You hit the road and hear that awful grinding noise. Big repair bills follow. You drive home later to find your basement flooded from a burst pipe. It always happens at the worst times.

It isn’t just the broken parts. It’s the sinking feeling as you figure out how to cover the cost without upending everything else. You might swipe a credit card and pay interest for months so that you can keep up with rent and utilities. Or borrow from family and face awkward conversations. Having a cash cushion for these surprises lets you stay calm and keeps your finances on track.

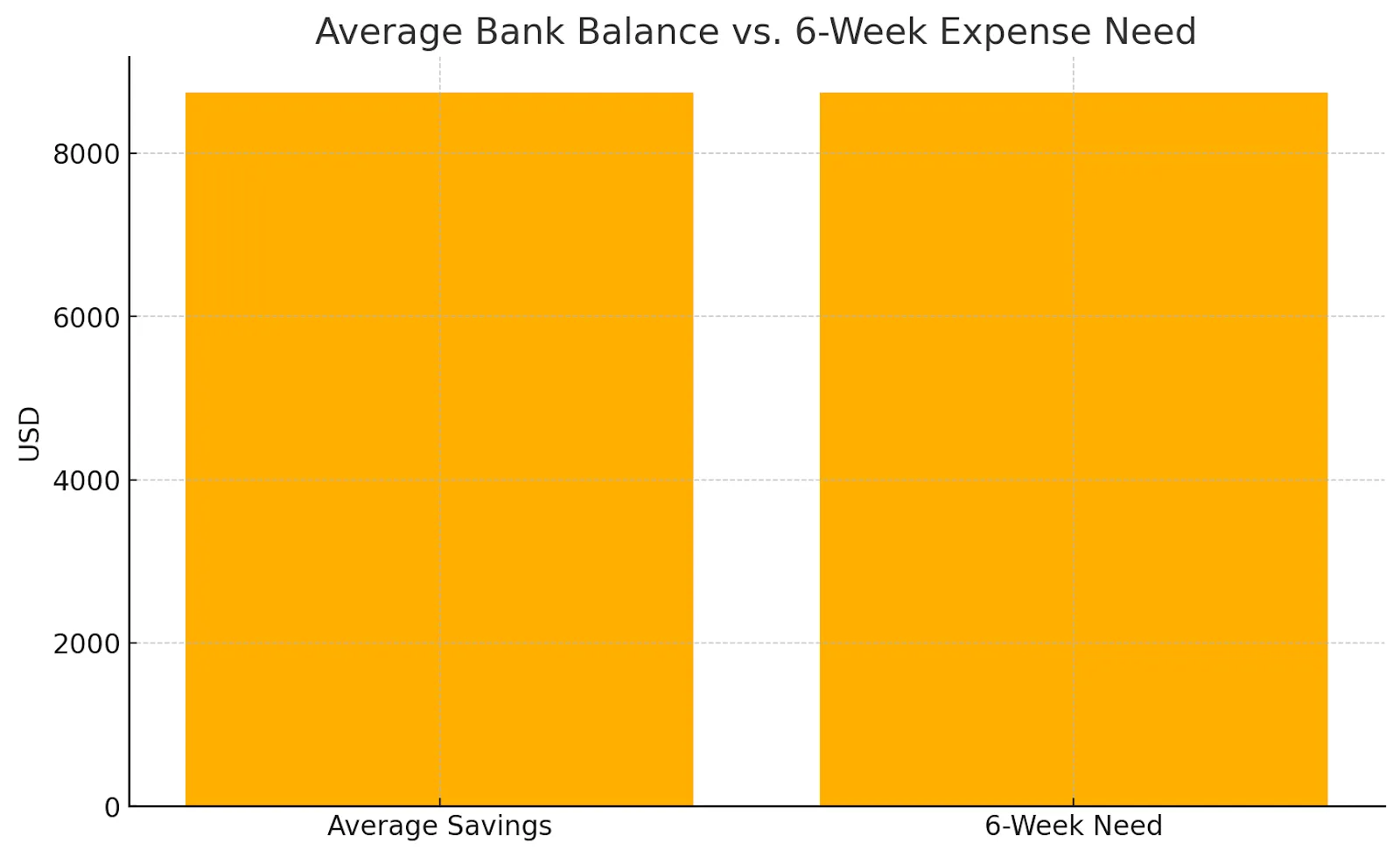

Most Americans aren't ready for financial emergencies. The average person had just $8,742 in their bank accounts in 2025, based on data from the Federal Reserve. That only covers about six weeks of normal household costs.

