France's P2P Lending Regulatory Framework: The Role of the AMF and ACPR

07.10.2025

5

Financial innovation rarely thrives under chaos seeing as too many regulations bury creativity in red tape. On the other hand, sparse and vague regulations kill trust among industry players and leave investors open to risks they never had a chance to see coming.

France's P2P lending industry has found a delicate middle ground between the two extremes using two regulators with differing but complementary roles.

The Autorité des Marchés Financiers (AMF) and the Autorité de Contrôle Prudentiel et de Résolution (ACPR) are doing more than enforcing regulations. They're establishing guardrails that empower fintech platforms and keep investors protected from risk, and in doing so, they're building a solid future digital finance space for France.

This piece uncovers the role these bodies play in building France's peer-to-peer, or P2P, alternative finance market, including the latest statistics, changes in regulation, and enacted investor protections. We’ll use anecdotes and insights to highlight why France is still one of Europe's safest yet most momentous P2P lending sectors.

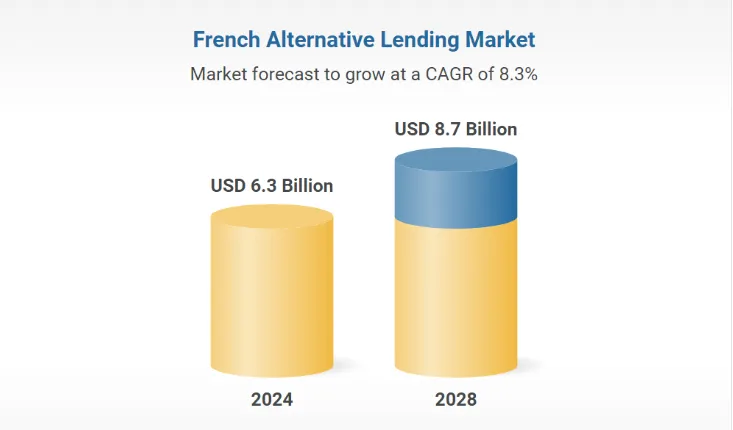

France's fintech sector is thriving in 2025. Fresh Statista figures show that France is home to almost 950 fintech companies, with P2P lending a primary catalyst for alternative finance.

According to a 2025 report published by the AMF and ACPR Joint Unit, France's P2P lending market has grown exponentially, reflecting steady growth since the ECSPR came into effect.

The application of the revised EU Crowdfunding Regulation (Regulation (EU) 2020/1503) that fully came into force as of November 10, 2023, harmonized investor protection across Europe and gave French platforms a passport they could use to expand seamlessly across EU borders.

In this momentous and well-regulated ecosystem, platforms like Maclear combine cutting-edge credit scoring with a diversified investment approach. Maclear empowers businesses that might otherwise face barriers to credit while offering investors attractive returns through risk-distributed lending backed by collateral.

The AMF: Vigilante for Investor Honesty

The AMF is France's gatekeeper to the financial markets. Its regulatory mandate sets the standard for every P2P lending platform that wants to conduct business within the country.

Here are some of the AMF’s main guidelines for P2P platforms.

Strict authorization and monitoring

The AMF must authorize every crowdlending platform before it can start operations within France. That means only crowdfunding platforms that meet high standards for risk disclosure, due diligence, and operating transparency.

EU standard harmonization

The AMF sees to it that all platforms adhere to uniform rules, e.g., funding caps per project of up to €5 million over 12 months per project holder. That provides safety and transparency within the community.

Better risk management

Platforms must update precise risk metrics and project disclosures. This level of regular transparency gives investors a way to make genuinely well-informed decisions in a changing market.

The AMF is like a careful maître d' of an upscale Parisian restaurant in that it only lets in that it ensures the ‘menu’ is full of only top-tier platforms that give investors the best experience possible.

The Role of the ACPR: Custodian of Financial Stability

While the AMF focuses on market integrity, the ACPR holds a broader vision for financial prudence. Its functions are mostly about the general well-being of the financial system, even parts that indirectly apply to P2P lending.

Here are some of the ACPR’s core responsibilities:

Prudential supervision & capital adequacy: The ACPR requires platforms to maintain capital cushions that amount to at least 120% of operating costs to be immune to market shocks.

Risk-based supervision: According to the ACPR’s 2025 work program, the regulator is stepping up its digital and risk-based supervision. That includes early detection of vulnerability, particularly with the new phenomenon of blockchain and tokenization.

