No one wakes up stoked about paying taxes. That goes without saying, so that’s quite a treat when they provide us an avenue to skip on paying them. It’s the government’s job to incentivize continued behavior among citizens to contribute to make way for a more prosperous, future-focused nation. Such vehicles simultaneously help provide people the benefits they need while reducing strain for the public doll and follow programs that serve vital necessities.

The government thus creates savings vehicles through fiscal exceptions should they elect to allocate funds toward healthy causes. New signups may think of these as legally sanctioned fiscal shelters.

That said, people who are totally ignorant of them won’t be able to take advantage of these. Too many people get scared off thinking that those hairy programs are too much of a bother to manage. In reality, such programs are meant for ordinary Joes to do just that.

Special-purpose savings plans are not all created to serve the same ends. Rather they all have their own ends which align with particular priorities.

Pension

All too many people fail to stash earnings away for their pensions. And the government firstly wants people to prepare responsibly for the day the grocery store clerk and the saw mill worker and the garbageman grow into their twilight days on one hand. On the other hand, if they don’t set aside money, that’s going to put a lot of strain on the nation’s young to provide for their needs.

Nearly half of American households don't have any retirement savings. These folks miss out on breaks and even free money from their employers. Not saving early enough for pension ranks as one of people's biggest money regrets. The intricacies and terms can feel overwhelming, so an old fashioned one is simpler to grasp. It's easier to just stick with a regular savings account. But that means you're probably paying more .

401(k) and 403(b): You pay straight out of your paycheck and a lot of the time your boss matches it

457(b) Plans: like the one above but for public employees as well as some nonprofit employees. You walk away with your money no matter how old when you vacate your occupation.

