Why Current Market Value Matters More Than Book Value in Loan Assessments

05.02.2026

6

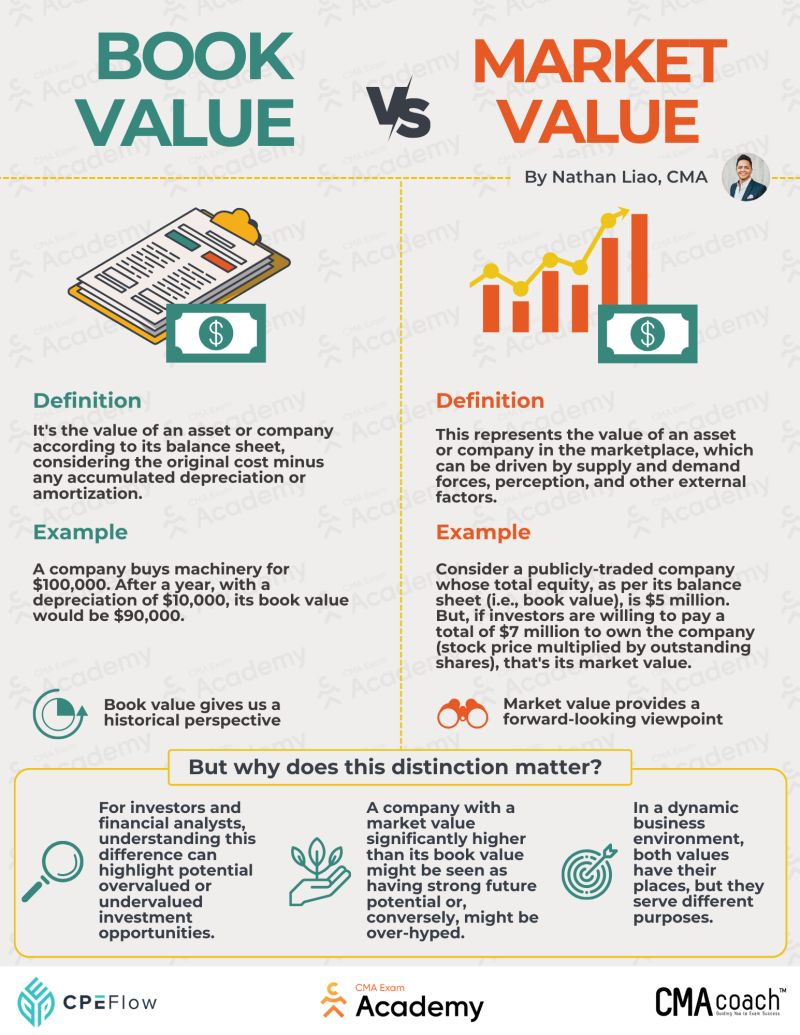

In lending, collateral serves as the safety net that protects investors and lenders from potential losses. Traditionally, many turn to publicly available or private records to assess what particular property would fetch if sold, but these sources often report merely the book value – in other words, a historical figure reflecting the original purchase price minus presumed depreciation. While recorded figures provide a standardized accounting measure, they seldom tell the full story.

For those risking their capital, the market cost of pledged possessions is far more relevant. The distinction proves critical when calculating the loan-to-value ratio, which directly influences allocation decisions, interest rates, and perceived risk exposure. Using outdated or public figures can create a misleading sense of security, while relying on changing assessments ensures that the backing a loan is properly aligned with its liquidation potential.

In dynamic industries – whether real estate, machinery, or vehicles – valuation fluctuates due to supply and demand, technological shifts, and broader economic trends.

This has long been a staple metric in book and corporate finance. It represents the original purchase price of a valuable minus losses over time on the company’s balance sheet. That said, it comes with some problems.

Historical Cost, Not Economic Reality

An object purchased years ago – say, a commercial property, industrial equipment, or a vehicle – may have appreciated significantly due to demand, improvements, or strategic location. There could have been a sudden shortage, as there suddenly was a lack of toilet paper for a while during COVID, and as real estate prices shoot up following gentrification.

