont plus susceptibles de s'engager activement dans le crowdlending et les investissements dans les crypto-monnaies lorsqu'ils sont bien informés grâce à des informations améliorées et à un environnement réglementaire équilibré.

Impact des politiques et comportement des investisseurs

En plus d'affecter la dynamique du marché, les récentes avancées réglementaires et les changements politiques ont également une incidence sur le comportement des investisseurs. Grâce à une ouverture accrue et à des rapports approfondis, les investisseurs abandonnent la spéculation à court terme au profit d'investissements fiables et à long terme dans le financement participatif et les cryptomonnaies.

Grâce à une réglementation fiscale rationalisée et à des informations améliorées, les investisseurs peuvent désormais évaluer et atténuer les risques. Selon des enquêtes, la confiance des investisseurs dans les marchés des crypto-monnaies a augmenté d'environ 8 % en raison de la récente transparence.

Nous assistons également à un impact distributif plus important sur l'ensemble de l'économie alors que de plus en plus d'investisseurs ordinaires font leurs premières incursions sur ces marchés, grâce au renforcement des programmes de formation des investisseurs soutenus par les politiques et les recherches gouvernementales.

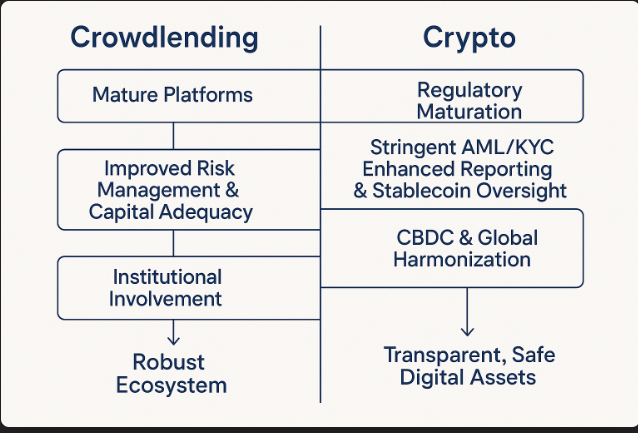

Visualiser le futur

Voici une figure ASCII mise à jour qui retrace l'évolution pour vous aider à comprendre comment ces modèles et les résultats de la recherche se sont combinés :

Développements futurs : tracer la voie à suivre

Le crowdlending et les cryptomonnaies présentent des perspectives intéressantes à mesure que le paysage financier britannique évolue, mais ils nécessitent également flexibilité et prévoyance. Pensez à ces développements à venir :

Alors que de plus en plus de plateformes de prêt participatif et de prêt cryptographique adoptent l'intelligence artificielle et l'apprentissage automatique pour améliorer les méthodes d'évaluation des emprunteurs, on s'attend à ce que les taux de défaut continuent de baisser et que la confiance des investisseurs augmente.

Une implication accrue des banques et des gestionnaires d'actifs conduirait à des normes de gouvernance et de gestion des risques encore plus strictes. La FCA continuera de modifier ses structures de surveillance afin de créer de solides programmes de protection des investisseurs capables de suivre le rythme de l'innovation rapide.

Réflexions finales : Vers un avenir d'innovation responsable

L'écosystème financier du Royaume-Uni connaît une transformation à la fois stimulante et passionnante. À l'ère numérique, le crowdlending et les cryptomonnaies sont bien plus que de simples termes à la mode ; ils redéfinissent la façon dont nous collectons, gérons et augmentons le capital. Les investisseurs, les innovateurs, des cadres réglementaires solides, des lois fiscales réfléchies et des connaissances étayées par la recherche constituent le moyen le plus sûr de garantir un avenir prospère.

Pour les investisseurs britanniques à la recherche d'une plateforme fiable et avant-gardiste alignée sur de solides valeurs réglementaires, Maclear propose une alternative d'origine suisse conçue pour la transparence, l'atténuation des risques et des rendements constants.

FAQ

Ces développements promettent de rendre le crowdlending et les cryptomonnaies plus sûrs, transparents et accessibles pour tous les investisseurs.