P2P Lending in Europe: Austria, Italy, and Bulgaria Leading the Charge

15.09.2025

5

Peer-to-peer (P2P) lending is transforming business access to capital throughout Europe. Rather than having to apply for bank loans, with P2P lending, borrowers can get a loan directly from individual lenders through online platforms.

This model is seeping through all regions and industries, especially in countries where small and medium-sized enterprises and startups have particular difficulties obtaining financing. Austria, Italy, and Bulgaria have differentiated themselves among their peers, earning reputations as strong players in this sector, each exhibiting spectacular figures.

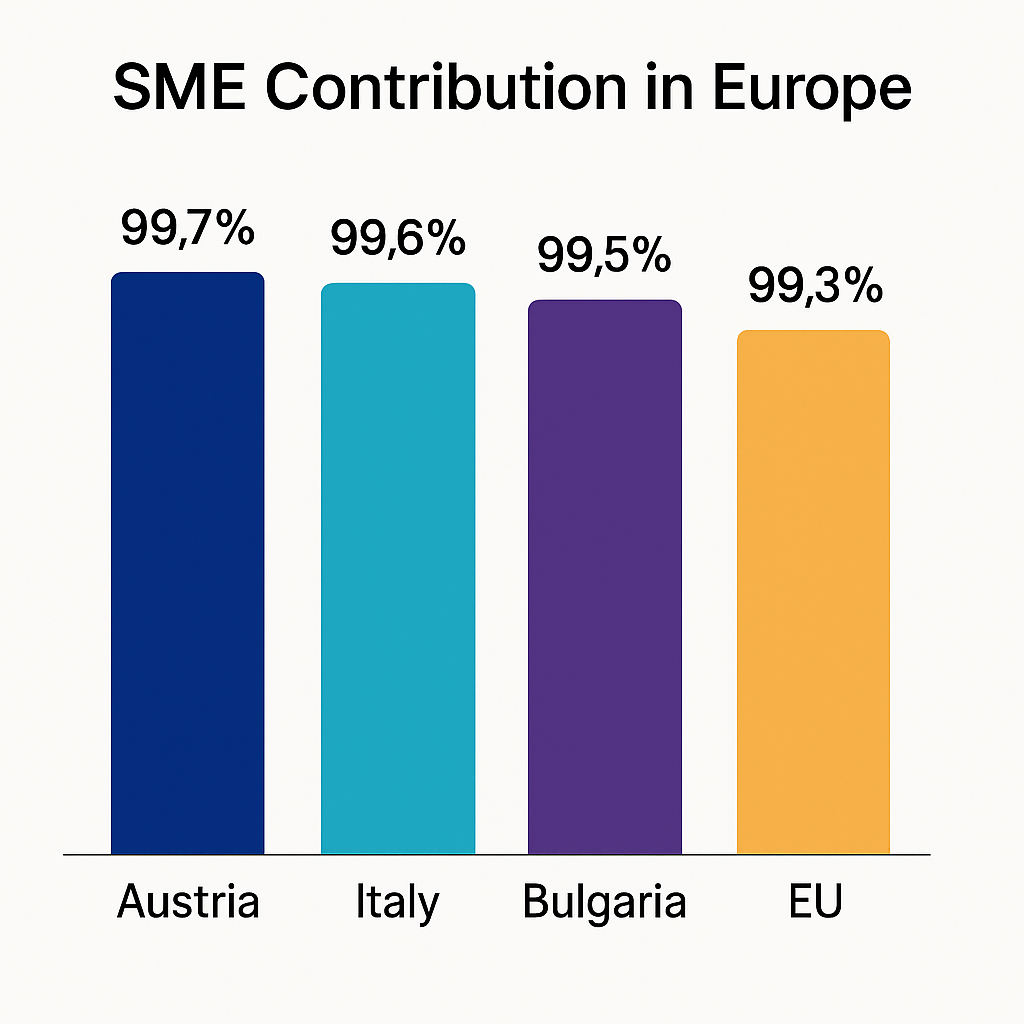

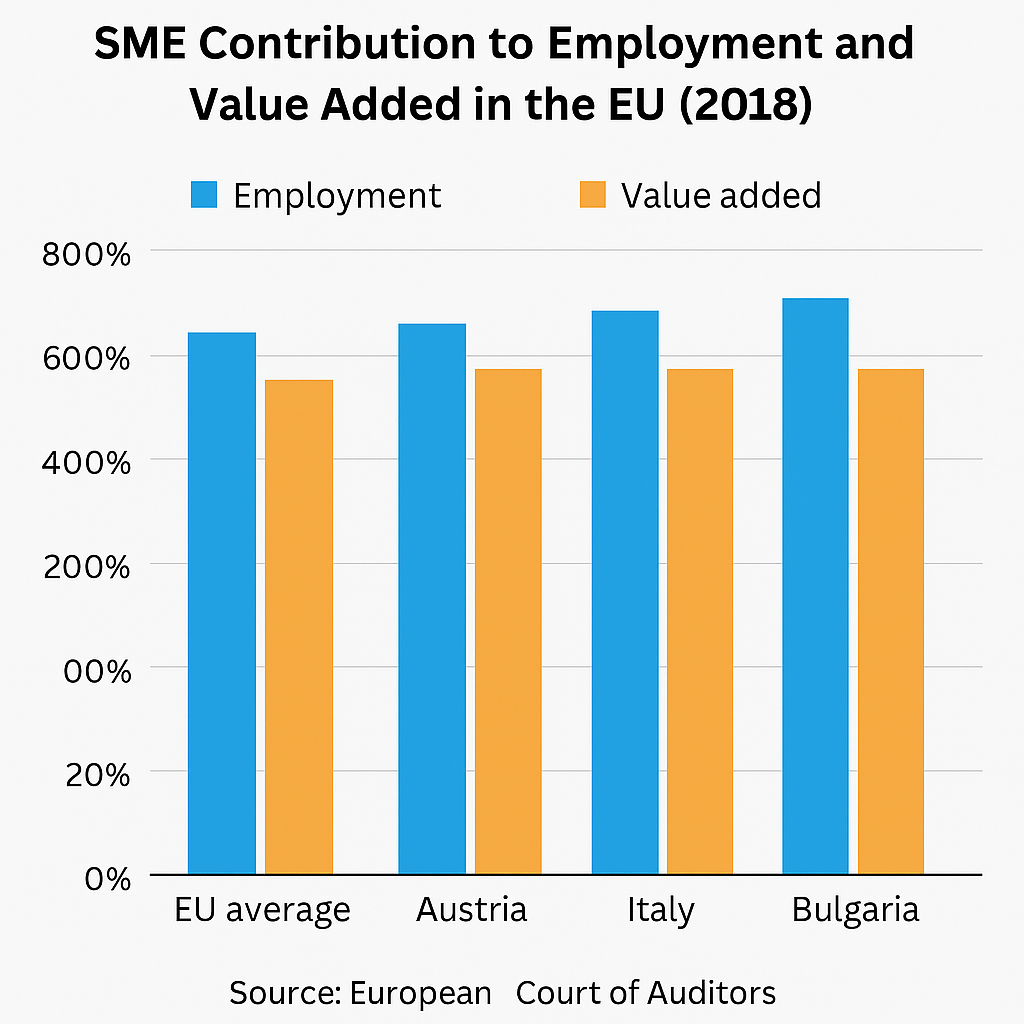

More than 99% of all businesses in Austria are SMEs, which have a strong hold on their economy. More and more of these enterprises are looking for fresh new lending sources.

The Austrian government has created an entrepreneur-friendly environment for fintech’s growth. The Financial Market Authority (FMA) decided to implement a regulatory sandbox in 2020, whereby companies with new business models would first be given the opportunity to test the regulatory sandbox. This program helps to initiate innovation while safeguarding consumers.

Subsequently, in 2022, Austria passed the Crowdfunding Enforcement Act, bringing national regulations up to the EU’s crowdfunding regulations. Such harmonization ensures legally sound P2P lending platforms, as well as boosting investors’ confidence.

Austria is a seductive ground for P2P lending because of the presence of its robust SME sector and a regulatory environment striking a balance between innovation and supervision.

Italy: Rapid Growth Amidst Economic Challenges

Italy’s market is supported by the exceptional nature of the economy there. Many Italian firms are family-operated SMEs that regularly struggle to obtain conventional bank loans. Nevertheless, peer-to-peer credit with flexible terms for companies there has been all the rage.