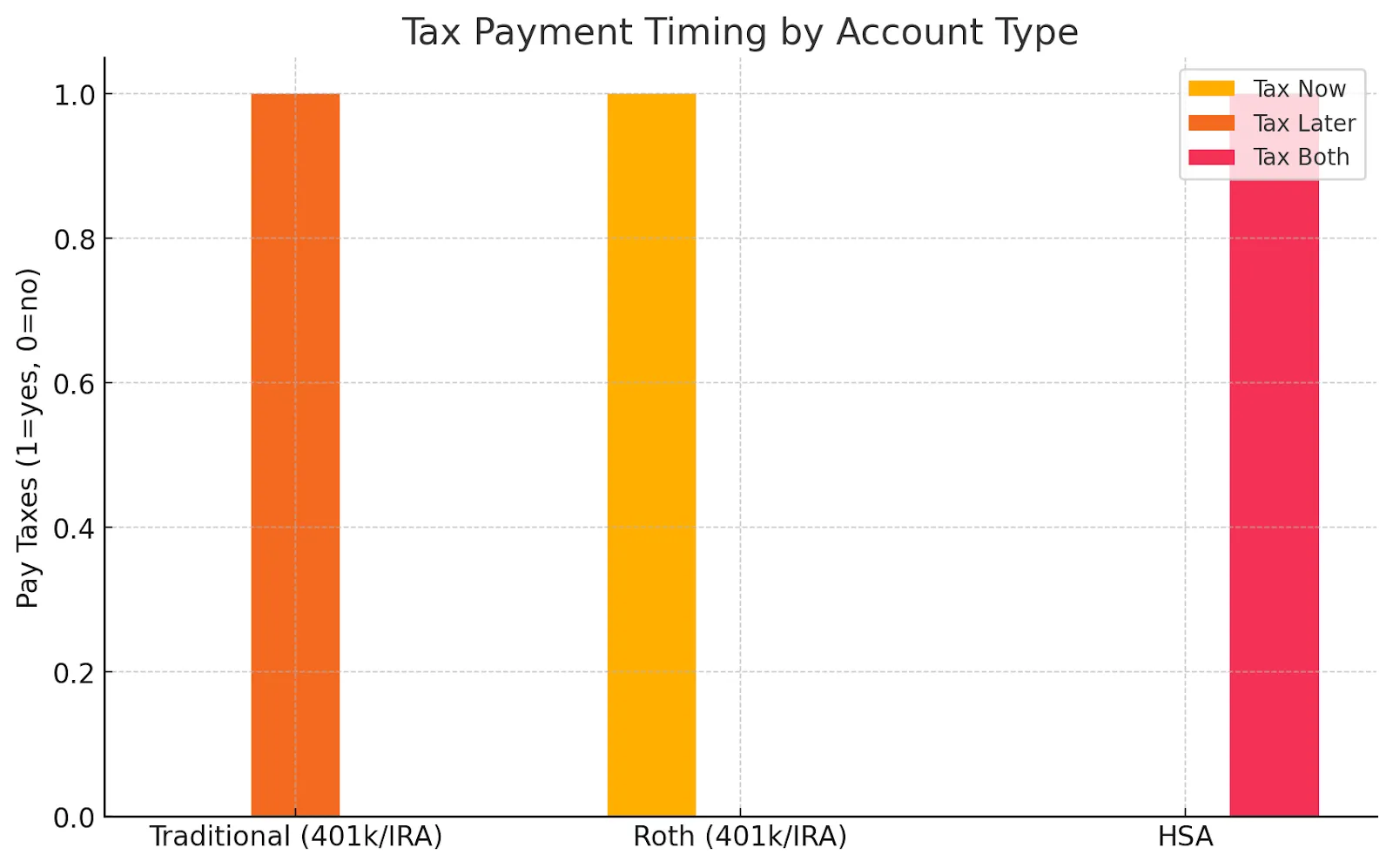

Individual Retirement Account: the older one, where you open it yourself and you only pay taxes when you withdraw, possibly even no taxes if you stick to the regulations.

Traditional IRA: An account you open yourself. Contributions may be tax-deductible, and investments grow tax-deferred until withdrawal.

Roth IRA: Popular with younger savers who expect to be in a higher tax bracket later.

SEP IRA: self-employed people or small businesses, with more able to be deposited than other such independent savings vehicles.

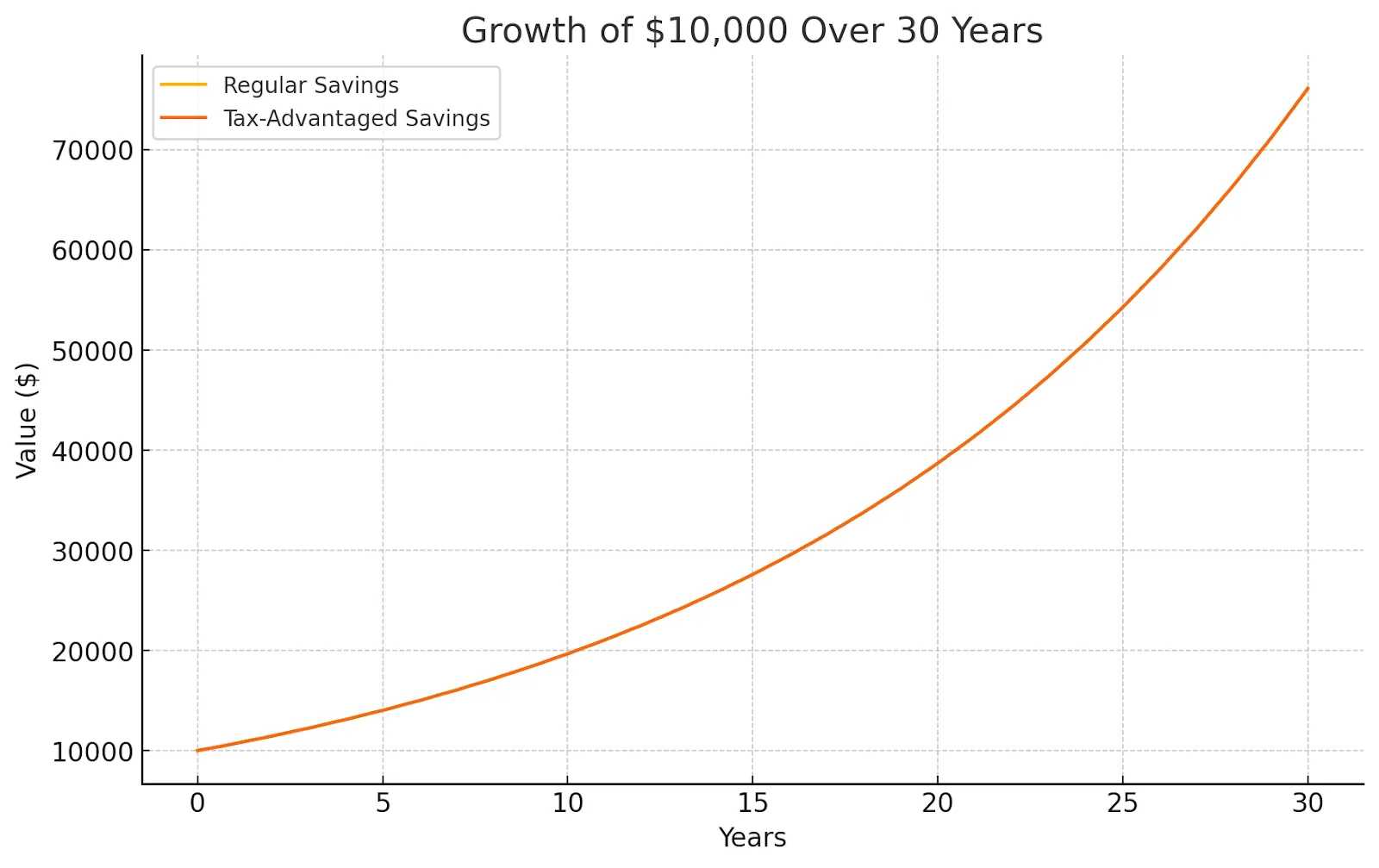

Maria, a 32-year-old marketing manager, has always struggled to put money aside for retirement. When her employer offers a 401(k) plan with a dollar-for-dollar match up to 5% of her salary, she decides to contribute the full 5%. This means for every $200 she puts in per paycheck, her company adds another $200 — instantly doubling her savings. She chooses a mix of index funds for long-term growth.