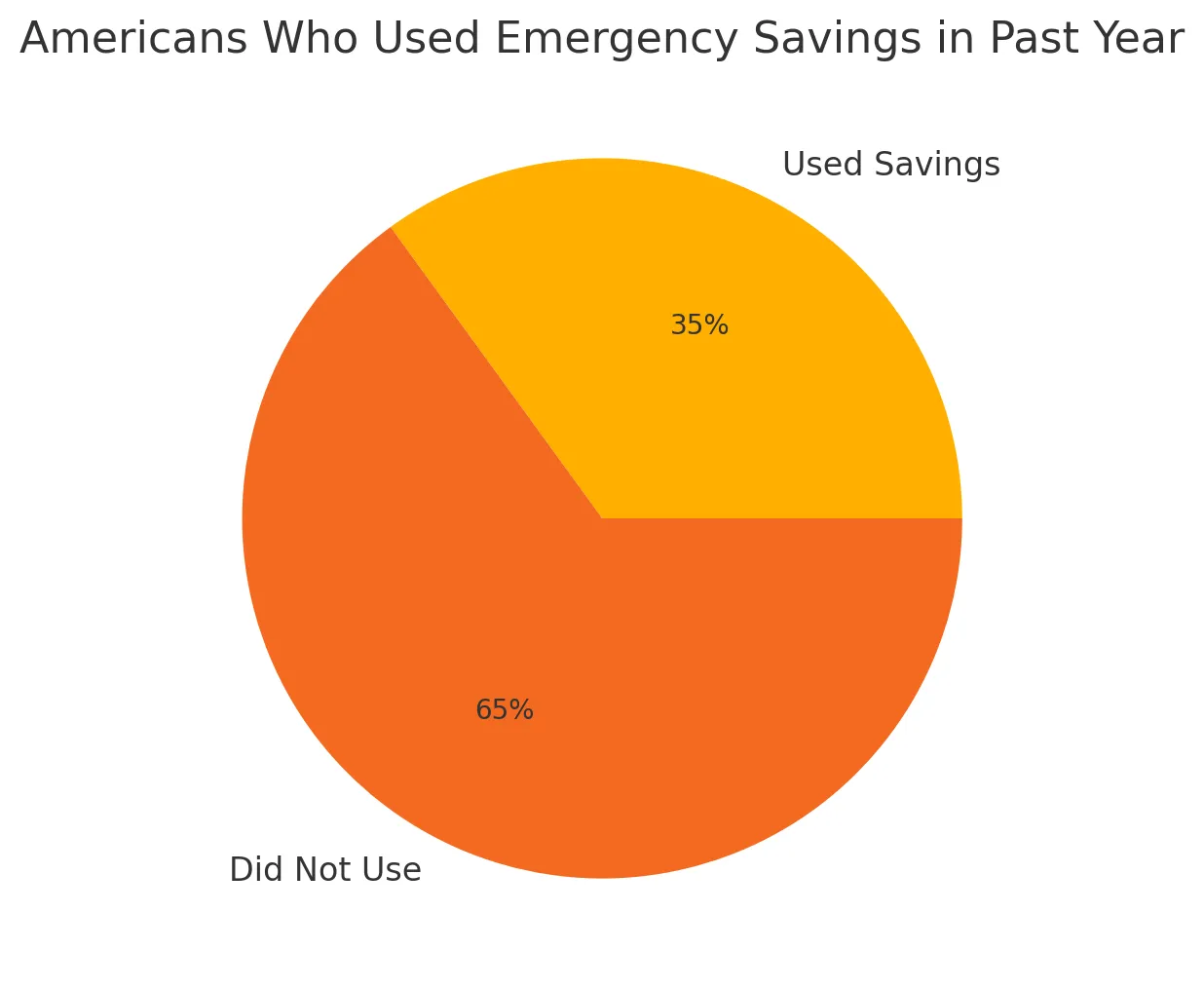

It gets worse. A 2025 survey by Bankrate found that more than one-third of Americans used their emergency savings in the past year.

Many used it for everyday expenses instead of real emergencies. This tells us that lots of families live so close to the edge that regular expenses feel like emergencies.

