Spain’s Approach to P2P Lending Regulation: CNMV and Bank of Spain Oversight

09.10.2025

5

Updated:

22.06.2026

Spain's alternative finance market has experienced phenomenal growth in recent years, thanks to new platforms and a regulatory environment that aims to provide investors with some protection while spurring market growth.

Two institutions govern Spain's evolving paradigm: the Bank of Spain and the National Securities Market Commission (CNMV). Collectively, they form an oversight and regulation system that aligns with the EU’s minimum requirements while still being complementary enough to guarantee responsible development.

This deep dive into Spain’s approach to P2P lending regulations will give you invaluable insight that might improve your chances should you decide to foray and invest in this market.

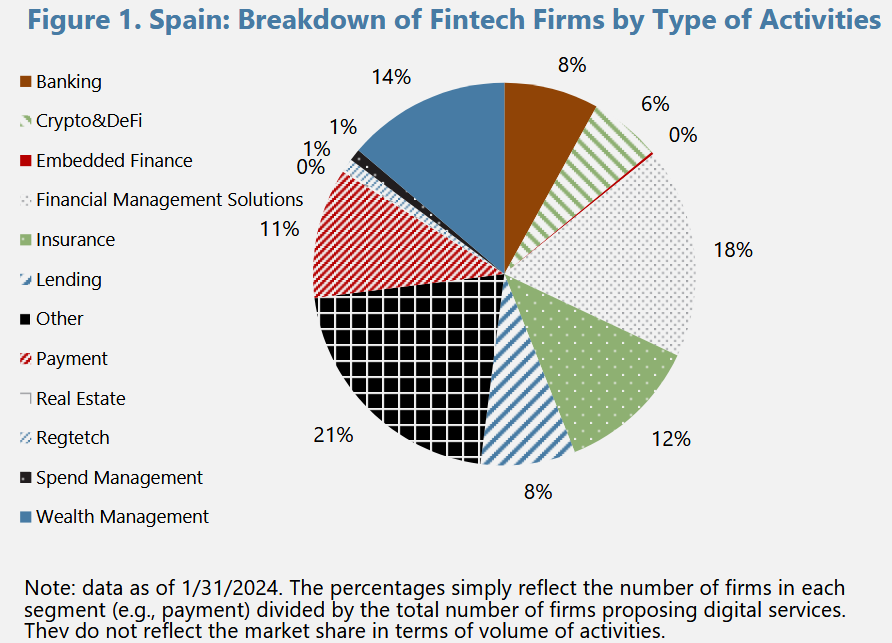

The most recent data provided by Statista indicates that Spain's fintech sector currently consists of approximately 850 active companies. Additionally, the alternative finance market, specifically the peer-to-peer (P2P) lending market, has become increasingly important.

According to recent estimates, Spain's P2P lending market crossed a €3.8 billion threshold in loan origination value in early 2024, with further development prospects driven by local market needs and cross-border possibilities enabled by EU harmonized regulation.

In essence, Spanish P2P lending platforms are a vital bridge between traditional banking paths and excluded borrowers because they offer innovative credit products and attractive, albeit modest, returns to investors.

Due to this bullish growth, regulators have had to step up to ensure that growth does not compromise investor security and financial stability.

Let’s look at Spain’s current P2P regulatory framework.

The CNMV and Bank of Spain

Strong task separation is the hallmark trait of Spain's regulatory framework for P2P lending.

The CNMV, the primary regulator of Spain's securities market, governs investment-based crowdfunding activities and has strict disclosure requirements. The Bank of Spain, on the other hand, regulates credit and lending activities with the traditional prudential and macroprudential regulations.

They collectively enact an integrated framework that ensures transparency, risk management, and capital adequacy across all platforms.

However, let's highlight each body’s mandate.

The CNMV's Mandate

The CNMV's primary mandate is authorizing and regulating platforms that offer capital-raising services. That covers equity-based crowdfunding as well as debt products. Its regulatory approach has multiple pillars:

P2P lending platforms eager to engage in investment-based crowdfunding must receive authorization from the CNMV. The authorization process involves rigorous tests of business models, disclosure regimes, internal procedures, and risk management processes. The CNMV has recently increased its requirements, now requiring crowdfunding platforms to report frequent reviews to maintain their licensed status.

Spanish platforms must conduct periodic disclosures on transparent project risk, borrower creditworthiness, and business performance, as required by the CNMV. These obligations are more stringent than the minimum of the EU Crowdfunding Regulation (Regulation (EU) 2020/1503), thus also offering a further degree of protection to retail investors.

The CNMV also ensures that P2P lending activity remains within the ambit of national legislation, including amendments to the "Crowdfunding Decree" and other relevant financial legislation. The body has recently made several regulatory decisions, including recent March 2025 changes that make internal procedures and investor safeguards more precise.

The Bank of Spain’s Oversight Role

While the CNMV focuses more on investor information and enforcing best practices in the market, the Bank of Spain ensures that Spain’s overall financial system remains stable, using capital requirements to monitor the prudential solidity of P2P lending platforms and requiring platforms to maintain adequate capital buffers to cover operating costs as well as expected credit losses. These guidelines align with standard banking regulations and are Spain’s shot at cushioning its financial system in situations of market stress.

