Money never sleeps, and neither does innovation of the cunning ways we grow it. While traditional banks continue on with their centuries-old practices, a financial revolution is quietly picking up steam in the peer-to-peer lending space. By 2030, the commotion around it will be all but impossible to drown out.

Maintaining a comprehensive, clear grasp of the investment landscape is becoming harder and harder as it’s changing faster than many people are aware of. What began as a fringe alternative has evolved into a sophisticated market that's projected to reach astronomical figures by the end of this decade. But what's driving this transformation, and what does it mean for investors looking to diversify their portfolios?

Today, we’re going to explore five critical trends shaping P2P lending and what the broader investment market will look like come 2030.

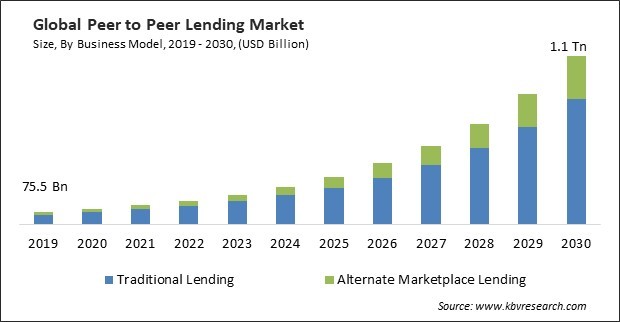

The numbers tell a compelling story. The global P2P lending market has been climbing steadily, but few recognize the acceleration that's about to occur. Currently valued at approximately $176.5 billion in 2025, this market is a force to be reckoned with. By 2030, projections from Precedence Research suggest the market will exceed $700 billion with a CAGR of 25.73%.

That's just peanuts compared to what’s coming, though. Pushing forward to 2034, the market size is expected to balloon to $1.38 trillion, reflecting the steady but staggering 25.73% CAGR.

It’s simple. We are witnessing more than a mere expansion. This is a fundamental restructuring of the ways capital is going to flow throughout the economy, relieving traditional banks of their gatekeeping role. And it’s not about big numbers on paper. This growth unfolding before our eyes indicates a real economic impact through:

Democratized access to capital and financing for previously excluded small enterprises;

New investment opportunities for retail investors seeking yield in a challenging environment;

Lower intermediation costs across the entire lending ecosystem.

These changes aren't happening in isolation. Instead, they’re reflecting dramatic, foundational shifts in how we think about money, technology, and trust.

Real-World Assets: The New Investment Frontier

In the past, P2P lending referred to consolidating credit card debt or financing someone's wedding. Those days are gone. Today's platforms ever more efficiently connect investors to tangible, productive assets that generate real economic value.

For instance, platforms like Maclear have a promoted return of up to 14.9% for investors. This significantly outclasses traditional fixed-income investments, all by providing funding for physical asset acquisition and development.

This wouldn’t have received so much consideration even five years ago. However, P2P platforms are often the first recommendation for investors with an expansion capital of under $5 million.

The comparison to other investment vehicles is particularly striking:

Investment Type

Typical Average Annual Return

Inflation Protection Rating

Bank Savings

0.9%

Poor

10-Year Treasury

3.8%

Moderate

Corporate Bonds

5.2%

Moderate

P2P Real Assets

9.7-14.9%

Strong

Real-world asset allocations in diversified portfolios are projected to grow between 20% and 30% by 2030. It’s not longer just about chasing yield – it’s recognizing the inherent value that assets that produce goods and services for the economy hold. This can include manufacturing, agriculture, or commercial real estate.

The primary concern sophisticated investors had with early P2P models has been addressed with the transition to asset-backed lending. Ultimately, handling tangible assets of standalone value as the basis for lending gives the lender more confidence as opposed to just a borrower’s promise to repay.

Technology Integration: AI and Blockchain Revolution

Two critical technologies are central to the performance of P2P lending platforms – artificial intelligence and blockchain. Let’s explore their contributions in powering these P2P platforms.

AI’s transformation of risk assessment

P2P lending platforms have two powerful technologies that are pivotal to transforming it into sophisticated financial ecosystems out of simple matching services. Artificial intelligence has leapt from mere basic credit scoring to comprehensive risk assessment. Today, it takes only seconds for algorithms to analyze hundreds of data points and patterns that human underwriters often miss.