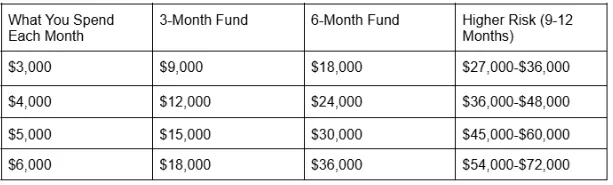

You've probably heard the advice to save three to six months of expenses. It sounds easy enough, but it leaves people wondering what that actually means in real money. Some experts say to start with $1,000. Others push for $2,000 at least. Recent studies suggest the average household needs around $35,000 to feel truly secure.

Two Types of Money Problems

Financial experts talk about emergencies in two different ways. Each one needs a different approach.

Surprise Expenses

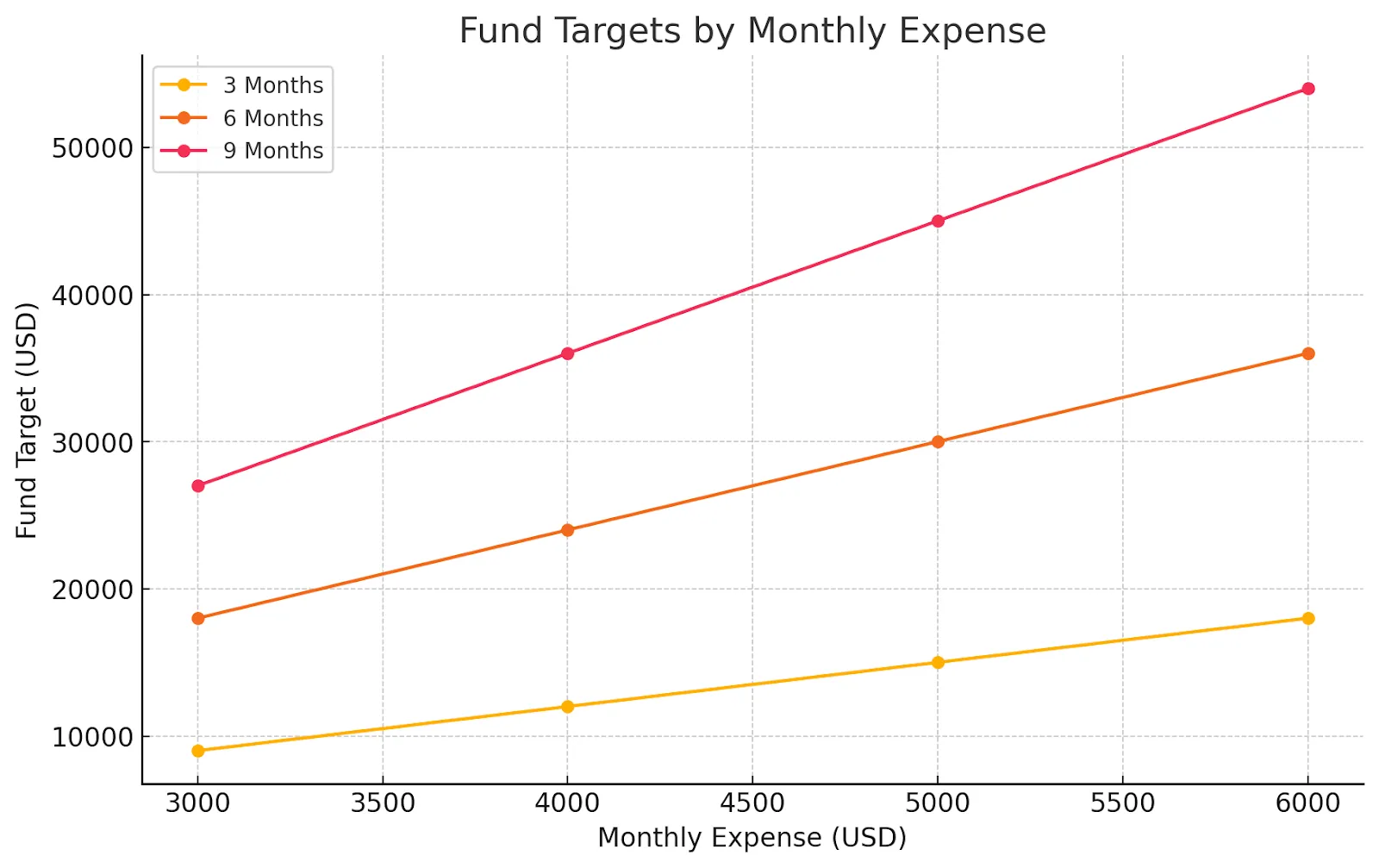

These are surprise costs like fixing your car, paying medical bills, or replacing a broken washing machine. Financial experts at Vanguard suggest having half a month's living costs or $2,000 saved up, whichever amount is bigger. This helps with the common money problems that pop up.

