Is P2P Lending a Threat or Complement to Traditional Banking?

18.12.2025

4

Updated:

29.07.2026

The financial world constantly changes due to new technologies and dynamic customer needs. P2P lending has become critical in the last few decades, gradually transforming from a little experiment into a billion-dollar global business. By eliminating the conventional intermediaries, it begs the question: “Is the supremacy of traditional banking being threatened, or is P2P a complementary force that enhances the general financial ecosystem?”

The answer lies in how P2P lending works, its appeal, how it may be a source of concern to conventional banks, and whether working together would be better than competing.

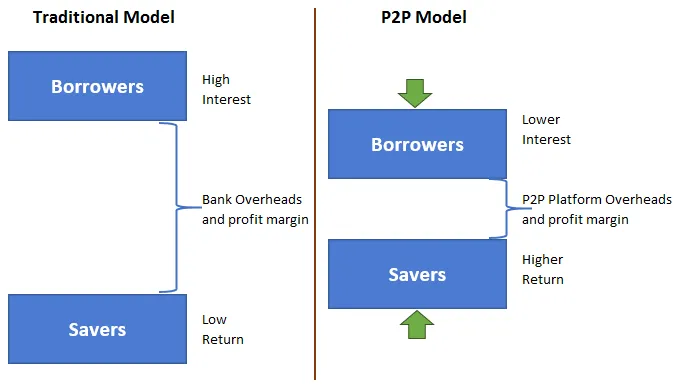

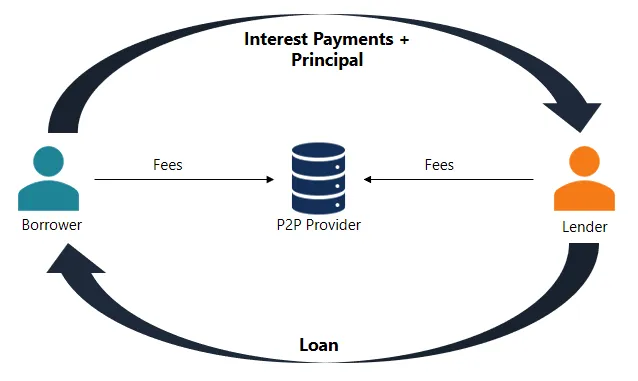

The idea of P2P lending is to cut out the middleman. P2P platforms work like digital markets instead of banks that take deposits and give out loans. People or organizations can choose to fund loans based on the level of risk they are willing to take and the potential return. Borrowers list their loan demands online. The platform takes care of credit checks, payments, and communication, but the lender is usually at risk of the borrower defaulting.

P2P platforms have lower operating costs and more flexible operations than banks, which have high overhead costs and strict rules. This lets them help consumers who may not meet a bank's requirements, like those with unique sources of income, poor credit histories, or regional limits. Customers experience faster loan approval, more options for loan conditions, and often pay less interest. For lenders, P2P lending is a chance to get higher returns and have direct control over their money.

This approach has been very popular in areas where traditional banking services are not very good or are not available, which is one of its best features. But it also speaks to younger, tech-savvy consumers in rich countries who want their financial interactions to be simple, straightforward, and tailored to them.

Why Banks Feel the Pressure

The rise of P2P lending puts significant pressure on the banking paradigm, starting with loan revenue. Banks generate substantial profits by lending to consumers and small businesses. P2P platforms are slowly taking over parts of that industry, especially among borrowers who prioritize speed and ease of use over the security and history of traditional banks.

Another problem is that prices are competitive. Because P2P platforms run their businesses more efficiently, they can give borrowers better rates and investors better profits. For banks, meeting those terms typically means cutting into already thin margins or losing clients.

There is also the issue of new ideas. Peer-to-peer lenders usually use newer, more flexible ways to check credit. Banks typically use standardized credit ratings, but P2P platforms may use other data points, including your activity on social media, level of education, or your firm's cash flow. This helps both people who don't have a lot of traditional credit history and makes banks reconsider how they collect and use customer data.