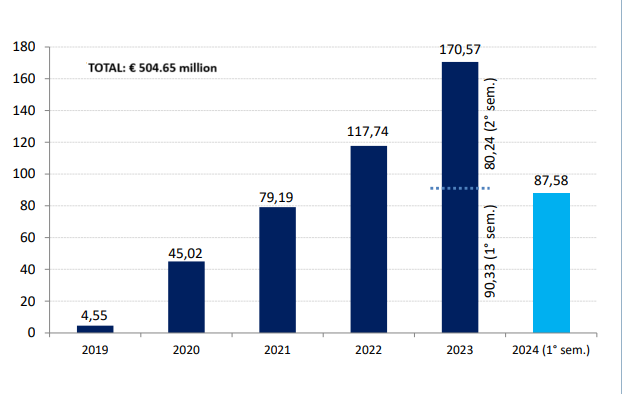

The legal environment has been simplified by the adoption of the ECSP Regulation in Italy. The number of authorized crowdfunding platforms that exist in the country was an impressive 33 as of June 2024.

During the first half of 2024, business direct lending platforms in Italy attracted €167.82 million, up 7.7% from the previous period. Real estate projects, in particular, demonstrated emboldening growth, as a 9.82% annual interest rate was offered to business credit.

The Italian alternative loans market is expected to reach US$8,412.4 million by 2027 and increase with a Compound Annual Growth Rate (CAGR) of 8.8% during 2023–2027.

Bulgaria: Empowering Startups and Rural Enterprises

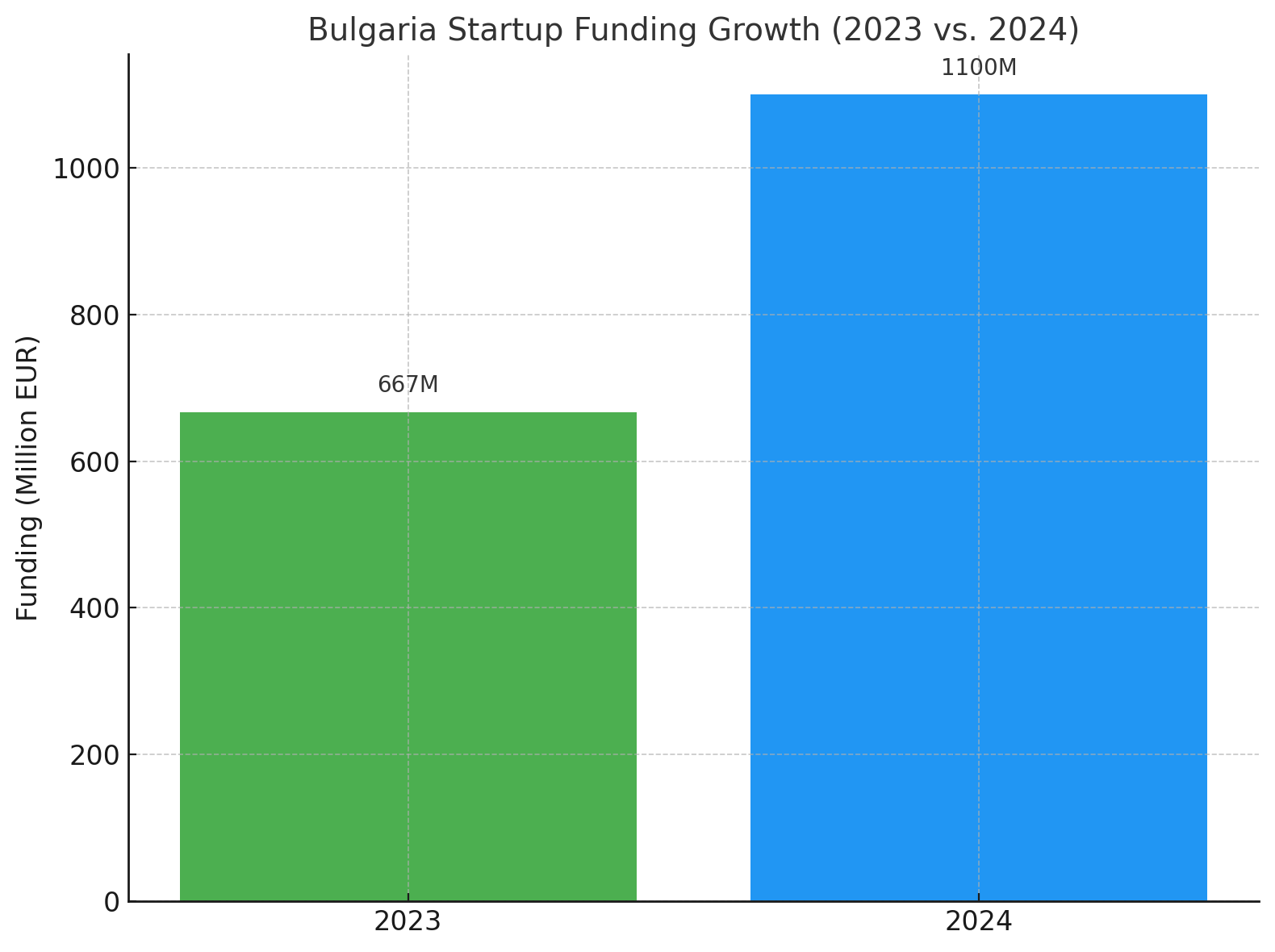

Bulgaria is a new blooming center for startups in Southeast Europe, and peer-to-peer loans is at the core of this new movement. In 2024, Bulgarian startups raised €1.1 billion, a 65% increase compared to the previous year.