Unforeseen Blows

When big problems hit your wallet like losing your job, getting seriously sick, or having your pay cut way down, you still want to set aside 3-6 months’ cushion. So if you spend $5,000 every month, you'd want $15,000 to $30,000 total.

Determining Needs

You might need more money if your job is independent or purely performance-based. The same goes if you have health problems or you're the only person in your family who works. People who work in very specific fields might need more, too, since it can take longer to find a new job.

You might manage to drop that given a super stable job with good severance protection. If both you and your partner work and both jobs are secure, that helps too. Having low monthly bills that you can easily cut also means you might not need as much.

The Real Numbers

A recent study by Investopedia says the average American family needs about $35,000 in backup savings. That's equal to six months of emergency costs when you add up housing, utilities, food, getting around, and other must-have expenses.

Rainy Day Funds vs Other Money Goals

Balancing cushion savings with other goals means a plan that fits your situation. With high‑interest debt, save $500 to $1,000 first. Then attack debt so that you avoid deeper trouble, and once it’s lower, build your fund. With steady loans, build savings while paying minimums.

That mix gives peace of mind even if math favors extra payments. When your job matches 401 (k) contributions, grab the full match first, then build your backup stash before adding more to retirement. With no debt, finish your emergency fund first. That base protects all the progress you make.

If you’ve already covered your basic cushion fund, the next step is growing your wealth without locking it away for decades. That’s where Maclear comes in. By pooling your capital with other investors, you can fund high-impact businesses—from renewable energy startups to sustainable agriculture—and still spread out your risk. It’s investing that balances returns with real-world change.

