How Crowdlending Is Democratizing Access to Capital and Returns

28.08.2025

4

Updated:

18.06.2026

Banks and wealthy gatekeepers have controlled who’s permitted to gain funding for decades. But P2P tech is flipping the script. This fast-growing fintech model allows ordinary investors to rack up solid returns through fueling real-world projects. It's finance without the middleman, powered by technology.

But how exactly is crowdlending democratizing capital access? This detailed guide has all the answers.

Established corporate alone titans often have no problem arming themselves with good debt. The story hasn’t been so rosy for smaller companies and startups. The impediments to funding for these organizations are heavy. Thankfully, now crowdlending (or peer-to-peer lending) has come onto the scene to flip the status quo on its head.

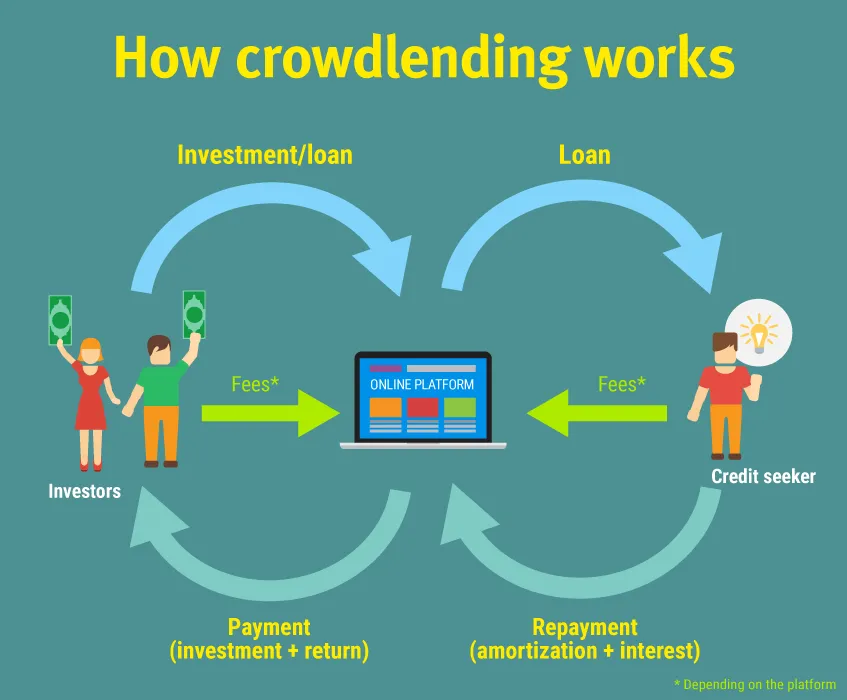

Crowdlending is a modern means of directly issuing and receiving credit between people or businesses through online platforms. Different forms of crowdlending have cropped up. But the concept was first observed during the 2008 financial crisis.

Banks reacted with stricter lending politics after the recession. Consequently, smaller businesses are challenged in preserving cash flow and securing credit. Many had to surf the web for unconventional alternative funding opportunities.