In some markets, P2P platforms have also had an easier time with rules. This lets them come up with new ideas quickly without incurring traditional bank regulatory fees. Even though regulations have gotten stricter recently, these platforms are still flexible.

The Case for Complementarity

Despite the competition, many agree that P2P lending doesn't spell the end of banks. Both models can live together and collaborate to improve the whole financial system.

Inclusion: often, P2P platforms help people and enterprises that banks don't help. These borrowers have historically been turned away from financial services because they don't make enough money, lack formal employment, or lack sufficient credit history.

Establishing creditworthiness in mainstream financing: They help borrowers create credit profiles and organize their finances, leading to future dealings with banks. Here, P2P lending is not a rival; it helps to get people into the larger financial system.

Specialization: Banks and P2P platforms usually focus on separate markets. Banks are better at mortgages, international trade financing, and wealth management. Conversely, P2P lenders are better at personal loans, debt consolidation, and funding small businesses. This difference makes it possible for people to work together rather than fight. Banks may focus on their main strengths, while P2P platforms keep coming up with new ideas in areas that banks consider too hazardous.

8lends is a prime example of how P2P lending can complement—and even enhance—the traditional financial system. 8lends leverages smart credit analytics and shared-risk lending to open access to capital for small businesses often overlooked by banks. Investors benefit from high-yield, asset-backed opportunities with zero lender commissions.

What’s Holding Banks Back?

Collaboration holds significant potential, but also has specific problems. Banks typically have trouble moving forward because they have old IT systems and a lot of red tape to deal with. Changing the way people think about P2P operations takes more than just new technology; it also requires a culture change. This is difficult in institutions that are geared toward stability rather than change.

The trust aspect is essential. Banks have an enduring history of being safe, thanks to rules, deposit protection, and their importance to the system. Some people are still skeptical of P2P platforms, especially after some fraud or platform failures. This can go both ways: banks may want the quickness and attraction of P2P entrepreneurs, but P2P lenders may wish for the trust and size of banks.

Still, there are many opportunities. Deposits provide banks with access to numerous customers and cheap cash. They also have advanced capabilities for managing risk that might be used in P2P settings.

Blurred Lines and Shared Futures

As rules change and the digital revolution continues, the gap between banks and P2P networks will likely reduce. Many peer-to-peer lenders already act like banks by offering savings accounts, mobile wallets, or even applying for digital banking licenses. To remain competitive, banks are investing in FinTech, developing mobile-first lending products, and streamlining the application process.

Regulators are also paying more attention. In the UK, the US, and Singapore, the government has established rules that make it harder for P2P systems to operate. This aims to safeguard consumers while allowing for new ideas.

This change may make it more expensive for P2P lenders to follow the rules. However, it will make them more trustworthy, enabling them to integrate better with the rest of the financial system.

This new hybrid approach will provide consumers and businesses with more options. People can utilize various platforms and providers to get a quick personal loan, money for a new business, or guidance on managing their money. While some of them are digital-native, others are based in modified traditional institutions.

In the end, the question of whether P2P lending is a danger or a help to traditional banking may not be the right one. We should not think of P2P lending as a zero-sum game. Instead, we should see it as part of a bigger change toward a more open, responsive, and diverse financial landscape. Banks that accept this truth by working together, putting money into new ideas, and reevaluating what they offer will remain relevant in the future.

Conclusion

For the traditional banking sector, P2P lending poses a problem and an opportunity. It breaks the rules that have long been in place, pushes banks to come up with new ideas, and serves groups of people that have been underserved for so long. However, technology makes it possible for people to collaborate, share information, and grow together. Financial institutions may make the future more open, dynamic, and strong by accepting this change instead of fighting it.

There doesn't have to be a clear winner and a loser in the fight between P2P platforms and traditional banks. Instead, it can lead to a new financial system that combines old strengths with new ideas better to suit the requirements of a rapidly changing world.

If you're ready to be part of the shift toward a more open and resilient financial future, 8lends is the place to start. With zero lender commissions, advanced risk modeling, and a mission to fund real-world progress, 8lends puts the power of lending back where it belongs – with people.