Or it could be rendered suddenly totally worthless, like DVDs did when Red Box and Netflix blew up. Old book figures simply cannot capture these fluctuations, creating a gap between the numbers recorded in financial statements and real liquidation potential.

Unaccounted-for Liabilities

Items such as liens, maintenance requirements, or regulatory compliance costs may reduce the effective worth of pledged objects.

Emerging Markets

Here, the discrepancy between original financials and updated estimates may be especially pronounced. Sometimes objects suddenly enter high demand due to regional development, supply constraints, or industry expansion. This is commonly the case with technology already successful in developed regions catching on later in developing regions – such as green energy projects and buy-now-pay-later companies.

Thus, documented financials are a convenient snapshot, but they’re not perfect.

Independent Current Market Value

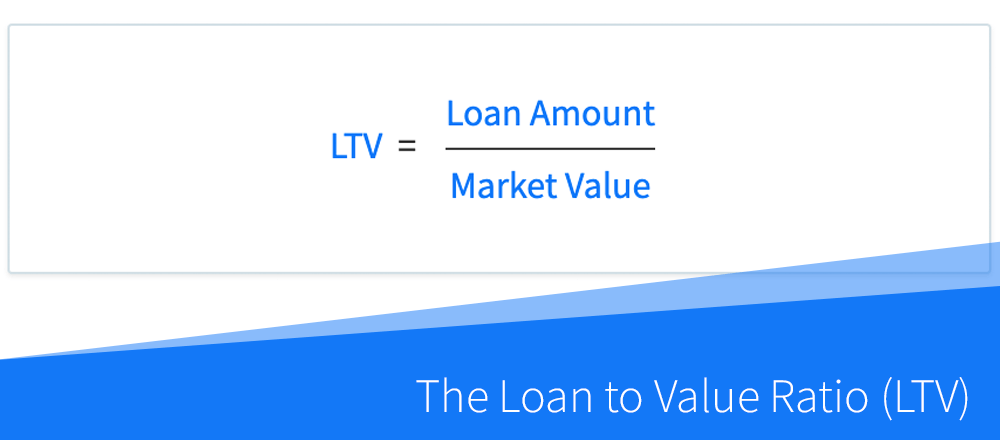

In financing, the LTV ratio is one of the most critical metrics for assessing risk. It expresses the amount of a disbursement relative to the valuation of what backs it. Traditionally, some financiers have mistakenly relied on public figures to calculate LTV; however, a more accurate assessment comes from using the updated price.

Reflecting Real Economic Worth

Consider a small manufacturing company in an emerging economy that purchased machinery five years ago. Its older recorded figures may have depreciated significantly, but if local demand for this type of machinery has increased or if the equipment has been upgraded, its updated estimate could far exceed the original worth.

Independent Valuation

To ensure objectivity, independent assessments are often used to determine current worth. Professional appraisers evaluate the condition, utility, and economic comparables of objects to provide a realistic estimate of what they would fetch in a sale. Independent valuations give both financiers confidence that the LTV ratio accurately represents financial backing.

Aligning with Staged or Milestone-Based Lending

In structured lending models, such as staged or milestone-based financing, new estimates become even more crucial. When tranches are given, contingent on operational achievements, knowing the realistic valuation of pledged property at each stage ensures that exposure remains aligned with recoverable assets. This reduces risk and helps maintain transparency for investors evaluating repayment potential.

How Differences Between Book Financials and New Estimates Affect Crowdlending Decisions

This distinction is critical for crowdlending investors because it directly influences perceived risk and potential return. Funds secured by assets featuring an updated estimate significantly above public figures may justify greater funding or slightly lower interest rates, reflecting the lower effective risk.

This is especially pronounced in sectors with rapid appreciation or technology-driven upgrades. Manufacturing equipment, specialized machinery, or intellectual property can increase in worth after upgrades or increased demand, while documented financials continue to depreciate on paper. Similarly, in real estate or developing economy businesses, local economic growth or development projects can boost the current worth of pledged property far beyond historical cost.

