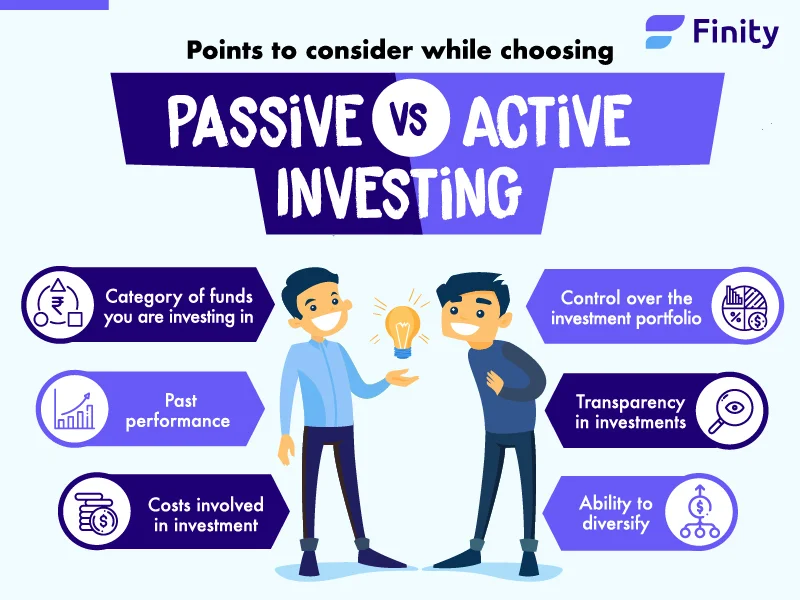

Active vs Passive Investing: Key Differences Explained

31.03.2026

5

It’s one of the most heated debates within the investing world: “Should one simply join the market as a whole and hope to grow wealthier with the masses or pursue more of a professional speculative approach and claim short-term profits from gaps left by market fluctuations?”

Supporters of each approach often preach passionately about performance, risk, and discipline, yet arguing about which strategy “wins” means missing the point. At its core, the active vs passive discussion is about how investors believe markets work, and what role individuals and professionals should play in their involvement with them.

The route you choose to take is going to be hugely impactful since it shapes everything from fees and risk exposure to tax efficiency and emotional stress. Upon becoming more enlightened on the topic, you’ll have the chance to decide what suits your particular objectives better.

Active investing is built around deliberate decision-making: constructing portfolios based on research, forecasts, and judgments about which assets are likely to outperform over a given period, rather than simply mirroring an index.

This process is typically led by professional managers supported by analysts who study:

Financial statements and earnings trends

Macroeconomic conditions and sector dynamics

Company-specific developments and competitive positioning

The goal is to identify mispriced opportunities — situations where the market may be undervaluing a company's prospects or overlooking emerging risks.

Common techniques include selecting individual securities, rotating exposure between sectors, and adjusting position sizes based on economic expectations. This flexibility allows portfolios to shift defensively during downturns or concentrate around high-conviction opportunities when conditions appear favorable.

The trade-off is real, however. Consistent outperformance demands deep expertise, disciplined timing, and tolerance for periods when results fall short of the broader market. Understanding how economic cycles influence asset prices is essential — something covered in more detail in our article on how to align your investment strategy with economic cycles.

What Is Passive Investing?

Passive investing takes a rules-based, long-term view. Rather than attempting to predict winners or adjust positions frequently, portfolios are designed to mirror the performance of a defined benchmark — typically a broad market index.

By tracking an index, this approach delivers instant diversification across many companies or asset classes. Holdings change only when the underlying benchmark changes, keeping turnover low and reducing the need for constant oversight. The underlying philosophy holds that consistently identifying mispriced assets is difficult, and that market prices already reflect most publicly available information.

This structure suits investors who value simplicity, transparency, and minimal intervention. The limitation is an absence of flexibility: when markets decline, passive portfolios fall in line with them, with no mechanism to reduce exposure.

Index funds are among the most widely used vehicles for this strategy. For a practical guide to building long-term wealth through them, see our piece on how to use index funds for passive growth over time.

