P2P Lending Regulations in Germany: Striking a Balance Between Control and Growth

02.10.2025

6

Germany has €4.2 billion committed in over 200K German P2P accounts. That makes it Europe's largest market but also the most regulated P2P market. While platforms like Auxmoney, Smava, and Lendico continue to match borrowers and investors, Germany's regulator, BaFin, ensures that every new platform adopts sound management practices and investor-centric protection measures.

In this article, we’ll focus on the simultaneous existence of rigorous, "gold-plated" rules and active market growth while also emphasizing the importance of finding a middle ground.

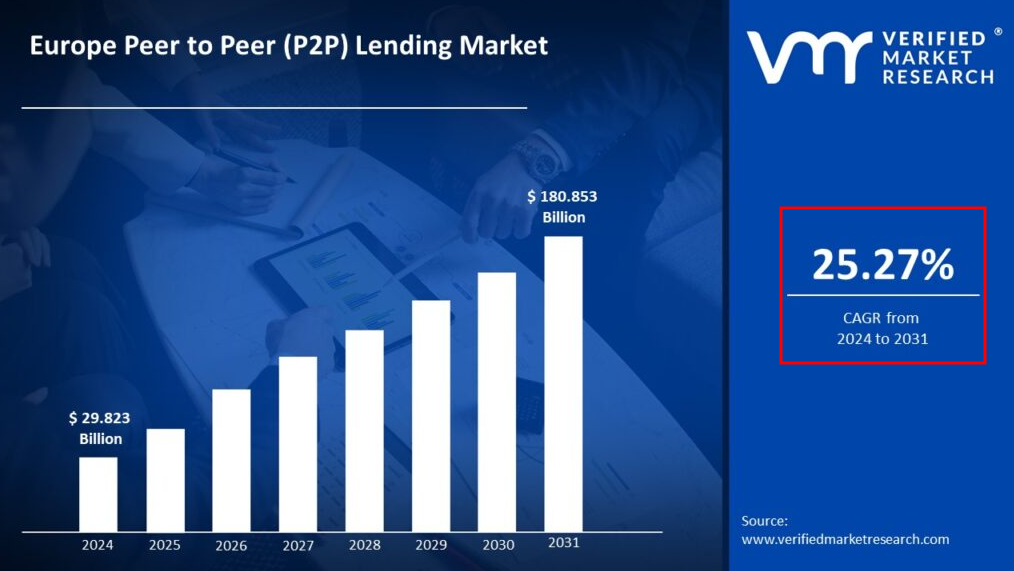

Data released by Verified Market Research shows that peer-to-peer lending in Europe is one of the top-performing market segments, with an expected compound annual growth rate (CAGR) of 25.27% between 2024 and 2031.

In addition to trains, Germany is known for its "Deutsche Pünktlichkeit" in the financial sector. Many people compare German P2P systems to finely calibrated Swiss watches – or, more accurately, German vehicles constructed to stringent specifications – because of the high accuracy of their risk management guidelines and audits.

Germany’s P2P regulatory landscape primarily focuses on exactness, sophistication, and measured calculation. Despite that, the country remains one of the EU’s largest alternative finance markets. Fascinatingly, despite Germany being one of the largest P2P markets in Europe, the country has fewer than 30 active ECSPR-licensed platforms. Instead of an all-you-can-eat buffet, it's more like a gourmet menu with a select few specially chosen foods.

In markets as meticulously regulated as Germany’s, platforms like Maclear demonstrate how innovation and compliance can go hand in hand. By spreading loan risk among diverse investors and applying revolutionary credit scoring, Maclear opens new doors for businesses traditionally underserved by banks– all while providing investors with a balanced, risk-conscious opportunity.

However, P2P expansion has caught the attention of regulators, so a lot of German and European legislators want to ensure growth doesn't compromise safety.

Why These Regulations Matter

According to research from the Cambridge Centre for Alternative Finance, platforms that adhere to strict risk management and transparency guidelines can experience a significant decrease in loan default rates. In Germany, P2P regulations aren't just administrative roadblocks; they're long-standing foundations of confidence that safeguard all investors in a market where accuracy is crucial.

The Regulatory Framework: Pillars of Safety and Trust

Germany's regulators, led by BaFin, distinguish the market by enforcing requirements that often go beyond EU-wide minimums.

Here's a concise glance at the key regulatory pillars:

Regulatory Pillar

What it means for Germany's P2P lending

Investor Protection

P2P lending platforms must provide investors with enhanced risk disclosures, or 'enhanced KIIs+', to clarify all the risks involved.

Platform Licensing

BaFin enforces strict licensing requirements to ensure that only platforms that meet rigorous financial and operational benchmarks can operate. As of January 2025, Germany has an estimated 30 ECSPR-licensed platforms.

Capital Adequacy & Liquidity

P2P lending platforms operating within Germany must maintain buffers of at least 120% of their operational expenses to safeguard against market downturns beyond the EU baseline.