Evaluating Borrower Strategy

Forward-looking growth plans often involve the acquisition of new assets or capital improvements that increase industry worth. By focusing on projections and with documents as proof, investors can better assess whether a borrower’s strategy is credible and likely to succeed, rather than relying solely on historical figures that may understate operational capacity. This is particularly relevant for staged or milestone-based lending, where each tranche requires up-to-date backing coverage.

Public Registry Confusion

A frequent source of confusion for investors is the apparent discrepancy between public registry data and the valuations reported on borrowing platforms. Registries typically record book figures, which reflects historical purchase prices adjusted for accounting depreciation. While this provides a standardized measure, it does not necessarily represent the asset’s updated economic or liquidation appraisal.

Crowdlending organizations, in contrast, use independent, up-to-date valuations to estimate object backing. This approach aligns with standard credit risk management practices and ensures that the LTV ratio reflects realistic collateral strength at the time the loan is issued. Differences between registry figures and platform valuations are therefore not inconsistencies or errors – they simply stem from the use of different methodologies.

At Maclear, every project undergoes a professional appraisal by third-party experts to determine an updated appraisal. Beyond individual projects, Maclear also commissions independent valuations of its own valuation, maintaining transparency and confidence for investors. This dual approach not only aligns with best practices in credit risk management but also provides an additional layer of assurance: investors know that collateral is evaluated objectively, consistently, and under real conditions.

By combining independent appraisals with robust structural protections, Maclear empowers investors to make informed decisions, optimize risk-adjusted returns, and confidently participate in crowdlending opportunities. It has facilitated over 53 million euros in loans, all backed by collateral in addition to a provision fund for protection, with a rejection rate of nearly 90%, providing up to 15% interest on funding for only the most solid projects.

LTV Impact Scenarios

Loan-to-value ratio is calculated based on the amount of a loan given divided by the appraised valuation of the collateral. The higher the former relative to the latter, the greater the risk for the issuer.

Retailer

Suppose a retailer seeks a €500,000 loan to expand operations, offering a 5,000 m² warehouse in Bucharest to back it. The property was purchased 10 years ago for €400,000, and accounting depreciation reduces the book value on the public registry to €350,000. Meanwhile, local commercial real estate has surged, and an independent appraisal today estimates the property at €580,000 due to strong demand, limited supply, and recent infrastructure improvements nearby.

Erroneous LTV: €500 / €350 = 143% → indicates the loan is overleveraged; a lender relying solely on book financials might reject it.

LTV by current appraisal: €500 / €580 = 86% → reflects a realistic, safe level of backing consistent with the latest conditions.

Factory

Imagine a small cutlery producer requests a €200,000 loan. The company’s balance sheet lists machinery at a book value of €180,000 after accounting for depreciation. Yet the machines have recently been upgraded and are in high demand for resale, with an updated estimate of €250,000.

LTV using current appraisal: €200 / €250 = 80% → low to moderate risk, accurately reflecting liquidation potential.

Here, the accounting figures underestimate the backing object’s real economic worth, which could mislead investors or financiers about backing security.

Vehicles

A logistics company applies for a €50,000 loan secured by two trucks. The recorded figures show €60,000, reflecting depreciation over three years, but the refreshed appraisal is €45,000 due to saturation and slower resale demand.

LTV using current appraisal: €50 / €45 = 111% → overleveraged, indicating higher risk for the issuer.

This scenario demonstrates the opposite outcome: the book value has overstated the collateral’s strength, exposing investors to unexpected losses if the operation goes under.

Conclusion

The importance of the difference between book value and current appraisal cannot be overstated when it comes to handing out loans. Older documented figures offer a historical, accounting-based snapshot of an asset, but it often fails to reflect its true economic or liquidation potential. For investors in crowdlending, relying solely on book figures can either understate or overstate risk, potentially leading to poor decision-making. Independent, up-to-date appraisals provide a realistic picture of collateral strength.

Platforms like Maclear exemplify best practices in this regard. Every project undergoes professional, independent estimations, and Maclear even commissions evaluations of its own valuations to maintain transparency and investor confidence. By combining rigorous collateral assessment with structural protections such as a provision fund, high rejection standards, and diversified, milestone-based financing, Maclear empowers investors to participate confidently in crowdlending opportunities.