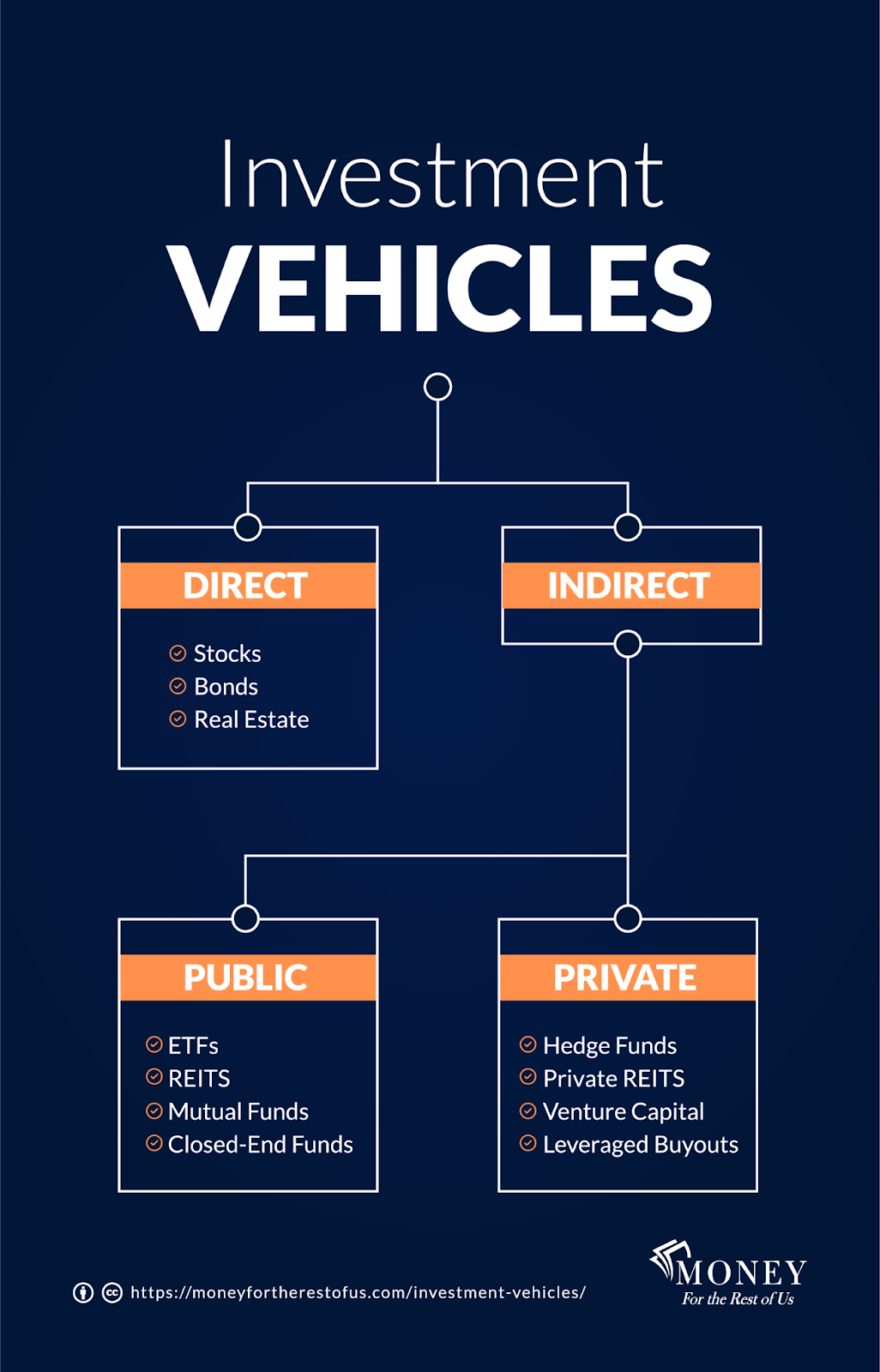

The Most Common Types of Investment Vehicles

Investors build wealth using a wide range of financial tools, though most households concentrate their assets across a small number of familiar categories.

Retirement accounts

Employer-sponsored plans and individual retirement arrangements form the backbone of long-term financial planning for most households, with around 59% of people holding some form of retirement account.

Share ownership

Holding individual companies allows investors to target specific businesses or industries, though it requires a higher tolerance for volatility. This approach suits those who want direct control over their holdings rather than relying on pooled vehicles.

Mutual funds

Estimated at approximately $67 trillion globally, mutual funds sit between hands-on stock selection and fully passive approaches. By pooling capital across many contributors, they provide built-in diversification and professional oversight — making them accessible to investors who want market exposure without managing every decision themselves.

Digital assets

Cryptocurrencies and other digital assets have gained a meaningful foothold in recent years. While still less common than traditional holdings, they attract participants drawn to decentralization, innovation, and the potential for asymmetric returns.

Alternative lending and crowdlending

Crowdlending operates differently from traditional asset classes. It enables credit-worthy projects to secure financing outside the conventional banking system, with risk distributed across multiple investors and returns generated through short-term, collateral-backed loans.