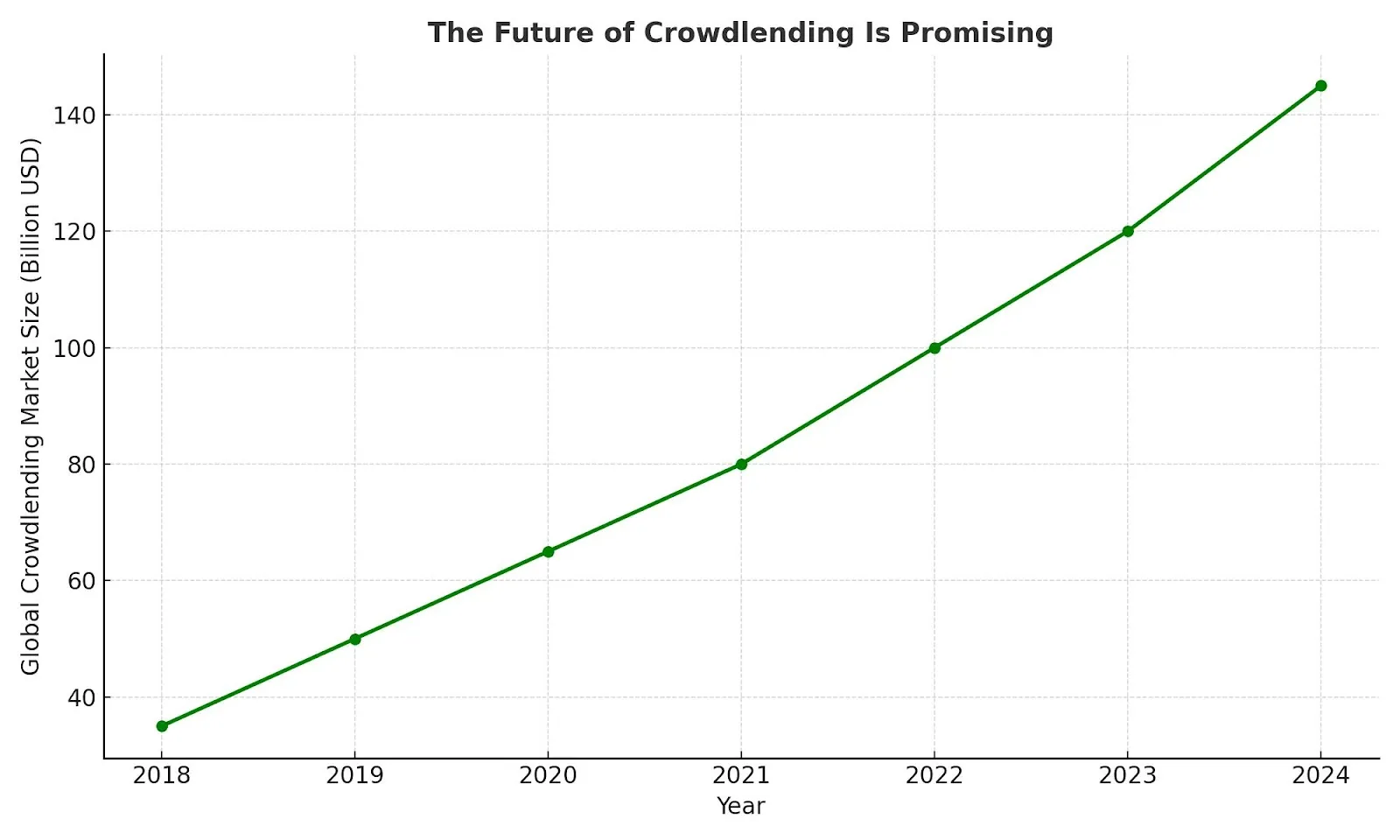

This field has grown tremendously ever since. The 2023 totals global crowdlending racked up soared to $1.17 billion, a projected $1.27 billion by 2028.

Tearing Down Barriers for Smaller Players

Crowdlending has redefined the playing field in favor of the underdog. SMEs and everyday entrepreneurs accessing funding through traditional banks can feel like they’re hitting a brick wall.

Long waits and high rejection rates often leave good ideas stuck on the sidelines. Crowdlending platforms change all that by opening the door to flexible financing. Small business owners can fund expansions or cover cashflow gaps without endless hoops. Individuals can secure personal loans without being penalized for not fitting the ideal borrower profile.

More borrowers are turning to crowdlending platforms because they focus on real potential. They can tell their story, set fair terms, and tap into support from people who want to see them succeed.

It's more humane and often much faster than traditional lending.

Investor Enticements

Completing the double whammy of the peer-to-peer is the dream it is for investors. These circumstances present investors a seat at the table once reserved for banks and big institutions. These individuals can now put their money directly into loans and earn interest like traditional creditors.

Low thresholds are the biggest draw for P2P platforms. Investors can allocate their resources across multiple loans to cut back risk and maintain a well-rounded diversified portfolio. This flexible investment opportunity is often more rewarding than passive investing in stocks or savings accounts.

Most platforms also provide key borrower information like:

Credit scores

Loan purpose

Risk ratings

This level of control and access was unheard of just a decade ago.

