The World’s Most Lucrative Countries for Crowdlending

03.02.2026

7

Crowdlending has become one of the most compelling alternatives to traditional fixed-income investing, but its profitability is far from evenly distributed across Europe. While many investors instinctively look to economically strong countries for safety, the reality is that the most attractive crowdlending returns tend to emerge where bank financing is expensive, rigid, or difficult to access. In these markets, small and medium-sized businesses are willing to pay higher interest rates in exchange for speed, flexibility, and reliable access to capital.

Granted, far from every business or project justifies giving it a loan and inspires confidence that the loan will be repaid. This requires a sophisticated, accurate system for determining risk that outperforms the outdated methods used by traditional banks, so that those who show promise are able to get capital and happily pay back the principal with interest, since they know they are making profits.

In some world regions though, structural gaps in the banking system continue to push borrowing costs well above those seen in Western Europe. Conservative lending policies, limited competition, and underbanked sectors mean that businesses often face interest rates that are two to three times higher than in core European economies. For crowdlending investors, this creates a clear opportunity: higher yields driven by market structure rather than speculative risk.

Why Geography Matters in Crowdlending Profitability

Geography plays a decisive role in crowdlending profitability because lending markets are shaped first and foremost by local banking structures, not by investor demand. In countries where banks dominate SME financing and operate in highly competitive environments, loan pricing is naturally compressed.

Switzerland’s Strongsuit and Downside for Crowdlending

On one hand, Switzerland offers something few other jurisdictions can match: operational certainty. Legal clarity, contract enforceability, strong investor protections, and financial oversight create an ideal base from which to operate cross-border lending activities. In practice, Switzerland functions as a low-yield, high-stability reference point against which other European markets can be measured.

In terms of revenue, Switzerland represents the low end of the crowdlending profitability spectrum and serves as a useful benchmark for understanding why geography matters. The Swiss banking system is among the most competitive, liquid, and risk-averse in the world. Small and medium-sized businesses benefit from strong relationships with banks, access to well-priced credit, and a regulatory environment designed to minimize systemic risk. As a result, business loan interest rates in Switzerland are structurally low and tightly compressed, sitting at under 3% on average.

Balkan Countries: Southeastern Europe

The Balkans and Southeastern Europe present some of the most compelling opportunities for crowdlending investors with spectacularly high business margins and growing SME economies. Each country will feature the average interest rate at which business loans are given out.

Albania: 6.79%

Albania is experiencing stable, steady growth of around 3.5%, fueled by private consumption, foreign investment, and expanding energy and manufacturing sectors. Tourism, renewable energy, and specialized manufacturing there are particularly promising. The strengthening Albanian Lek and EU-aligned policies create a modern, efficient business environment.

Serbia: 7.08%

Serbia is a dynamic, upper-middle-income economy in Central Europe with a growing GDP of 81.3 billion in 2023. Its economy thrives on FDI-supported manufacturing, energy, and ICT, with top exports including insulated wire, electricity, copper ore, and tires. Services account for nearly 60% of GDP, while industry and ICT are fast-growing sectors.

Romania: 8.44%

Romania combines resilience and strategic growth potential, with key sectors in automotive, machinery, IT outsourcing, and manufacturing, with trade focused on machinery, vehicles, and chemicals, and growing SME activity. Investments funded by the EU Recovery and Resilience Facility strengthen infrastructure and innovation.

North Macedonia: 4.51%

North Macedonia is enjoying nice growth of about 3.8%, supported by construction, infrastructure projects, and a strong manufacturing base, especially in automotive and textiles. Private consumption and remittances drive the economy, while trade partnerships with Germany and the UK expand opportunities.

Bosnia and Herzegovina: 5.04%

Bosnia and Herzegovina is steadily growing at roughly 3%, with an economy supported by exports of metals, electricity, and manufactured goods and strong remittance flows. Energy, manufacturing, and industrial enterprises offer promising avenues for crowdlending investors.

Central and Eastern European Countries

CEE countries have outpaced Western Europe in growth, with GDP per capita increasing faster than the EU average since 2004, driven by FDI and EU integration. These economies are highly integrated into global value chains, particularly in automobiles and machinery. The region has attracted substantial FDI.