Maclear operates in this space, connecting investors with secured business loans within a regulated Swiss framework. The platform applies an AAA-to-D borrower scoring system based on leading credit assessment practices, and maintains a provision fund to help mitigate downside risk while targeting yields of up to 15% annually. Unlike passive index exposure or speculative equity selection, this model generates fixed-income-style returns uncorrelated to stock market performance.

High-yield savings accounts and certificates of deposit serve a distinct purpose: capital preservation and liquidity. They are commonly used for emergency funds or near-term goals, offering modest returns with minimal risk beyond inflation erosion.

The Cost Difference Between Active and Passive Strategies

One of the most significant factors distinguishing these two approaches is cost. Portfolios built around frequent decision-making, research, and trading naturally carry higher expenses — management fees compensate for professional oversight, while transaction costs accumulate as positions are adjusted.

Index-tracking strategies, by contrast, operate with minimal intervention. Because holdings change infrequently and follow predefined rules, operating costs remain low. These savings may appear modest on an annual basis, but compound meaningfully over long investment horizons — directly improving net returns.

Fees matter because they represent one of the few variables that can be controlled with certainty. Market outcomes are not predictable; costs largely are.

The Major Stock Indices: A Passive Investor's Reference

For investors preferring a passive approach, understanding the structure of major benchmarks is essential. Each index reflects the combined performance of its underlying companies, but the forces driving each benchmark can differ substantially.

S&P 500

Tracking 500 of the largest publicly listed US companies, the S&P 500 is one of the broadest gauges of American economic health. It is weighted by market capitalisation, meaning its largest constituents — predominantly global technology leaders — exert disproportionate influence on overall performance. Earnings surprises, regulatory shifts, or changes in consumer demand affecting these firms can ripple through the entire index.

Dow Jones Industrial Average

The Dow tracks just 30 large US companies, selected by committee rather than size, and is weighted by share price rather than market value. Despite its structural differences, it tends to move in line with the broader US market in response to economic data, corporate earnings, and policy announcements.

FTSE 100

The UK's flagship index is concentrated in financial services, energy, and consumer goods. Because many of its constituents operate globally, its performance is less tied to domestic UK conditions than appearances suggest. Currency movements play an outsized role: a weaker pound often lifts the index as overseas earnings translate into higher sterling-denominated revenues.

DAX

Germany's main benchmark represents a relatively small group of large, export-oriented companies. A strong euro can reduce the international competitiveness of German exporters, making the DAX particularly sensitive to currency movements and shifts in global demand.

Tax Implications of Each Strategy

Active strategies that involve frequent buying and selling generate more taxable events — capital gains distributions, for instance, can create tax obligations even in years when overall portfolio performance is modest.

Why passive strategies tend to be more tax-efficient

Lower-turnover approaches defer gains more effectively. Because holdings change infrequently, capital compounds without being reduced by annual tax payments. When taxes eventually fall due, they are more likely to qualify for long-term rates, which are typically more favourable.

Tax efficiency becomes especially important in taxable accounts, where recurring distributions can quietly erode returns over time. Tax-advantaged accounts reduce or eliminate this concern, making the management style less impactful from a tax perspective.

For a detailed guide on keeping more of what you earn across all strategies, see our article on tax-efficient investing.

Frequently Asked Questions

Is one strategy objectively better than the other?▼

Neither is universally superior. Active strategies offer flexibility and the potential for outperformance; passive strategies offer lower costs, simplicity, and tax efficiency. Most investors benefit from combining elements of both.

Can alternative lending like crowdlending replace active or passive investing?▼

Not as a replacement, but as a complementary allocation. Crowdlending generates returns uncorrelated to equity markets, making it a useful diversifier alongside both traditional strategies.

How does inflation affect passive investors in particular?▼

Long-term passive investors are especially exposed to inflation eroding real returns. Understanding how to protect and grow wealth in inflationary environments is covered in our article on how inflation impacts long-term wealth.

Conclusion: Strategy Is About Alignment, Not Labels

The debate between active and passive investing often oversimplifies a more nuanced reality. Long-term success rarely hinges on selecting a single "correct" method — it depends on aligning strategy with goals, behaviour, time horizon, and real-world constraints.

Costs, risk exposure, tax efficiency, time commitment, and emotional discipline all shape outcomes in ways that headline returns alone do not capture.

Many investors find that combining broad market exposure with selective, income-focused allocations creates a more resilient structure. Diversification across strategies — not just assets — reduces reliance on any single source of returns. For a practical framework, see our guides on how to diversify investments and the best diversification strategies for P2P lending.

Maclear represents one way to extend that framework beyond traditional markets — offering access to private, collateral-backed lending within a regulated Swiss environment. With a provision fund covering late payments, an innovative borrower scoring system that rejects up to 90% of applicants, and yields of up to 15% annually, it occupies a distinct space in the investment landscape.