Benefit

Businesses

Individuals

Easy Access to Capital

Quick funding without traditional bank hurdles

Faster approval processes compared to banks

Flexible Loan Terms

Customized repayment plans suited to business cash flow

Shorter-term options with flexible amounts

Lower Interest Rates

Competitive rates due to reduced overhead on digital platforms

Often lower than credit cards or payday loans

Alternative to Banks

Ideal for startups or SMEs lacking credit history or collateral

Great for those with limited access to mainstream financial institutions

Community Support

Encourages brand loyalty when funded by customers or supporters

Feels more personal and empowering than dealing with large institutions

Speed and Convenience

Entire process can be done online, reducing paperwork and delays

No need to visit branches or submit lengthy applications

Repeat Borrowing Potential

Good repayment history builds credibility for future, larger funding rounds

Returning users often enjoy faster approvals and better terms

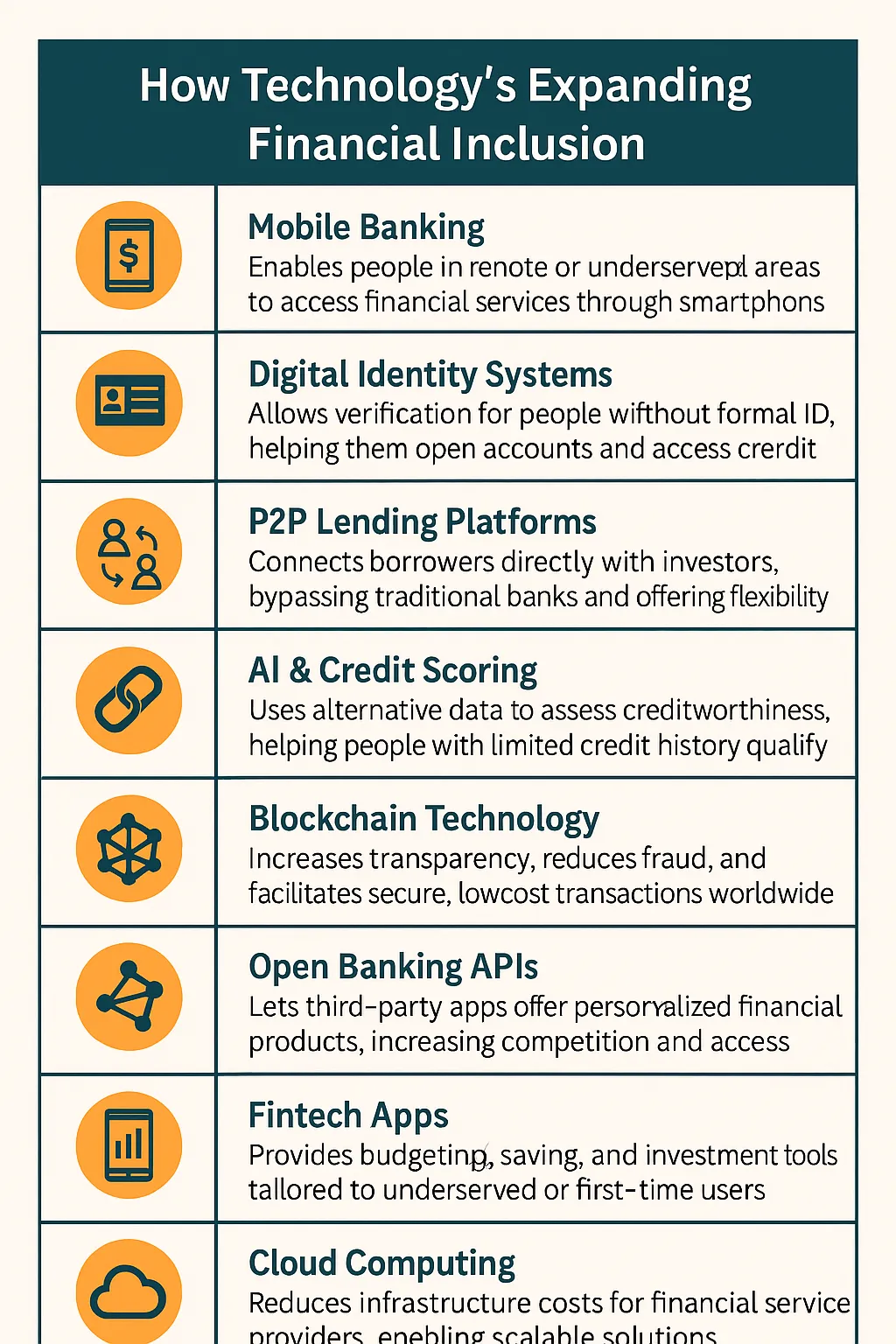

How’s Technology Expanding Financial Inclusion?

The crowdlending train wouldn't have become a success without technology. Innovative tech has enabled this shift to digital lending platforms. These solutions eliminate many of the traditional barriers that have long excluded people from investment endeavors. Credit providers can connect with borrowers from different locations and income levels in a few taps.