Operational Transparency

Trust-building measures include daily account reconciliations, regular audits, and psychometric testing during the investor onboarding process.

Extended Marketing Restrictions

To ensure clarity and prevent instances of misleading claims, crowdfunding platforms cannot market returns in a "savings account" or make deposits-like promises.

Although these "gold-plated" policies may appear stringent, they are the cornerstone of Germany’s P2P market that prioritizes long-term stability over transient volatility.

Recent Legal and Regulatory Updates in Germany

Germany's P2P lending environment has witnessed further shifts due to significant regulatory changes and court rulings. In 2022, the Frankfurt District Court (Landgericht Frankfurt) ruled that a platform was liable for failing to conduct adequate due diligence on loan originators. This decision upholds the requirement that all platforms follow stringent verification procedures.

In late 2013, BaFin began testing blockchain-based tokenized bonds. This move demonstrated how, despite the already existing strict security protocols, authorities are keen to innovate and experiment with cutting-edge technologies to improve transparency and liquidity without jeopardizing investor protection.

According to BaFin's official website, recent revisions to its guidelines emphasize risk disclosures and data transparency measures. These upgrades match the rate of innovation in investor protection.

These revisions demonstrate how the regulatory system continues to evolve in response to new international standards and technologies.

P2P Taxation in Germany: Navigating the Nuances

P2P lending is no exception to Germany's accurate tax system. Investors should be aware of the following:

Interest income: P2P loan earnings attract personal income tax, which ranges from 20% to 45% based on total income.

Capital gains: Profits from secondary market transactions attract Capital Gains Tax (CGT).

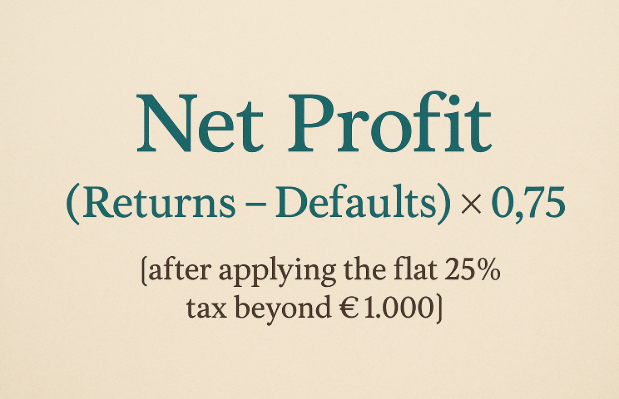

The €1,000 advantage: With a €1,000 annual tax-free allowance, intelligent investors can optimize returns by strategically splitting their investments. A handy rule of thumb is:

Loss harvesting: Selling off defaulted loans to offset gains is still an effective way to ensure that every euro works efficiently. Due to Germany’s highly regulated peer-to-peer environment, financial advisory reports are a crucial component of optimizing net returns and validating these tax management tactics.

The Investor's Dilemma: Balancing Safety with Returns

Germany’s P2P lending landscape is unique, and getting into it ultimately requires investors to weigh the benefits and constraints and create a market entry plan.

On the bright side, investors benefit from a safe environment that includes stringent capital buffers and thorough risk disclosures. Investment choices have a 14-day withdrawal window. And taxation is clear with the predictable, flat 25% tax rate and €1,000 allowance.

Constraints

That said, there are limited platform options. Because of stringent regulations, only three of the top ten European P2P platforms are currently available to German investors. Compared to the higher yields one would get in less regulated markets, expected returns on loans that comply with German regulations are typically between 5 and 8%.

Liquidity is also lacking. Due to BaFin's restrictions on trading in the secondary market and tokenized loan trading, assets are frequently locked in until they mature. Investors should be aware that investing in German P2P is akin to driving a speed-limited Ferrari: it’s exciting, but safety should always take priority.

Looking Ahead: Future Trends and Policy Updates

What prospects does Germany's peer-to-peer lending market have?

Expect higher levels of blockchain technology integration to improve transparency and even open up new liquidity channels, as tokenized bond pilots are already underway. Germany's "gold-plated" system may gradually evolve to align with the EU’s P2P and crowdfunding regulations, such as the ECSPR and others, and remove certain restrictions without compromising investor protection.

The gradual entry of traditional banks and asset managers into the P2P space may further promote quality consolidation and lower default rates. As industry associations and regulatory agencies strive to demystify the complicated world of alternative finance, we can also expect more comprehensive investor education initiatives.

Final Thoughts: The Art of Balance

Germany’s P2P lending industry is an example of the beauty of balance, where safety, growth, and accuracy all coexist. Strict controls may slow down rapid yields, but they also create stability and investor confidence, which will ultimately benefit everyone. If you’re eager to reap the benefits of investing in the German P2P lending landscape, balance is the key.

For those seeking to invest confidently in a regulated and evolving P2P lending environment, Maclear offers a Swiss-rooted platform that blends rigorous risk management with profitable lending opportunities. Discover how Maclear’s approach fits perfectly with Germany’s emphasis on precision and protection.