How to Build Your Safety Savings Step by Step

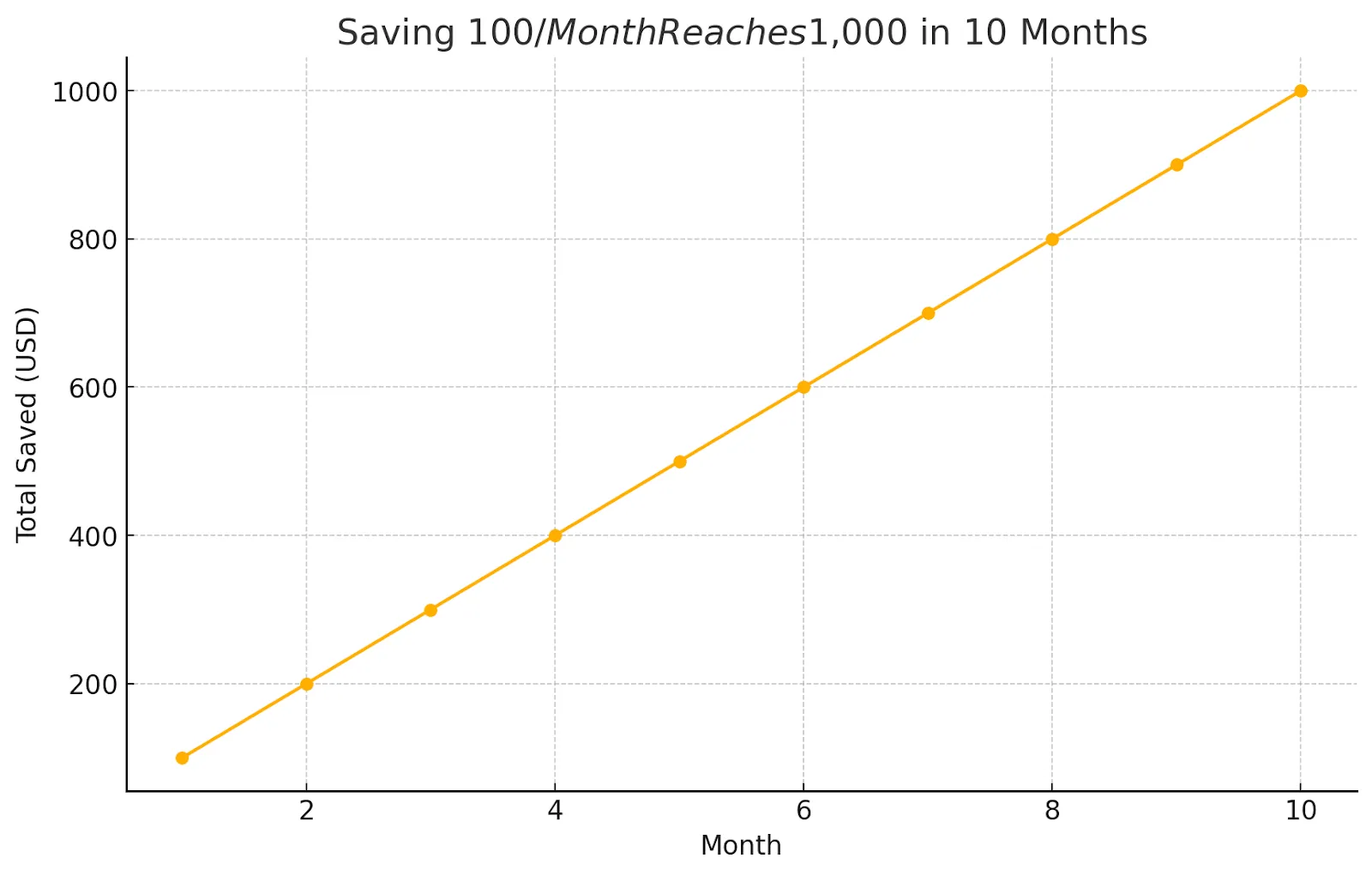

Step 1: Start small. Save $500 to $1,000. This covers minor emergencies without hurting your budget. Saving $100 a month gets you $1,000 in ten months.

Step 2: Build more. Aim for $2,000 or half your monthly expenses. That covers most surprises.

Step 3: Full cover. Work up to three to six months of essentials: rent, bills, food, transport, insurance, and loan minimums.

Set up automatic transfers so money moves on its own. Even $25 a week grows to over $1,300 a year. Try the 50/30/20 rule, saving 20%. Trim $100 of extras each month to boost savings.

Where to Keep It

Your safety stash needs to be easy to get to but separate from the money you spend every day.

Good Places to Keep It:

High-yield savings accounts that are FDIC-insured and pay good interest

Money market accounts that work like high-yield savings but might have extras like check-writing

Short-term CDs for money you won't need right away, since they pay a bit more

Places to Avoid:

Regular checking accounts because it's too easy to spend the money

Investment accounts because the value goes up and down, and you might not be able to get your money quickly

Retirement accounts, because you'll pay penalties and taxes if you take money out early

Mistakes People Make

Don't use your backup fund for things that aren't emergencies. Vacations and shopping don't count. Make separate funds for expenses you can predict. Don't keep too much once you reach your target. Send extra savings toward other goals instead.

Don't stop adding to your cushion fund. Check your target amount every year as your expenses change. Don't mix emergency money with other savings. Keep it in a separate account with a clear label so that you know exactly what it's for.

The Peace of Mind You Get

Cushion funds do more than just help with practical problems. They also help you feel better mentally. Research from Vanguard shows that people with at least $2,000 in backup savings spend much less time worrying about money. They worry for about 3.7 hours per week compared to 7.3 hours for people without emergency savings.

This mental space that gets freed up lets you focus on other important things. You can take smart career risks and approach life with more confidence.

Changing Your Plan as Life Changes

Your needs change as your life changes, too

In your early career, focus on getting that first $1,000 to $2,000 saved up. During your family years, increase your targets as your expenses grow. When you're earning the most money, balance emergency funds with retirement and education savings. Before you retire, think about emergency funds as part of managing all your cash.

What to Do Next

Building an emergency fund takes time. Each dollar you save makes your money stronger. First, list your monthly basics and pick a savings target you can meet. If you don’t have one yet, open a high‑yield savings account. Then set up automatic transfers and start with an amount that feels easy, so that you stick with it.

Even $25 a month adds up. A solid emergency fund does more than hold cash. It brings that calm feeling when life throws you a curveball. Spend a few minutes now to check your savings and make one small move toward your safety net. Your future self will thank you for that peace of mind..

Once your emergency fund is in place, your money can go from sitting safely to working actively. Maclear connects you with purpose-driven businesses worldwide, offering competitive returns backed by innovative credit scoring and a shared-risk model. Your capital doesn’t just grow—it helps unlock funding for ventures that make a difference.