Because her contributions are tax-deferred, she lowers her taxable income each year. By the time she’s 65, the compound growth and employer matches turn her consistent contributions into a seven-figure nest egg. She’s essentially used the tax rules and her employer’s incentives to make retirement financially comfortable without having to “feel” the savings pinch too much today.

Healthcare

In United States, people pay many times more what people pay in other developed countries. An X-ray in Japan costs ten times less than in USA, as does the typical pill in Great Britain. Fortunately, most people’s bosses there have to feed into FSAs as per the law. Workers get to use money for their health before taxes, although they have stricter rules, since they have to be used or you don’t get to enjoy the benefits.

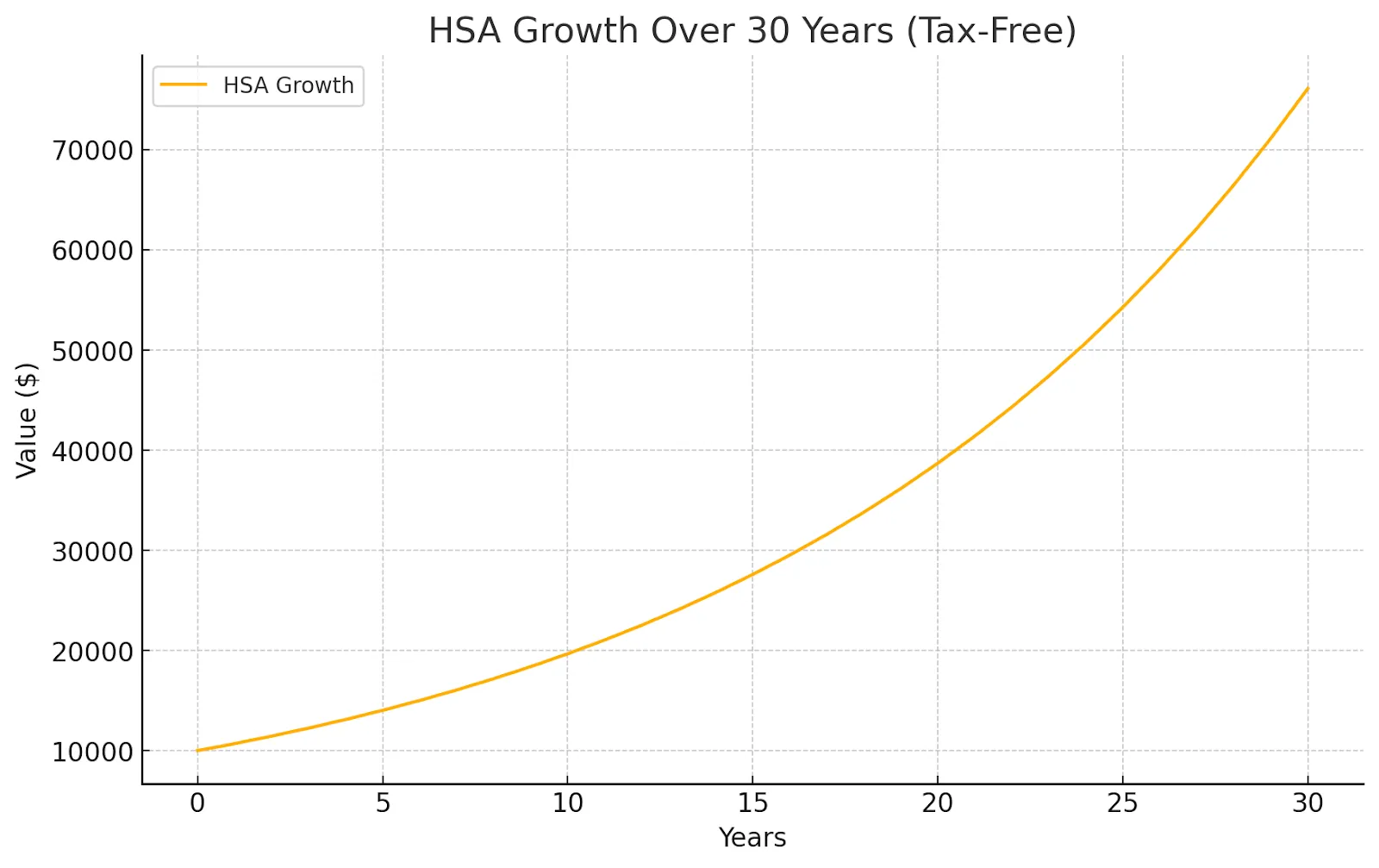

James, a 40-year-old freelance graphic designer, opts for a high-deductible health plan to keep monthly premiums low. He opens an HSA and contributes $3,000 for the year. He invests part of the balance into mutual funds so it grows over time — tax-free.