Fail-Safes

In its recent work program for 2025, the Bank of Spain has stressed the importance of implementing early-detection systems that alert non-bank lending platforms of possible vulnerabilities well before they can have disastrous financial implications. Its guidelines ask platforms to grandfather robust risk management systems into their systems, particularly those focusing on high-quality credit underwriting and liquidity management. Such a move is especially vital in a market where unexpected spurts may otherwise lead to excessive credit risks.

Stability

The Bank of Spain publishes regular circulars that oversee credit risk, liquidity management, and digital innovation. The updates allow P2P lending platforms to comply with national prudential standards and European regulatory updates, thus ensuring the market is stable during economic turmoil.

Effects of P2P Regulations on the Spanish Crowdlending Ecosystem

Spain's twin regulatory framework has certain core effects on platforms and investors.

The CNMV has intensified its regulatory surveillance. Coupled with prudential restrictions dictated by the Bank of Spain, this move has skyrocketed investor confidence in Spain’s P2P crowdfunding space. Mandatory disclosure requirements and periodic audits ensure that investors receive high-quality, timely information on the risks and performance of various projects.

Following the full application of the EU Crowdfunding Regulation in November 2023, Spanish P2P platforms now have an easier time conducting business across the European market. The harmonization has rationalized investor protections across member states to an agreed level and given Spanish crowdlending platforms a chance to raise capital from investors across the wider EU.

Within this landscape, the platforms best positioned to grow are those built around transparency, disciplined credit scoring, and the spreading of loan risk across a broad base of investors. Models of this kind aim to give underserved businesses access to fair funding while giving investors a clear view of the risks they take on. In tightly regulated environments like Spain, this combination of robust screening and full disclosure is what allows alternative finance to balance impact, profitability, and investor protection.

Balance

While strict regulations could hinder bullish growth in this emerging market, they are also an excellent way to temper risk and protect investors’ funds. The result is a slow and sustainably growing market instead of a high-speed and potentially volatile-growing market.

Screening

The model expects the platforms to conduct enhanced due diligence on the borrowers, using advanced creditworthiness analysis through advanced tools such as credit databases governed by the Banco de España. The emphasis on thorough screening helps curb the default rate and contributes to the industry’s overall stability.

Recent Regulatory Developments in Spain’s P2P Lending Space

Before we focus on Spain’s recent P2P regulatory developments, remember to check for updates from the two bodies we have mentioned throughout this deep dive, especially if you’re eager to dip your toes into this market as an investor.

The CNMV and Bank of Spain have recently enacted measures aimed at moving the industry closer to current realities in terms of technology and economics. Some of these developments include the following:

The CNMV recently expanded its disclosure requirements to include near real-time data on project performance and credit risk. The move seeks to give potential investors the freshest information possible.

Due to altered market conditions, the Bank of Spain has updated its capital adequacy requirements for non-banking credit institutions, including P2P lending platforms.

After recognizing the potential impact of digital transformation, these regulatory bodies are also exploring pilot projects for tokenized lending. Proposals to use blockchain technology to enhance transparency and secondary markets for digital loans are under development.

CNMV and the Bank of Spain have published recent reports that emphasize the need to account for environmental, social, and governance (ESG) factors in financial risk analysis. All signs point to the trend that sustainable finance will increasingly shape P2P lending, with platforms having to consider ESG factors as part of their credit assessment process.

Investors’ View: 5 Strategic Ways To Reduce and Manage Risk in Spain’s P2P Crowdfunding Space

Below are some key lessons and steps investors interested in Spain’s P2P market can take to manage risk and generate good returns from this ripe-for-picking, well-regulated market.

Investors should periodically review the information provided by the two regulatory bodies and other verifiable data sources. The detailed risk disclosures mandated by the CNMV are like a cheat code that will help you assess borrowers’ credit risk. Conduct thorough due diligence by comparing the historical performance and default risk ratio of different platforms and investment opportunities.

No matter the platform, each investment is likely to have some inherent risks; that’s why diversification is still one of the best and most effective ways to hedge against losses. Although Spain’s highly regulated P2P crowdfunding space is not as volatile as that of other EU member states, do your best to diversify investment capital across platforms and sectors.

Since the Bank of Spain and the CNMV are actively overhauling their structures, stay abreast of regulatory announcements and reports. Remember that some developments from these bodies could provide valuable indicators of untapped or developing market dynamics, trends, and shifts.

The more stringent prudential requirements enforced by the Bank of Spain have created a playground where platforms with strong capital buffers are better able to withstand economic recessions. Therefore, investors should focus more on platforms that meet and exceed minimum regulatory requirements.

Due to the complexity of Spain’s crowdlending regulations, wise investors should consider consulting financial experts who specialize in alternative investments in this market. These experts usually have the know-how to navigate the narrow streets of Spain’s financial regulation.

Conclusion

Thanks to efforts from the CNMV and the Bank of Spain, Spain has a robust P2P regulatory framework that strikes a cordial balance between innovation and sound fiscal management practices.

The system adheres to EU P2P lending guidelines but supersedes it by layering over it supplementary, tailor-made safeguards that ensure the market grows steadily in a transparent and risk-managed environment. All this makes Spain an attractive and lucrative P2P crowdlending market for investors willing to take calculated, well-informed risks!

For investors prepared to do their homework, the combination of EU-level harmonization and Spain’s additional national safeguards makes this one of the more compelling alternative-finance markets in Europe to watch as it continues to mature.