Tax-Efficient Investing: Preserving More of Your Returns

11.11.2025

5

What is as certain as death? You guessed it: taxes!

Accounting for taxes should be a part of every investor’s plan simply because wealth building usually boils down to how much of your income you can keep and reinvest after accounting for taxes and other expenses.

Since how much tax you end up paying on an investment can make all the difference in your investing journey, it’s only fair that we dive deep into the importance of investing in a tax-efficient way.

Every investment portfolio should account for taxes, and investors should always aim to pay the least amount of taxes on their capital gains.

That is the essence of tax-efficient investing: understanding how government bodies tax gains from different assets, and then using all available legal means to lower taxable income.

When you invest wisely and in a way that decreases ‘tax drag,’ it frees up money you can reinvest for compound growth.

Here are some key benefits of prioritizing tax efficiency when making investment decisions:

It protects your actual returns, which is very important because high taxes can erode even the most impressive gross yields.

It works for every investor. From retirement savers to high-net-worth individuals preserving capital, every investor can benefit from legally lowering their taxable income.

Drives compounding. Less paid in taxes means more left to grow tax-deferred or tax-free.

As you can see, taxation is not something any investor should overlook. But how do you invest in a way that ensures you pay lower taxes and keep more of what your investments generate?

You can use various approaches to do that. Let’s start with the most fundamental way.

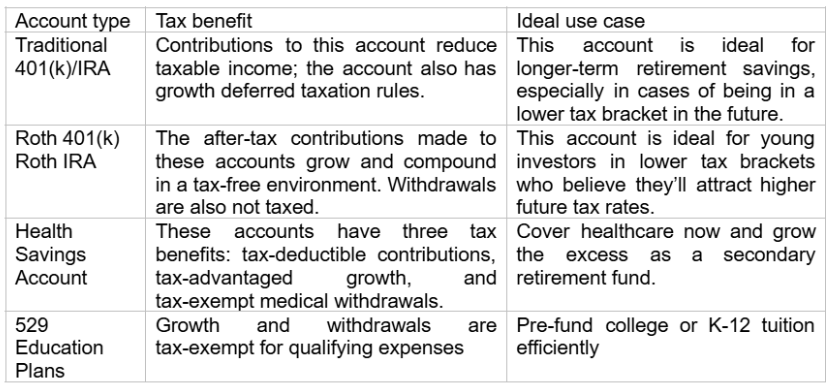

Tax-Friendly Accounts: Your First Line of Defense

Some accounts have better taxation rules than others.

Below are the accounts investors should know about!

Maxing out these accounts each year shelters assets from current or future tax liability. It lets you keep more of your money and compound your wealth.

For investors seeking to maximize their tax efficiency, Maclearcrowdlending platform offers tailored portfolio solutions designed to optimize tax-favored accounts and implement smart asset location strategies. With expert guidance and a Swiss-based platform trusted for transparency and compliance, Maclear helps you keep more of your returns while growing your wealth.

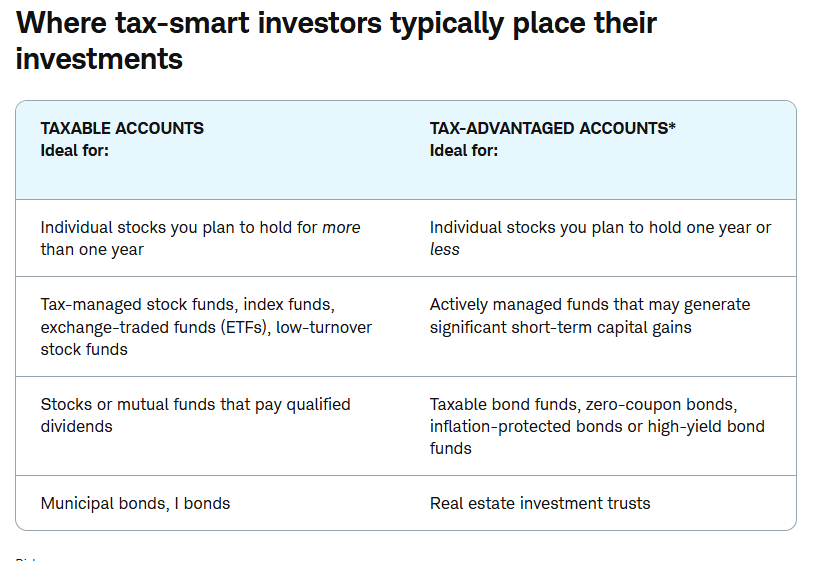

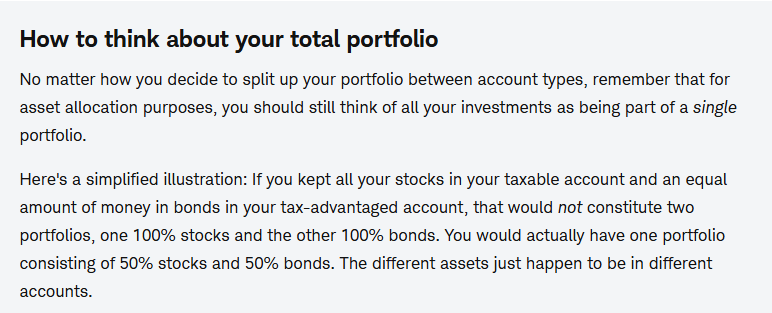

Asset Location as a Smart Tax-Saving Strategy

Considering where your income-generating assets call home is another key tax-efficiency measure investors should not overlook.