Poland: 7.09%

Poland’s economy is enjoying a robust recovery, with GDP growth projected at 3.5% in 2026, driven by strong domestic demand, rising wages, and EU-funded investments. The country has a highly developed manufacturing sector, thriving services industry, and low unemployment.

Czechia: 5.16%

Czechia has a mature industrial and automotive base, complemented by growing tech and service sectors. With EU integration supporting trade and capital flows, the country offers a stable environment for lending.

Hungary: 8.43%

Hungary is experiencing a consumption-driven recovery. The interest rates there are among the highest in Europe.

Latvia: 6.21%

Latvia’s economy is rapidly developing in logistics, fintech, and green energy, supported by EU funds and a business-friendly regulatory environment. SMEs are expanding, particularly in Riga’s technology and service hubs.

Lithuania: 4.54%

Lithuania is recognized for its advanced fintech ecosystem, light manufacturing, and transport logistics. Economic stability, EU integration, and increasing SME activity create a promising environment.

Estonia: 4.83%

Estonia is a leader in digital innovation and e-government, fostering rapid growth in tech, IT services, and start-ups. A stable, transparent regulatory framework and a business-friendly climate make crowdlending an appealing way to support SMEs there.

Southern Europe

Southern Europe is strengthening its economies through reforms, EU-funded projects, and sustainable growth initiatives. Labor markets are growing more flexible, foreign investment is rising in manufacturing, technology, and design, and exports remain resilient.

Portugal: 5.01%

Portugal is showing robust growth above 2% in 2026, driven by services, tourism, and EU-funded modernization programs. Falling public debt, low unemployment under 6%, and strong investment in renewable energy and industrial sectors highlight its resilient economic trajectory.

Italy: 3.89%

The eurozone’s third-largest economy is supported by strong exports in manufacturing and luxury goods, as well as EU-funded digital and green projects.

Greece: 4.15%

The nation is in a strong recovery phase, with GDP growth of 2.2% projected in 2026. Investment, tourism, and EU Recovery and Resilience Facility funding are driving growth, while improving banking health, falling unemployment, and structural reforms support long-term stability and competitiveness.

Diversification Strategies for Crowdlending Investors

Successful crowdlending investing requires more than chasing the highest interest rates. Diversification is key to managing risk, smoothing returns, and protecting capital against surprises and market fluctuations.

Get involved in different sectors: Invest across multiple industries, from manufacturing and technology to services and renewable energy. Different sectors respond differently to economic cycles, helping to stabilize returns.

Geographic spread: Crowdlending opportunities exist in markets with varying economic conditions. By allocating funds across countries, investors can mitigate local economic and regulatory risks.

Vary risk profiles: This creates a balance between potential upside and downside protection. Carefully evaluate credit scores, collateral, and cash-flow strength before committing to higher-risk loans.

Utilize secondary markets: Secondary trading provide flexibility to rebalance portfolios.

Monitor and adjust investments regularly: These are not “set it and forget it.” Track performance, monitor borrower updates, and rebalance your allocations.