Integration with European initiatives: The ACPR keeps French practices competitive, resilient, and fully integrated into the overall EU framework through tight integration with European regulatory bodies (like the EBA).

If the AMF is the maître d', then the ACPR is the backstage support team that works tirelessly to ensure the entire restaurant stays afloat and functions like clockwork, even if that means overseeing every ingredient.

The French Regulatory Framework: Innovation Meets Protection

France's P2P lending infrastructure is multi-layered and rich in frameworks that go above EU minimums.

Here’s a snapshot comparing EU minima with French "gold-plating" demands:

Regulatory dimension

EU (Regulation 2020/1503)

Minimum French Enhancements

AMF/ACPR

Investor onboarding

Basic risk tests, standard asset disclosures

Enhanced risk disclosures, periodic updates, and, in some cases, mandatory psychometric assessments

Marketing & communications

Prohibition on misleading claims

Strict bans on terms like "guaranteed return" or "savings account" style language to avoid deposit-like promises

Liquidity and capital standards

Requirement for segregated accounts

Daily reconciliations, third-party audits every six months, and robust capital buffers covering at least 120% of operating costs

These additional protective layers give investors confidence, especially seeing as the AMF and ACPR only give authorization to platforms that meet these strict standards.

New Regulatory Developments and Policy Changes within France’s P2P Space

French regulators are continually evolving according to the demands of a digital financial world:

EU Crowdfunding Regulation is in full swing. After a one-year postponement, Regulation (EU) 2020/1503 took full effect on November 10, 2023. That heralded the dawn of a new era of market transparency and cross-border operability for French P2P platforms.

The AMF recently increased the risk frequency and level of disclosure. The body now requires platforms to publish more granular, near real-time project risk and borrower performance information, thereby keeping investor information as current as possible.

Furthermore, kicked off in January 2025, the ACPR's work program focuses on enhancing risk-based supervision, digitalization, and early financial vulnerability warnings. Recent ACPR and AMF reports demonstrate a growing emphasis on incorporating ESG (Environmental, Social, and Governance) considerations into financial risk analysis as well.

Investor Strategies for Optimizing Returns in the French P2P Landscape

While it’s always best to create a personalized investing plan, here are some strategic ways to optimize your returns on capital invested in the French P2P market:

Diversification is key: Diversify investments among loan types (consumer, business, property). Additionally, diversify across multiple platforms to reduce exposure to risks from any one provider.

Prioritize secured loans: Partners offering collateral-backed loans (e.g., lending against property) tend to carry lower default risks. Screen Loan-to-Value (LTV) ratios; a low LTV suggests stronger security for investors.

Stay current with regulatory updates: The ACPR's 2025 work program prioritizes new risk-based supervision. Investors should observe how this affects lending platforms. The AMF's reinforced disclosure rules give investors more frequent access to risk information. Use this basis to make tactical adjustments.

Optimize tax efficiency: France's streamlined 30% tax (PFU) on P2P lending returns is a reduction from typical income tax rates. As a consequence, investors should model portfolios. Investors can also claim Wealth Tax (IFI) if net assets are below €1.3 M.

Market Insights: French P2P Landscape Trends to Watch in 2025

Here are some key insights you should monitor in 2025 and beyond to stay informed about what’s happening in France’s P2P lending industry.

Institutional asset managers and banks are collaborating with platforms to introduce higher governance levels and more secure funding sources.

The simultaneous ESG focus of the AMF and ACPR will lead to platforms dealing in green finance or social impact loans due to increased investor interest.

The ACPR’s 2025 roadmap has tokenized bond tests. The move promises to introduce new liquidity sources for P2P investors.

Conclusion

France's regulatory landscape for P2P lending is like a finely balanced French cocktail. The prudent oversight of the AMF and ACPR encourages platforms to innovate within the guidelines that use transparency and risk management to safeguard each investment.

As you dive into this dynamic, ever-evolving world, be sure to keep current with developments from respected sources like the AMF, ACPR, Statista, and the Cambridge Centre for Alternative Finance.

For investors and businesses looking to participate in the next generation of crowdlending, Maclear offers a secure, profitable platform built on transparency and advanced risk management. Discover how Maclear’s Swiss-rooted model is perfectly aligned with France’s strict regulatory standards.