Here, you have two basic options:

You can use taxable accounts to purchase and hold tax-friendly assets

You can use tax-friendly accounts to buy and hold tax-unfriendly investments.

Let’s look at an example:

An asset's tax character

Best account placement

Why

Low-turnover ETFs & index funds

It's best to place these in taxable accounts.

These yield good rates in the long run on capital gains

High-yield bonds, REITs, and active funds

It's best to have these in later taxed or untaxed accounts for holdings.

Pursuing this defers or eliminates taxes on interest, dividends, & short-horizon gains on capital.

Having tax-disadvantaged assets inside retirement vehicles and tax-friendly assets in brokerage accounts minimizes annual tax costs and boosts compounding.

For investments like managed mutual funds, REITS, bonds, and other assets that often generate high gains that could increase your taxable income, consider confining them to tax-exempt or deferred accounts. This simple approach delays taxes on short-term capital gains. Some accounts, like the Roth IRA, are so tax-friendly that it might be entirely possible not to pay taxes on gains.

Keeping your income-generating assets in the right account can be an effective way to reduce your annual tax bill so you can keep more of what you make and grow it.

Advanced Way to Lower Your Taxable Investing Income

Investors looking for other ways to create a tax-efficient investing portfolio can consider the following strategies.

Tax-loss harvesting (TLH)

TLH is a simple approach: it’s about selling some investments—even if that means taking a marginal loss on a depreciating asset—to offset capital gains generated by other higher-value holdings in your investment portfolio.

Since this is an advanced strategy, three things matter the most:

Timing: Periodically review your portfolio to find investments you can offload to balance out capital gains elsewhere.

30-day wash-sale rule: Avoid rebuying substantial portions of the same assets within 30 days of offloading.

Carry forwards: Track excess losses you cannot deduct in one year because they typically carry over and may be deductible in future tax years.

Adopt the habit of reviewing your portfolio for depreciating investments you can sell to lower your tax bill.

Roth conversion

Switching to a 401(k) into a Roth IRA is another way to lower your taxable accruals. The move works so well because converting the amount in a tax-delayed account like a 401(k) into a Roth IRA makes future gains and qualified withdrawals at no tax. This tactic is especially great in low-income years because it locks in the tax-free growth in bullish years.

Strategically sell some assets

Savvy investors know that it usually boils down to timing; nowhere is that more true than ‘when’ an investor decides to sell an investment. Short-term investment vehicles usually attract higher capital gains tax. Therefore, hold assets for at least a year to qualify for rate breaks from long-accruing capital.

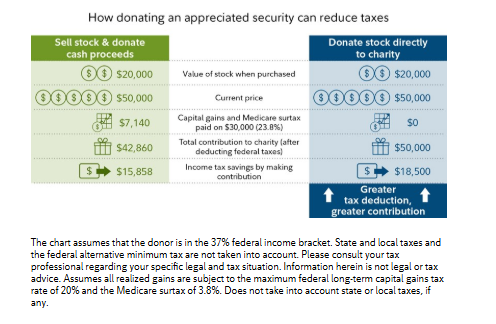

Give to worthy causes

They say nothing feels as good as giving; that’s true, but nothing feels as great as legally lowering your taxable gains. In most countries, charitable donations are tax-deductible. Moves like giving away stocks rising in value to an organization for the needy or establishing a donor-advised fund can count for altruism breaks. It can also be a great way to circumvent taxes from capital gains on gifts.

Takeaways

Use the following optimization tactics to bolster your portfolio holdings:

Max out annual contributions to tax-favored accounts like Roth IRAs and stay aware of IRS updates since contribution limits change. When they do, adjust your savings plan accordingly.

Think about the accounts that hold your investment vehicles. Periodically assess and rebalance your portfolio to keep the entire portfolio tax-lean.

Retain all holdings long enough to take advantage of capital gains breaks down the road. In years of high taxable income, sell depreciating assets to minimize tax payments.

Routinely review your portfolio to uncover assets you can offload to lower your taxable income. Maintain precise records to comply with IRS regulations, track carryforwards, and avoid wash sales.

Consult a reputable financial advisor or tax professional specializing in tax optimization. Professional input is invaluable when putting together a taxation plan that meets your short-term and long-term investing goals.

The world of taxes changes regularly. Being up to date with tax rate changes, the rules, and available incentives is imperative. High-income individuals and those with sophisticated investment situations are particularly in need of this vigilance.

Final Thoughts

Tax-efficient investing is a very effective tool for making your hard-earned funds work for you. By reducing asset location inefficiencies, using complex techniques such as tax-loss harvesting and Roth conversions, tax-favored accounts, and pre-planning tax events, investors can significantly reduce their tax bill. The best gain is the ability to keep more of your profits, to continue investing, and to contribute to the building of sustainable long-term wealth.

Ready to take your tax-efficient investing to the next level? Discover how Maclear crowdlending combines advanced tax planning strategies, portfolio optimization, and Swiss financial expertise to help you preserve more of your hard-earned returns.