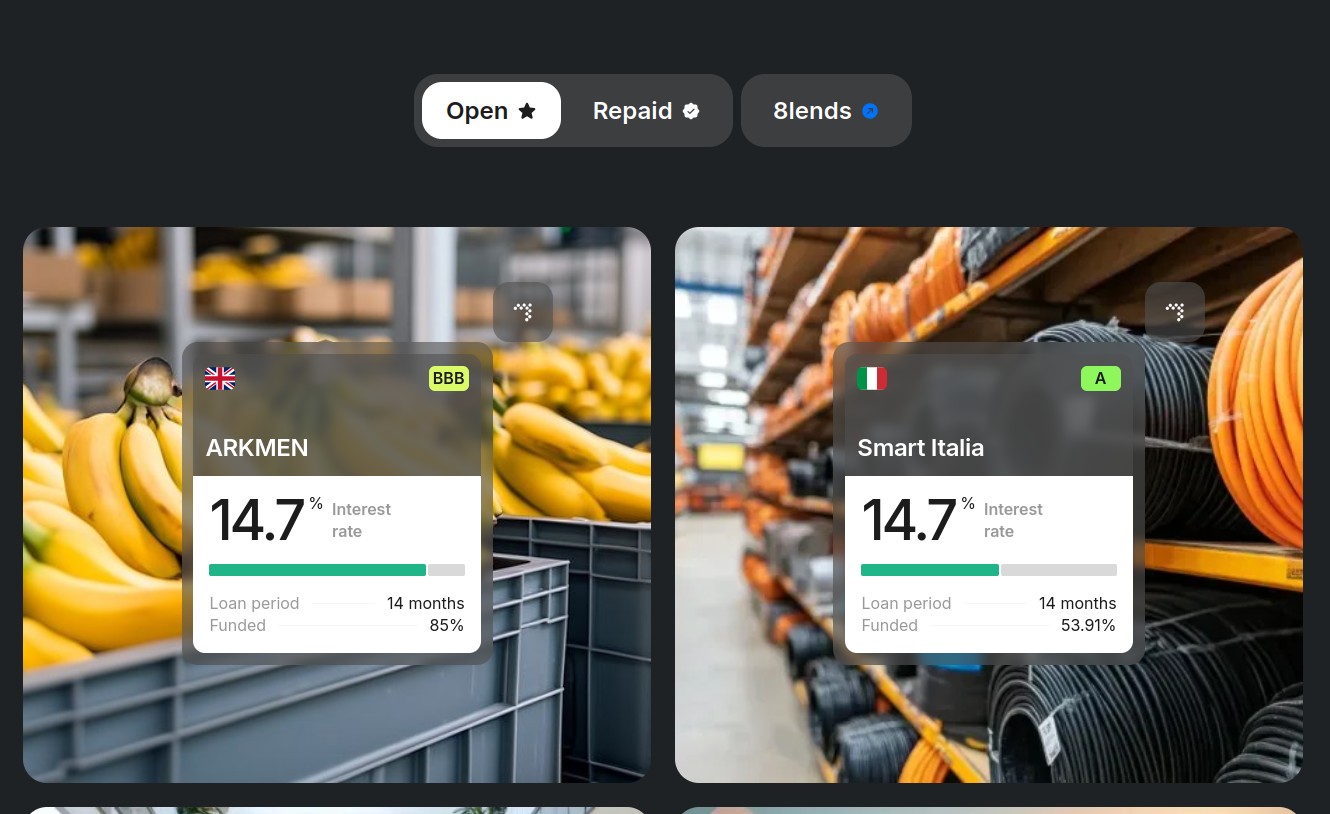

Investing Smarter with Maclear

For investors seeking access to some of the most promising crowdlending markets, Maclear entails a secure and transparent platform to participate in projects rendering as high as 15% interest. Operating under robust Swiss security, Maclear safeguards client funds, offers robust credit assessment using a proprietary 14-point scoring system, and backs all loans with collateral and a provision fund.

With a focus on diversification, transparency, and regulatory compliance, Maclear provides access to SMEs across multiple sectors, from technology and manufacturing to tourism and renewable energy, each heavily vetted with up to a 90% rejection rate. By combining expert risk evaluation with innovative investment solutions, Maclear helps crowdlending investors maximize returns while minimizing exposure.

Loans are disbursed in multiple stages rather than as a lump sum. Investors fund projects step by step, with repayment of principal at the end of each stage.

In case of prolonged default, Maclear acts as a legal collateral agent, managing and liquidating pledged assets.

Each project includes detailed information: borrower credit rating, business description, loan structure, collateral, LTV, and stage progress.

Conclusion

Crowdlending presents a unique chance for investors to earn attractive returns in markets where traditional banking is limited, interest rates are higher, and SMEs are eager for flexible financing. Success in this space relies on understanding local market dynamics, carefully assessing borrower quality, and diversifying across geographies, sectors, and loan structures. By spreading investments and monitoring performance, investors can capture high yields while managing risk effectively.

For those looking to enter these lucrative markets with confidence, Maclear offers a comprehensive solution. With Swiss-based security, a proprietary 14-point credit scoring system, and dual layers of protection – including a provision fund and collateral-backed loans – Maclear allows investors to access high-quality projects across multiple sectors. Step-by-step loan funding, transparent borrower information, and robust risk management render it easier to maximize returns while safeguarding capital.