When James needs a $1,500 dental procedure, he pays for it directly from his HSA. Not only does he avoid paying taxes on the money used for the treatment, but the investment growth in the account continues untouched for future healthcare needs.

For his part-time teaching job, he also uses an FSA to cover predictable expenses like prescription eyeglasses and annual check-ups. By using both accounts strategically, he reduces his taxable income while ensuring medical costs don’t eat into his emergency savings.

College and Schooling

Vehicles like these are a serious economic driver and non-public donations totalled 61 billion in private donations in 2024. So people with such kinds of accounts get their expenses relaxed for schools.

529 plans

Coverdell

This can apply not only to college but also children’s schooling, like in the latter case, the former including a potential prepaid tuition plan.

Priya, a 29-year-old software developer, wants to give her 2-year-old daughter a financial head start. She opens a 529 plan and contributes $200 a month. She chooses aggressive growth investments while her daughter is young, knowing she has 16 years before the funds will be needed.

Years later, when her daughter is accepted into a top-tier university, Priya withdraws the money tax-free to pay for tuition, books, and even on-campus housing. Thanks to years of compounded, tax-free growth, the account has doubled in value, allowing Priya to cover a major chunk of costs without resorting to student loans.

ABLE Savings Plans for Invalids

Designed for disabled individuals to put away cash or buy assets and still uphold their right to public health programs. Their deposits are usable in housing, education, and assistive technology.

Samantha’s younger brother, Ethan, has a disability that limits his earning potential. She helps him open an ABLE account, where contributions grow tax-free and can be used for disability-related expenses without jeopardizing his eligibility for government assistance. Over time, the account funds things like adaptive technology, transportation, and continuing education courses.

Meanwhile, in another example, Anthony — a single father — uses an Individual Development Account (IDA) offered through a local nonprofit. For every $1 he saves, the program contributes $3. Within three years, he has enough to launch a small catering business, all while receiving financial literacy training as part of the program.

Alternative Avenues

Government programs and employer benefits can help you save, but your money doesn’t have to stop there. While traditional tax-advantaged accounts protect and grow your wealth slowly, crowdlending platforms like Maclear let you put part of your savings to work funding real-world progress.

Maclear uses advanced credit scoring to connect investors with businesses that would otherwise struggle to access credit — spreading the risk among many backers while offering competitive returns. It’s a way to keep your money moving forward, not just sitting in an account.

Smart Strategies for These Accounts

Now let's talk about how to use these accounts wisely.

1. Get Your Employer to Match First

Free money should always be your priority. If your employer matches 401(k) contributions, put in at least enough to get the full match. Where else can you get an instant 100% return?

2. Pick the Right Order

Here's a common approach that works well:

401(k) up to the employer match

Max out your HSA (if you have one)

Contribute to an IRA (Roth if you qualify)

Put whatever’s left back in your 401(k)

3. Think About Your Taxes

Pick between traditional and Roth, based on your situation:

Go with Roth if: You're young, don't make a ton of money yet, or think taxes will be higher when you retire

Go Traditional if: You're in your peak earning years and expect to have less income in retirement

4. Leave It Alone

Taking money out early hurts in three ways. You pay taxes. You pay penalties. And you lose all that future growth. When you switch jobs, roll your old 401(k) into an IRA or your new employer's plan. Don't cash it out.

Here are some mistakes people make:

Not getting the full employer match – This is free money you're passing up

Forgetting about HSAs: People miss out on the only triple-tax-advantaged account

Picking the wrong type: Think about your tax situation before choosing traditional or Roth

Playing it too safe: With decades until retirement, you probably need investments that can grow

Not increasing contributions: As you earn more, save more

Wrapping It Up

Tax savings vehicles are powerful in building wealth. But beginning now is key – time is the necessary ingredient for a strategy to really pay off. Benefits get better the longer they’re liberated from fiscal burdens. Even small amounts matter. Open an account, automate savings, and bump them up when possible. Years later, you'll be so glad you protected them from extra taxes.

Once your savings vehicles are operating, make your money work for good. With Maclear crowdlending, you get to back high-impact ventures and earn steady returns – without the volatility of the stock market.