The results speak for themselves. For instance, CloudBankin's AI-enhanced underwriting system reduced loan default rates by 25%-30% with its early warning capabilities and deeper risk analysis.

Blockchain infrastructure development

Another equally innovative tool is blockchain technology, which executes lending agreements automatically using smart contracts. This injects unprecedented transparency and efficiency to transactions, reducing administrative overhead and ensuring compliance.

Blockchain, in a case study of the lending sector, cut operational costs by 70% in comparison to traditional lending methods. This blend of blockchain and AI makes for a lending ecosystem that's simultaneously more secure and more inclusive. Lending platforms can easily, quickly, and accurately identify qualified borrowers that conventional systems miss while reducing fraud through immutable transaction records.

When they converge, both technologies work magic. AI identifies optimal lending opportunities while blockchain ensures transparent execution.

The Evolving Regulatory Landscape

Unlike what is often the case, where regulation often lags behind innovation, P2P lending has now entered a phase of regulatory maturity that will be a profound determinant in its future.

The European Crowdfunding Service Providers Regulation (ECSPR), implemented in 2021, established the first comprehensive framework specifically addressing P2P lending platforms, far from just a bureaucratic busywork. Strong regulatory frameworks usually instill institutional confidence and legitimacy in the sector.

There’s no doubt that frameworks like the ECSPR are often responsible for creating regulatory certainty, which allows institutional capital to enter the space with confidence. Still, it is an ongoing process that is expected to rein in most of the major financial jurisdictions, with most of them set to develop a similar comprehensive framework by 2030.

Though the framework is not yet perfect, it is still a step in the right direction. Specific improvements that are expected in the coming years include:

Clear capital adequacy requirements ensure platform stability;

The U.S. SEC is also walking a similar path with the development and fine-tuning of its Marketplace Lending Framework. This is expected to be finalized by 2025, producing further clarity for the American market.

The Green P2P Lending Revolution

It’s a wonder how sustainable finance and P2P lending are making so much headway together in this increasingly climate-conscious world. Perhaps it is the timing of changing consumer behavior and innovation brought together by fate.

Nevertheless, this combination is reshaping investment priorities. It is estimated that by 2030, the global market for sustainable financial products could reach $40 trillion with private investment like P2P facilitating the bulk of the projects

This growth aligns with broader European Union sustainability goals and reflects growing investor demand for opportunities that deliver both financial returns and positive environmental impact. Still, P2P platforms are breaking the barrier of tailor-made investment, where capital is deployed to sustainability projects too small for institutional investors but too large for individual funding.

This missing happy medium represents an enormous opportunity for both environmental impact and investment returns.

Other rapidly growing green sectors in the P2P space include:

Energy-efficient building retrofits;

Recycling infrastructure development;

Sustainable agriculture initiatives;

Small-scale renewable energy projects.

For investors, these opportunities represent attractive diversification alongside potential overachievement.

Investment Strategy Implications

How should investors approach this evolving landscape? The transformation of P2P lending calls for not haphazard allocation but thoughtful strategy. The key is understanding where P2P fits within a broader portfolio strategy.

The expectation by 2030 is for P2P allocations to be included in most diversified portfolios, ranging from 5% to 25% for conservative investors and for those with higher risk tolerance, respectively.

Effective strategies include:

Platform diversification: Spreading investments out across multiple lending platforms to mitigate platform-specific risks.

Loan diversification: Maintaining small positions across numerous loans rather than concentrating on a few large positions.

Sector diversification: Balancing exposure across different industries and borrower types.

Liquidity management: Staggering investment maturities to maintain access to capital as needed.

Mostly, P2P is an access mechanism to multiple underlying asset classes for the most sophisticated investors, rather than a single asset class. They understand that real estate projects perform differently from manufacturing loans, which perform differently from consumer credit.

The Path Forward

The transformation of P2P lending by 2030 goes beyond just another new investment opportunity. Think of it as a fundamental shift in how assets are constituted within the economy. As an investor, if you are willing to navigate this evolving landscape thoughtfully, the rewards could be substantial.

What began as a simple concept, i.e., connecting those who have capital with those who need it, has evolved into a sophisticated ecosystem leveraging advanced technologies to deliver new efficiencies. In the near future, P2P platforms will undergo another shift. This time, to challenge the status quo and revamp the traditional means of carrying out financial transactions.