The absence of specific P2P lending regulations in Bulgaria has been no impediment on the sector's growth. This is because platforms such as Maclear are now extending personal loans to prime customers to fill the void left by traditional financial institutions. Decentralized credit is especially sought after in construction, logistics, and agriculture in Bulgaria.

Several incentives are available to investors in Maclear:

Users who register receive a €10 bonus.

14.9% return on any investments.

Both parties receive a 2% bonus of their friends’ investments within their first 90 days of investing for those who refer friends.

Loyal investors don’t go unmentioned either. Depending on the total amount invested, they can earn an additional 2% per annum.

Furthermore, with a straightforward dashboard, Maclear ensures that the investors follow up with their investments effortlessly. And with auto-invest and a secondary market planned as a new feature to come, Maclear is prepared to be friendlier and more convenient to use.

Comparative Overview: P2P Lending Landscape in Austria, Italy, and Bulgaria

Country

SME Contribution to the Economy

Regulatory Environment

P2P Lending Growth

Key Sectors Benefiting

Australia

Over 99% of businesses

Clear fintech regulations

Thriving SME sector

SMEs across various industries

Italy

High number of family-owned SMEs

Streamlined under ECSP Regulation

Projected to reach $8.41 billion by 2027

Real estate, business lending

Bulgaria

Vibrant startup ecosystem

No specific P2P regulations

€1.1 billion raised in 2024

Construction, logistics, agriculture

Benefits for SMEs

Peer-to-peer lending offers a timely alternative to credit-scarce regions. Through P2P platforms, SMEs can connect directly with investors rather than traditional financial institutions. For businesses in remote areas or with poor credit histories, P2P lending can be a lifeline. That widens the pool of investors that could invest. On top of that, borrowers can leverage their own assets to borrow more.

On the other hand, investors support real businesses and may get attractive returns of 15% from loans that can be diversified across multiple projects and their risk is shared among fellow investors.

Challenges and Risks in the P2P Lending Landscape

P2P lending isn't without its challenges, though.

The obvious risk of borrower default. Unlike traditional banks, since these P2P platforms are not banks, they may not afford you the same protection, so you have to be careful as an investor. Research the risk assessment processes of the platform.

Regulatory frameworks vary across Europe. Some have explicit guidelines; others are still writing regulations. This is inconsistent and confusing for borrowers and investors.

Not all P2P sites are created equal. Some may have weak vetting processes that expose them to fraud or poor performance.

Another problem is liquidity. Investments in P2P loans are typically for fixed terms, and exiting early could prove tricky.

However, despite those challenges, many platforms are using borrowers’ assets as collateral. Blockchain also provides total transparency, as every transaction can be tracked on a ledger. It goes without saying, due diligence is always required.

Future Outlook: Where Is P2P Lending Headed in Europe?

All signs point to a flourishing P2P future for Europe and the likelihood that it will play a dominant role in the global market. Continued technological advancement only enriches P2P platforms (from a UX perspective) and adds refinement to risk assessment tools. This evolution enables both investors and borrowers to engage with the platform more confidently.

Regulators are taking note too. But as the industry expands, moves are afoot for more standard rules throughout Europe. Such consistency may build trust and bring additional participants to the P2P lending area. Moreover, you're seeing more interest in sustainable and impact investments. P2P platforms start featuring projects that reflect these values so investors can invest in initiatives that reflect their values.

Final Thoughts

Without a doubt, P2P lending is changing business financing in Europe by providing flexible and accessible alternatives to banks. Austria, Italy, and Bulgaria illustrate how different economies are using P2P platforms. The sector, as it develops now, offers real possibilities for investors and businesses alike.

Maclear, a Swiss P2P lending site, operates under Switzerland’s stringent conditions, prioritizing top-notch transparency and investor protection. A standout feature is the provision fund, which serves as a safety net covering the interest payments if the borrower fails.