Innovation speeds up the loan process faster and renders it more transparent for borrowers. They get to decline dealing with enduring paper clutter and in-person meetings. Instead, they can apply on an app and get scored by algorithms that look beyond just credit scores. The funds can hit their accounts in mere days.

Investors are also reaping benefits, thanks to technology. Online lending platforms simplify decision-making and manage risk using data analytics and user-friendly dashboards. Anyone with internet access can browse loan opportunities and build a lending portfolio from home.

Familiarize Yourself with Risks and Regulation

Crowdlending may feel like a breath of fresh air compared to traditional finance. However, don't expect nothing but smooth sailing.

The potential returns are appealing to investors, but there is the possibility of borrowers defaulting. Consequently, smart investors even out the lending they provide among numerous loans and keep an attentive eye on platform-provided risk ratings.

Credit applicants must remain careful and responsible. Greater speed and flexibility compared to a bank don’t mean it's a free pass. Interest rates can climb depending on their risk profile, and missing payments can still hurt their credit scores.

Then there's the regulatory side. Financial authorities tightly regulate some platforms. They can't help but play by the rules and protect users. Others operate within grey areas with fewer safeguards. Crowdlending opportunities come with a degree of responsibility. Be sure to do your homework and read the fine print.

Real-World Success Stories in Crowdlending

We hear success stories of real people solving real problems through accessible financing every day. We've seen Individuals and small enterprises across the globe convert their dreams into a reality via crowdlending platforms.

The most notable examples are brands that created their own crowdfunding campaigns. Scottish BrewDog craft beer company and Glowforge, a U.S.-based 3D laser printer manufacturer, achieved major success through crowdfunding. BrewDog raised over £126 million through its Equity for Punks campaign on Crowdcube.

Meanwhile, Glowforge raised $27.9 million in just one month. The company used the funds to launch its product and attract further investment.

Likewise, businesses are making the most of peer-to-peer lending avenues. Maclear is one of the front-runners, the P2P lending platform facilitating over €18 million in funding and empowering small ventures with necessary capital flowing where it’s needed, backed by collateral.

Challenges Facing the Crowdlending Industry

Crowdlending platforms face their fair share of bottlenecks. The most prominent setbacks include:

Difficulty managing investor risk: Investors assume financial risks even on platforms that perform credit checks and generate ratings. Top P2P lending platforms aid investors in managing risk more effectively with advanced credit scoring algorithms and loan diversification tools.

Uneven regulation: Crowdlending regulations differ widely. Many platforms proactively cooperate with regional authorities to establish clear compliance frameworks and build trust in the financial system.

Building trust and credibility: Crowdlending happens online, so trust is everything. New lenders and borrowers are often ambivalent engaging in it due to fears of fraud or data misuse. Savvy platforms are navigating this using detailed borrower profiles, real-time tracking, and identity verification.

Platform scalability and quality: Constantly growing crowdlending platforms struggle to maintain consistent service, risk assessment standards, and borrower vetting. Automated systems and AI-driven underwriting are helping platforms scale while maintaining consistent loan vetting.

Market volatility and economic shifts: Economic downturns or inflation can hit crowdlending projects hard. The conditions increase defaults and reduce investor confidence. Platforms are adapting by offering flexible repayment plans, updating risk models, and facilitating user interaction.

The Future Is Still Promising

Crowdlending's future looks bright as global markets continue to embrace innovation. More countries are expected to pass thorough regulations for investor protection and market stability. We can also look forward to efficient and personalized crowdlending apps as more entities adopt AI for loan origination, risk assessment, and customer service.

Crowdlending platforms are increasingly facilitating fractional investments. Investors can now distribute small contributions across multiple loans to reduce their risk. Furthermore, there is a growing emphasis on ESG investing. More investors are supporting projects adhering to environmental and moral goals like Nigeria’s We Care Solar.

Blockchain integration improves transparency and streamlines loan processes through smart contracts and secure transactions. We're also seeing hybrid crowdlending models combine lending with equity or donation-based funding.

Finally, crowdlending platforms are diversifying their loan offerings. They're now including products like invoice financing and environmental loans to meet varying borrower needs.

Final Thoughts

Investors should keep a close eye on regulatory shifts and global expansion trends to stay ahead in the evolving crowdlending field. Go for a more diversified portfolio by exploring options like fractional investments and ESG-driven loans. You must also stay informed and adapt quickly to new models to gain a competitive edge.